ACT1600-Fundamentals-of-financial-accounting

advertisement

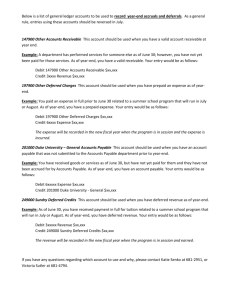

CHAPTER 1 Assets are the resources a business owns. Claims of those to whom the company owes money (creditors) are called liabilities. Claims of owners are called equity. This relationship is the basic accounting equation. Assets must equal the sum of liabilities and equity. (ASSETS = LIABILITIES + EQUITY) ASSETS The business uses it assets in carrying out such activities as production and sales. The common characteristic possessed by all assets is the capacity to provide future services or benefits. LIABILITIES Liabilities are claims against assets – that is, existing debts and obligations. Businesses of all sizes usually borrow money and purchase merchandise on credit. Examples; - Campus Pizza, for instance, purchases cheese, sausage, flour, and beverages on credit from suppliers. These obligations are called accounts payable. - Campus Pizza also has a note payable to First National Bank for the money borrowed to purchase the delivery truck. - Campus Pizza may also have salaries and wages payable to employees and sales and real estate taxes payable to the local government. All of these persons or entities to whom Campus Pizza owes money are its creditors. EQUITY The ownership claim on total assets is equity. It is equal to total assets minus total liabilities. Here is why: The assets of a business are claimed by either creditors or shareholders. To find out what belongs to shareholders, we subtract creditors’ claims (the liabilities) from the assets. Equity generally consists of (1) share capital – ordinary and (2) retained earnings. SHARE CAPITAL – ORDINARY A corporation may obtain funds by selling ordinary shares to investors. Share capital – Ordinary is the term used to describe the amounts paid in by shareholders for the ordinary shares they purchase. RETAINED EARNINGS Retained earnings is determined by three items: revenues, expenses, and dividends. REVENUES Revenues are the gross increases in equity resulting from business activities entered into for the purpose of earning income. Revenues usually result in an increase in an asset. EXPENSES Expenses are the cost of assets consumed or service used in the process of earning revenue. They are decreases in equity that result from operating the business. DIVIDENDS Net income represents an increase in net assets which is then available to distribute to shareholders. The distribution of cash or other assets to shareholders is called a dividend. Dividends reduce retained earnings. However, dividends are not an expense. Summary of Transactions 1. Each transaction must be analyzed in terms of its effect on: (a) The three components of the basic accounting equation. (b) Specific types (kinds) of items within each component. 2. The two sides of the equation must always be equal 3. The share capital – ordinary and retained earnings columns indicate the causes of each change in the shareholders’ claim on assets. Financial statements Companies prepare four financial statements from the summarized accounting data: 1. An income statement presents the revenues and expenses and resulting net income or net loss for a specific period of time. 2. A retained earnings statement summarizes the change in retained earnings for a specific period of time. 3. A statement of financial position (sometimes referred to as a balance sheet) reports the assets, liabilities, and equity of a company at a specific date. 4. A statement of cash flows summarizes information about the cash inflows (receipt) and outflows (payment) for a specific period of time. CHAPTER 2 An accounting is an individual accounting record of increases and decreases in a specific asset, liabilities, or equity item. In its simplest from, an account consists of three parts: (1) a title, (2) a left or debit side, and (3) a right or credit side as a T-account. Journal Entries Ledger (T Account) Dr. ___________ xx (Account name) Cr. ____________ xx Dr. Cr. Rules of debit and credit Asset Dr. Liabilities Cr. Dr. Expense Dr. Stockholder’s Equity Cr. Dr. Nature Debit side Dividends Dr. Cr. Cr. Nature credit side Revenue Cr. Dr. Cr. Steps in the Recording Process Three basic steps in the recording process: 1. Analyze each transaction for its effects on the accounts. 