GN-e Macroeconomics

advertisement

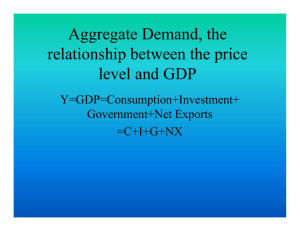

Macroeconomics 6 Business Cycles & Growth Changes in the economy often follow a typical pattern, though where we are on in that pattern is hard to tell while it is happening. This section corresponds to Chapter 12: Sections 2 & 3. OBJECTIVES 60. Describe the phases of the business cycle 61. Discuss aggregate demand and aggregate supply. 62. Identify the causes of the changes in the business cycle and how economists predict those changes. 63. Analyze the causes and measures of economic growth. LX. The four phases of the business cycle KEY CONCEPTS o Business cycle—series of periods of expanding and contracting activity, measured by increases or decreases in real GDP. o Recession—contraction lasting two or more quarters. o Depression—long period of high unemployment, slow business activity. o Stagflation—stagnation in business activity with inflation of prices. A. Stage 1: ★ 1. Expansion is period of economic growth—an increase in real GDP—growing from a low point, or trough. 2. Jobs easier to find; unemployment drops. 3. More resources needed to keep up with spending demand. 4. As resources become scarce, their prices rise. B. Stage 2: ★ 1. Peak is point at which real GDP is highest 2. As prices rise and resources tighten, businesses become less profitable; businesses cut back production, and real GDP drops. C. Stage 3: ★ 1. During contraction, producers cut back and unemployment increases. 2. Resources become less scarce, so prices tend to stabilize or fall. D. Stage 4: ★ 1. Trough is point at which real GDP and employment stop declining. 2. A business cycle is complete when it has gone through all four phases. LXI. Aggregate Demand and Supply A. Aggregate Demand—total amount of products that might be bought at every level 1. It includes all goods and services, ★ 2. Aggregate demand curve is downward sloping a. vertical axis shows average price of all goods and services b. horizontal axis shows the economy’s total output B. Aggregate Supply—sum of all goods and services that might be provided at every price level 1. Aggregate supply curve almost horizontal when real GDP is low, as businesses do not raise prices when economy is weak. 2. Curve slopes upward as prices increase with rise in real GDP 3. Curve almost vertical with inflation—no rise in real GDP C. Macroeconomic Equilibrium—when aggregate demand equals aggregate supply. 1. aggregate demand curve intersects aggregate supply curve 2. increase in aggregate demand shifts AD curve to right 3. decrease in aggregate supply shifts AS curve to left LXII. Changes in the Cycle A. Why Do Business Cycles Occur? 1. Factor 1: Business Decisions a. Decisions by businesses affect suppliers and related businesses b. If enough make similar decisions, ★ c. Demand slump can lead to decreased production, lay offs—contraction d. New technology can raise productivity, demand, employment—expansion 2. Factor 2: Changes in Interest Rates a. Rising interest rates make borrowing costly, ★ b. Decrease household purchases and business investment in capital goods promotes contraction c. Low rates increase home sales—more people qualify for mortgage d. related economic activities increase and economy expands 3. Factor 3: Consumer Expectations a. Consumers’ ideas on prices, business activity, jobs influence choices and can change aggregate demand b. confident consumers tend to consume more, ★ c. Consumer Confidence Survey report published monthly 4. Factor 4: External Issues a. A nation’s economy can be influenced by events beyond its control b. Natural disasters can damage capital, infrastructure c. Conflicts overseas and political decisions made by other countries B. Predicting Business Cycles 1. Economic indicators—measures for predicting changes in business cycle help businesses and government make informed choices 2. Leading indicators—measures that usually change before real GDP 3. Coincident indicators—measures that usually change at same time as real GDP 4. Lagging indicators—measures that usually change after real GDP LXIII. Economic Growth A. What Is Economic Growth? 1. Gauging Economic Growth a. Early theories held that economic growth resulted from: collecting high taxes from growing population, and exporting more than importing. Adam Smith argued “wealth of nations” came from productive capacities. b. Best measure of growth is increase in real GDP. The rate of real GDP change is good indicator ★ 2. Population and Economic Growth a. Population influences economic growth b. If population grows faster than real GDP, growth may mean more workers c. Real GDP per capita—real GDP divided by total population. Real GDP per capita is measure of standard of living. Everyone does not actually have that amount; does not measure quality of life. B. What Determines Economic Growth? 1. Factor 1: ★ a. Access to natural resources is important: arable land, water, forests, oil, mineral resources. b. Resources not enough; also need free market, effective government 2. Factor 2: ★ a. Labor input—size of labor force multiplied by length of work week b. Population growth made up for shorter work week since early 1900s c. More important than size of labor force is its level of human capital 3. Factor 3: ★ a. More and better capital goods increase output; more and better machines can produce more goods. b. Capital deepening—increase in the capital to labor ratio, providing more and better equipment to each worker increases production 4. Factor 4: ★ a. Technology, innovation make efficient use of resources, raise output b. Innovations can increase economic growth C. Productivity and Economic Growth 1. Productivity—amount of output produced from a set amount of inputs a. labor productivity: amount of goods and services produced by one worker in an hour b. capital productivity: amount produced by set amount of equipment and materials 2. How Is Productivity Measured? a. For a business, compare amount of capital and work hours to total output b. Multifactor productivity—★ c. Ratio between economic output and labor and capital inputs used d. Multifactor productivity data compiled for major industries, sectors are used to estimate productivity of entire economy. 3. What Contributes to Productivity? a. Quality of labor—educated, healthy workforce is more productive b. Technological innovation—new technology helps increase output c. Energy costs—cheaper power lowers cost of using tools d. Financial markets—banks, stock markets flow funds where needed 4. How Are Productivity and Growth Related? a. Economic growth is a measure of a change in production b. Productivity ★ c. Economy can grow by increasing quantity of resources, labor, capital, or technology—or by increasing productivity.