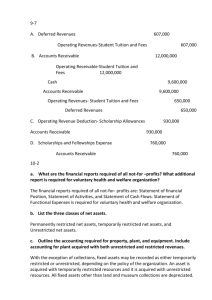

Essentials of Accounting for

Governmental and Not-for-Profit

Organizations

Chapter 12:

Accounting for Hospitals and Other

Care Providers

McGraw-Hill/Irwin

©2007, The McGraw-Hill Companies, All Rights Reserved

12-2

Overview of Chapter 12

•

•

•

•

•

Who has standard setting authority?

What types of entities are included?

General reporting principles

Illustrative transactions

Example Financial Statements

12-3

Ownership Types

Investor Owned:

Humana Corporation

Private Not-For-Profit:

St. Joseph’s Hospital of

Atlanta

•

Stock is listed on the New York

Stock Exchange

The Hospital is owned by the

(Catholic) Archdiocese of Atlanta

The Hospital and other facilities

Government Owned:

are owned by the State of

Medical College of Georgia Georgia

Hospital

12-4

Standard setting authority

• GASB - Category A GAAP

– Authority over government related hospitals

• FASB - Categornot-for-profit GAAP

– Private nonprofit hospitals

• Major FASBs 93, 116,117, 124, 136

– Investor owned hospitals

• Other FASBs

• AICPA Audit Guide for Health Care

Organizations.- Level B GAAP for government

related, private not-for-profits, and business oriented

12-5

What types of Organizations?

• Clinics

• Medical groups

• Individual

practitioners

• Emergency care

• Laboratories

• Surgery care centers

•

•

•

•

•

•

Continuing care

HMOs

Home health agencies

Hospitals

Nursing homes

Rehabilitation centers

12-6

Hospital Financial Statements

– Balance Sheet,

• Most use classified balance sheet –

exception: continuing care communities

– Statement of Operations,

– Statement of Changes in Equity,

– Statement of Cash Flows and Notes

12-7

Display Issues –

Statement of Operations

• Private not-for-profits and

Government related entities must

provide a Performance Indicator

which excludes:

Equity transfers, Restricted Contributions,

Contributions of LT assets, Most unrealized

gains and losses, Restricted investment

returns, Extraordinary items

12-8

Display Issues –

Statement of Operations cont’d

• Patient service revenues shown net of

contractual adjustments; separate out

capitation agreement revenues

• Patient service revenue excludes charity

care

12-9

Display Issues –

Statement of Operations cont’d

• Operating revenues often classified as

– Net patient service revenues, premium (capitation)

revenue, and Other Revenue (parking lot, gift shop,

cafeteria, and tuition).

• Unrestricted gifts may be treated as Operating or

Nonoperating depending on policy.

• Expenses: Minimum must report 2 functions:

health care and general/admin.

12-10

Display Issues – Balance Sheet

• The term restricted used only for donor

restrictions; Assets whose use is limited is

used to indicate board or bond covenant

restrictions.

• FASB vs. GASB equity categories

– FASB: unrestricted, temporarily restricted,

permanently restricted

– GASB: unrestricted, restricted, capital assets net of

related debt

12-11

Comparison of Financial

Statements

• Statement of Operations:

– Similar for not-for-profits, Government,

Business

• Statement of Changes in Net Assets:

– not-for-profits must show details of net changes

for unrestricted, temporarily and permanently

restricted

12-12

Comparison of Financial

Statements

• Statement of Financial Position:

– Classified, similar for not-for-profit, Government,

Business except for equity section

• not-for-profit: unrestricted, temporarily and permanently

restricted

• Government: unrestricted, restricted, invested in capital assets

net of debt

• Business: Contributed Capital and Retained Earnings

• Statement of Cash Flows:

– Bus and not-for-profit, 3 sections; Governmental, 4

sections