2. Enter the transaction information in a journal. 3. Transfer the journal in formation to appropriate accounts in the ledger. The Journal -is referred to as the book of original entry. Entering transaction data in the journal is known as journalizing. A complete entry consists of (1) the date of the transaction, (2) the accounts and amounts to be debited and credited, and (3) a brief explanation of the transaction. The Ledger –the entire group of accounts maintained by a company The Trial balance –is a list of accounts and their balance at a given time. The steps for preparing are (1) List the account titles and their balances, (2) Total the debit and credit columns, and (3) Prove the equality of the two columns. Example: A group of investors opened Laundromat Inc. on September 1, 2014.During the first month of operations, the following transactions occurred. Sept. 1 Shareholders invested $200000 cash in the business. 2 Paid $10000 cash for store rent for the month September. 3 Purchased washers and dryers for $250000, paying $100000 in cash and signing a $150000, 6 month, and 12% note payable. 4 Paid $ 12000 for a one year accident insurance policy. 10 Received a bill for advertising $2000. 20 Declared and paid a cash dividend to shareholders $7000. 30 Determined that cash receipts for laundry fees for the month were $62000. The chart of accounts are cash(101),Accounts receivable(112),Supplies(126),Prepaid Insurance(130),Equipment(157),Accumulated Depreciation-Equipment(158),Notes Payable(200),Accounts Payable(201),Unearned service revenue(209),Salaries and wages payable(212),Interest Payable(230),Share Capital-Ordinary(311),Retained Earnings(320),Dividends(332),Income Summary(350),Service Revenue(400),Advertising Expense(610),Supplies Expense(631),Depreciation Expense(711),Insurance Expense(722),Salaries and wages Expense(726),Rent Expense(729),Utilities Expense(732),and Interest Expense(905). General Journal J1 Date Account Titles and Explanation 2014 Sept.1 Cash Share Capital-Ordinary (Shareholders’ investment of cash in the business) 2 Rent Expense Cash (Paid September rent) 3 Equipment Cash Note Payable (Purchased laundry equipment for cash and 6 month ,12% note payable) 4 Prepaid Insurance Cash (Paid one year insurance policy) 10 Advertising Expense Accounts Payable (Received bill for advertising) 20 Dividends Cash (Declared and paid a cash dividend) 30 Cash Service Revenue (Received cash for services provided) Ref. Debit 101 311 200000 729 101 10000 157 101 200 250000 130 101 12000 610 201 2000 332 101 7000 101 400 62000 Credit 200000 10000 100000 150000 12000 2000 7000 62000 General Ledger Cash Ref. Date Explanation Debit 2014 Sep.1 J1 200000 2 J1 3 J1 4 J1 20 J1 30 J1 62000 Prepaid Insurance Date Explanation Ref. Debit 2014 Sep.4 J1 12000 Equipment Date Explanation Ref. Debit 2014 Sep.3 J1 250000 Credit No.101 Balance Credit 200000 190000 90000 78000 71000 133000 No.130 Balance Credit 12000 No.157 Balance 10000 100000 12000 7000 250000 Date 2014 Sep.3 Date 2014 Sep.10 Date 2014 Sep.1 Date 2014 Sep.30 Notes Payable Explanation Ref. Debit J1 Accounts Payable Explanation Ref. Debit J1 Share Capital-Ordinary Explanation Ref. Debit J1 Service Revenue Explanation Ref. Debit J1 Credit 150000 No.200 Balance Credit 150000 No.201 Balance 2000 2000 Credit No.311 Balance 200000 Credit 200000 No.400 Balance 62000 62000 Date Dividends Explanation Ref. Debit Credit No.332 Balance 2014 Sep.20 Date Date Advertising Expense Explanation Ref. Debit Credit No.610 Balance 2014 J1 7000 Rent Expense Explanation Ref. Debit Credit 7000 No.729 Balance Sep.10 J1 2014 Sep.2 J1 10000 10000 Laundromat Inc. Trial Balance September 30, 2014 Cash Prepaid Insurance Equipment Notes Payable Accounts Payable Share Capital-Ordinary Dividends Service Revenue Advertising Expense Rent Expense Debit $133000 12000 250000 Credit 150000 2000 200000 7000 62000 2000 10000 $414000 $414000 2000 2000 Chapter 3 Fiscal and Calendar Years A period that a company or government uses for accounting purposes and preparing financial statements. The fiscal year may or may not be the same as a calendar year. For tax purposes, companies can choose to be calendar-year taxpayers or fiscal-year taxpayers. The default IRS system is based on the calendar year, so fiscal-year taxpayers have to make some adjustments to the deadlines for filing certain forms and making certain payments. In many instances, even fiscal year taxpayers must adhere to the calendar-year deadlines. Accounting time periods are generally a month, a quarter, or a year. Adjusting journal entries (at the end of accounting period) Adjusting entries, also called adjusting journal entries, are journal entries made at the end of a period to correct accounts before the financial statements are prepared. This is the fourth step in the accounting cycle. Adjusting entries are most commonly used in accordance with the matching principle to match revenue and expenses in the period in which they occur. 1. Depreciation 4. Supplies 2. Accrued revenue 5. Prepaid 3. Accrued expense 6. Unearned 1. Depreciation (Journal entry) Depreciation expense - Dr. Accumulated depreciation - Cr. 2. Accrued Revenue (Revenue not yet recorded in the journal) Account receivable - Dr. .......................... Revenue - Cr. Note Receivable- Adjusting entry Interest receivable - Dr. Interest revenue - Cr. 3. Accrued Expense (Expense not yet recorded in the journal) ………………… Expense - Dr. .......................... Payable - Cr. Note Payable- Adjusting entry Interest expense - Dr. Interest payable - Cr. 4. Supplies (stationary items like pen, pencil, paper, etc. which the business uses every day) Supply expense (new a/c) - Dr. Supplies (old a/c) - Cr. (Find out the amount for the new a/c) 5. Prepaid (We have to separate expense for this year from prepaid account which was recorded before) …………….expense (new a/c) - Dr. Prepaid ……………. (Old a/c) - Cr. (Find out the amount for the new a/c) 6. Unearned revenue (This is cash received already for future revenue. We have to separate from it revenue earned for the year) Unearned …………… ………….. Revenue (new a/c) (Amount for the new a/c) Dr. Cr. Chapter 4 Completing the Accounting cycle Using Worksheet Worksheet is a multiple-column form used in the adjustment process and in preparing financial statements. Steps in preparing worksheet 1) Prepare a trial balance on the worksheet 2) Enter the adjustments in the Adjustments columns 3) Enter adjusted balances in the adjusted trial balance columns 4) Extend adjusted trial balance amounts to appropriate financial statement columns to appropriate financial statement columns 5) Total the statement columns, compute the net income (or net loss), and complete the worksheet Preparing Financial Statements from a worksheet The income statement is prepared from the income statement columns. The statement of financial position and retained earnings statement are prepared from the statement of financial position columns. Preparing Adjusting Entries from a Worksheet The adjusting entries are prepared from the adjustments columns of the worksheet. Closing the Books At the end of the accounting period, the company makes the accounts ready for the next period. Temporary accounts relate only to a given accounting period and be closed at the end of the period. Permanent accounts relate to one or more future accounting periods and be not closed from period to period. Preparing Closing Entries Directly from the adjusted balances in the ledger by following four entries accomplish the desired result more efficiently: 1) Debit each revenue account for its balance, and credit income summary for total revenues. 2) Debit income summary for total expenses, and credit each expense account for its balance. 3) Debit income summary and credit retained earnings for the amount of net income. 4) Debit retained earnings for the balance in the dividends account, and credit dividends for the same amount. Posting Closing Entries The post-closing trial balance is to prove the equality of the permanent account balances carried forward into the next accounting period. Example Watson Answering Service Inc. Trial Balance August 31, 2014 Cash Accounts Receivable Supplies Prepaid Insurance Equipment Notes Payable Accounts Payable Share Capital-Ordinary Dividends Service Revenue Salaries and wages Expense Utilities Expense Advertising Expense Debit $5400 2800 1300 2400 60000 Credit $40000 2400 30000 1000 4900 3200 800 400 $77300 Other data: a).Insurance expires at the rate of $200 per month. b). $1000 of supplies are on hand at August 31. c).Monthly depreciation on the equipment is $900. d).Interest of $500 in the notes payable has accrued during August. $77300 Watson Answering Service Inc. Worksheet for the Month Ended August 31, 2014 Trial Balance Account Titles Cash Accounts Receivable Supplies Prepaid Insurance Equipment Notes Payable Accounts Payable Share Capital- Ordinary Dividends Service Revenue Salaries and Wages Expense Utilities Expense Advertising Expense Totals Insurance Expense Supplies Expense Depreciation Expense Accumulated Depreciation-Equipment Interest Expense Interest Payable Totals Net loss Totals Dr. 5400 2800 1300 2400 60000 Cr. Adjustments Dr. Cr. (b)300 (a)200 40000 2400 30000 1000 4900 3200 800 400 77300 Adjusted Trial Balance Dr. Cr. 5400 2800 1000 2200 60000 40000 2400 30000 1000 4900 Income Statement Dr. Cr. Statement of Financial Position Dr. Cr. 5400 2800 1000 2200 60000 40000 2400 30000 1000 4900 3200 800 400 3200 800 400 200 300 900 200 300 900 77300 (a)200 (b)300 (c)900 (c)900 (d)500 1900 900 500 (d)500 1900 78700 900 500 500 78700 6300 6300 4900 1400 6300 72400 1400 73800 500 73800 73800 Watson Answering Service Inc. Statement of Financial Position August 31, 2014 Assets Property, plant, and equipment Equipment Less: Accumulated depreciation-equipment Current assets Prepaid insurance Supplies Accounts receivable Cash Total assets $60000 900 2200 1000 2800 5400 $59100 11400 $70500 Equity and Liabilities Equity Share capital-ordinary Retained earnings Non-Current Liabilities Notes payable Current liabilities Notes payable Accounts payable Interest payable Total equity and liabilities Aug.31 Service Revenue Income Summary (To Close revenue account) 31 Income Summary Salaries and Wages Expense Depreciation Expense Utilities Expense Interest Expense Advertising Expense Supplies Expense Insurance Expense (To Close net loss to retained earnings) 31 Retained Earnings Income Summary (To Close net loss to retained earnings) 31 Retained Earnings Dividends (To Close dividends to retained earnings) $30000 2400 $27600 35000 5000 2400 500 7900 $70500 4900 4900 6300 3200 900 800 500 400 300 200 1400 1400 1000 1000 Chapter 5 Accounting for purchase and sale of merchandise The articles they buy and sell are called merchandise. Anything we buy to use in the business is asset. Computation of discount (purchase discount or sales discount). - (Purchase or sale – return) × 𝑟𝑎𝑡𝑒 100 FOB Shipping point = buyer must pay transportation or freight on merchandise purchased (Freight-in). FOB Destination = seller is responsible for freight charges on sale of merchandise (Delivery expense or freight-out). Note: 2/10 = 2% discount if cash paid within 10 days. N/30 = maximum credit period 30 days. Journal Entries for buyer Perpetual 1. 2. 3. 4. Purchase merchandise Inventory XX Cash/ A/P XX Return the merchandise purchase Cash/ A/P XX Inventory XX Paid freight (FOB Shipping point) Inventory XX Cash XX Payment during the discount period Account Payable XX Cash XX Inventory XX Periodic Purchase merchandise Purchase XX Cash/ A/P Return the merchandise purchase Cash/ A/P XX Purchase return & Allowance Paid freight (FOB Shipping point) Freight - in XX Cash Payment during the discount period Account Payable XX Cash Purchase Discount XX XX XX XX XX Journal Entries for seller Perpetual 1. 2. 3. 4. Sell merchandise Cash/ A/R XX Sales XX Cost of Goods Sold XX Inventory XX Customer return the merchandise sold Sales Returns & Allowances XX Cash/ A/R XX Inventory XX Cost of Goods Sold XX Paid freight (FOB Destination) Freight - out XX Cash XX Payment during the discount period Cash XX Sales Discount XX Cash/ A/R XX Periodic Sell merchandise Cash/ A/R Sales XX XX Customer return the merchandise sold Sales Returns & Allowances XX Cash/ A/R XX Paid freight (FOB Destination) Freight - out XX Cash XX Payment during the discount period Cash XX Sales Discount XX Cash/ A/R XX Chapter 6 Inventory is the stock of goods which a business keeps for sales. Ending inventory is the unsold stock of merchandise on the last day of an accounting period (usually December 31). The ending inventory of one year (December 31) is the beginning inventory (January 1) of the next year. Usually ending inventory comes from different purchase. So it is rather difficult to decide the cost of it. The business should include cost of ending inventory in the Income statement and balance sheet. If ending inventory is overstated. Then net income will be overstated under value ending inventory cost will understate net income. There are two main systems to compute cost of ending inventory. 1. Periodic system 2. Perceptual system Periodic system (a) First In first out (FIFO) (b) Weighted average method (c) Lower of cost or market price (LCM) method We must decide the cost of ending inventory. First we must find out the ending inventory in units. The following format we can to get the ending inventory in units. Date Details Beginning Inventory 1st purchase 2nd purchase Less purchase return 3rd purchase 4th purchase Total Unit Unit Sold Ending Inventory (units) Computation of units sold Units sold XX Units sold XX Less sales return (units) Total units sold (XX) XX Units XX XX XX XX XX XX XX (XX) XX Unit Cost XX XX XX XX XX XX Total Cost XX XX XX (XX) XX XX XXX (A) First in first out Under this method merchandise purchased first will be sold first. So ending inventory comes from the last purchase (newest purchase) Cost of ending inventory Cost of goods sold = Total cost – cost of ending inventory (b) Weighted average method Cost of ending inventory = x ending inventory (units) (c) Lower of cost or market price (LCM) method Under this method compute cost price of ending inventory and total market price. Compute both and take the lower one as the cost of ending inventory. CHAPTER 7 BANK RECONCILIATION The common items causing the difference in cash balance as per business records and bank statement are; 1. Deposit in transit. Cash received by the business and given to bank for deposit but the bank not yet recorded the deposit. 2. Outstanding checks. These are check issued by the business, but not yet paid by bank. 3. Credit memo items. These are usually revenue items on which cash was collected by bank for the business and recorded on the deposit column of bank statement but these item are not yet recorded in business records. Ex; note receivable by the business, collected by the bank and record in the bank statement. 4. Debit memo items. These are expenses paid by bank on behalf of the business but not recorded in the business cash payment journal. Ex; note payable paid by bank for the business. 5. NSF cheque. This is a check received by the business from a customer, which is then given to the bank to collect cash from the bank of the customer. But the customers’ bank refuse to pay money on the check saying that there is ‘NOT sufficient fund’ (no cash balance) in customer account. 6. Stop order (payment) check. This is a check issued by the business, then later told the bank not to pay cash on that check but the bank paid cash by mistake. Format of Bank reconciliation statements; 1) Balance as per bank Add deposit in transit xxx xxx xxx Add stop order check Less Outstanding Check No. xxx xxx xxx Corrected balance (adjusted balance) -------------------------------------------> xxx xxx xxx (xxx) xxx (Note. If the bank made any error in recording, that should be corrected here. When we correct the mistake, if each increases in the bank then add it and if cash decrease, then less it) 2) Balance as per book (Business) (BB + Total cash receipt – Total cash payment) Add credit memo items. Note receivable – collected Interest revenue Other revenues Less debit memo items. Note payable paid xxx xxx xxx xxx xxx xxx Interest expense Bank service charges NSF check Other expenses Corrected balance ---------------------------------------------------------------> xxx xxx xxx xxx (xxx) xxx Note. Any error made by accountant business must be corrected here. When we correct the mistake, if cash increases in the business, then add the error, if cash balance decreases, then less the error amount. Adjusting journal entries on bank reconciliation 1) To record credit memo items (revenues) Cash at bank Note receivable Interest revenue Any other revenue 2) To record debit memo items (expenses) Note payable Interest expense A/R (NSF) Miscellaneous expenses (Bank service charge + Collection fees, etc.) Cash at bank xxx xxx xxx xxx xxx xxx xxx xxx xxx