Handout - Casualty Actuarial Society

advertisement

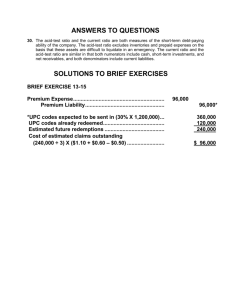

CAS Seminar on Ratemaking Development of an Overall Indication and Calculation of Ratemaking Relativities (INT-1) March 8, 2007 Atlanta, GA Presented by: Gavin Lienemann, FCAS, MAAA & Amy Juknelis, FCAS, MAAA 1 Basic Ratemaking Equation and Its Considerations: Organization of Data Premium Adjustments Loss Adjustments Expense Considerations Other Considerations ORGANIZATION OF DATA I. CALENDAR YEAR DATA (standard accounting year) II. POLICY YEAR DATA III. ACCIDENT YEAR DATA ORGANIZATION OF DATA I. CALENDAR YEAR DATA Premium and Loss transactions that occur during the year. Loss = Payments + change in reserves during year Matches financial statements Data available quickly, least time lag in development Never changes after it is calculated at the end of a year. Premium and Loss transactions DO NOT match Reserve changes from prior years can distort the reliability of the data for ratemaking and management purposes. ORGANIZATION OF DATA II. POLICY YEAR DATA Premium and Loss transactions on policies with effective dates (new or renewal) during the year. Loss = Payments + Reserves Premium and Loss transactions DO match Transactions from policies effective in prior years do not distort the data for ratemaking Data with the greatest time lag (not available until one term after end of the year.) Exact ultimate losses cannot be finalized until all losses settled. ORGANIZATION OF DATA III. ACCIDENT YEAR DATA Loss transactions for accidents occurring during the year. Premium transaction during the same 12 months. Loss = Payments + Reserves Premium and Loss transactions generally match Transactions from accidents occurring in prior years do not distort the data for ratemaking Data with slight time lag Exact ultimate losses cannot be finalized until all losses settled. Basic Ratemaking Equation: Future Premiums = Future Losses + Future Expenses + Underwriting Profit and Contingency Provision BASIC RATEMAKING METHODS Loss Ratio Method develops indicated rate change (A) A = Experience LR / Target LR Pure Premium (PP) Method PP = Loss / Exposure Units develops R indicated rate per unit of exposure (R) = [PP + FE] / [1-VER-Profit Ratio] NOTE: THE TWO METHODS PRODUCE IDENTICAL RESULTS WHEN IDENTICAL DATA AND ASSUMPTIONS ARE USED. LOSS RATIO METHODOLOGY Fixed Expense Approach INDICATED (needed) RATE LEVEL CHANGE = Projected Experience Loss + Fixed Expense Ratio Expected (Target) Loss + Fixed Expense Ratio For Example: 90.3% - 1.0 = + 17.9% 76.6% - 1.0 LOSS RATIO METHODOLOGY Experience Loss + Fixed Expense Ratio Projection Premium Adjustments Adjust to Current Rate Level Premium Trend Loss Adjustments Loss Development Loss Trend Catastrophe Adjustments RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . . (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . . . (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . . (7) Annual Loss Trend ___% Trend Period: (8) Exponential Trend Factor [1.0 + (7)] ** Trend Period. . . . . . . . . . . . (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . . (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . . C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0. . . . . . . . . . . . . . . Sample Rate Level Indication Assumptions • Annual Policies. Rates to be revised as of JANUARY 1, 2008 • Loss Ratio Methodology • EXPERIENCE PERIOD: ACCIDENT YEAR 2006 2006 Earned Premium $3,690,000 Reported Incurred Losses as of 12/31/06: $1,900,000 PREMIUM ADJUSTMENTS Current Rate Level Adjustment Loss Ratio Method analyzes the appropriateness of the CURRENT RATES for use in the future. CRL adjustment reflects rate changes NOT already included in historical recorded premium. PREMIUM ADJUSTMENTS Current Rate Level Adjustment - Common Techniques Extension of Exposures • Re-rate each exposure (policy) • Requires extensive detail and mechanization • Most accurate method Parallelogram Method • Easier method • Specific policy information not required • Assumes even distribution of policies written throughout the year CURRENT RATE LEVEL ADJUSTMENT Extension of Exposures Method 2006 Earned Exposures Class 1 1,500 1,995 2,700 Territory 1 Territory 2 Territory 3 Class 2 2,260 3,010 2,500 Current Rates Class 1 $150 $175 $220 Territory 1 Territory 2 Territory 3 Class 2 $300 $350 $440 Premium @ Current Rates Territory 1 Territory 2 Territory 3 Statewide total Class 1 $225,000 $349,125 $594,000 Class 2 $678,000 $1,053,500 $1,100,000 $3,999,625 CURRENT RATE LEVEL ADJUSTMENT Parallelogram Method A B 1/05 1/06 1/07 1/08 1/09 Rate Change History Date Change Rate Index From 1/1/05 to 6/30/06 None 1.000 A 7/1/06 + 12% 1.12 (1 * 1.12) B CURRENT RATE LEVEL ADJUSTMENT Calculation of On-Level Factor - Parallelogram Method I. Rate Index for 2006: Area Percent of 2006 Rate Index A B 87.5 12.5 1.000 1.120 100.0 1.015 TOTAL II. On-Level Factor for 2006: (1) Current Index (2) 2006 Index (3) On-Level Factor (1) / (2) 1.120 1.015 1.103 (4) 2006 Earned Premium $3,690,000 (5) 2006 Earned Premium @ Current Rate Level $4,070,070 RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . (7) Annual Loss Trend ___% Trend Period: (8) Exponential Trend Factor [1.0 + (7)] ** Trend Period. . . . . . . . . . . (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0 . . . . . . . . . . . . . . . 3,690 1.103 PREMIUM ADJUSTMENTS Premium Trend To project the premium level which will exist during the period being priced. The premium trend accounts for shifts of business that will also impact the losses. Must adjust for items such as: Average car model year or price group Average home value Territorial distribution shift Any item that would impact future premium or both premium and losses in the future except policy count Premium Adjustments Premium Trend – Determination of Trend Period • • Annual Policies. Rates to be revised as of JANUARY 1, 2008 EXPERIENCE PERIOD: ACCIDENT YEAR 2006 2006 Experience Period 2007 2008 Policies Effective 2009 <COVERAGE PROVIDED> Avg. Earned Date is 7/1/06 Avg. Earned Date under Revised Rates is 1/1/2009 TREND PERIOD is 2.50 Years Assuming an average annual trend of 2% for this example, the premium trend would be: (1.02) ^ 2.5 = 1.051 RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . . (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . . . (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . . (7) Annual Loss Trend ___% Trend Period: 2.5 years (8) Exponential Trend Factor [1.0 + (7)] ** 2.5. . . . . . . . . . . . . . . . . . . . (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . . (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . . C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0 . . . . . . . . . . . . . . . 3,690 1.103 1.051 4,278 LOSS RATIO METHODOLOGY Experience Loss + Fixed Expense Ratio Projection Loss Adjustments Loss Development Loss Adjustment Expenses Allocated Loss Adjustment Expense (ALAE) Unallocated Loss Adjustment Expense (ULAE) Generally included with loss Generally loaded to Loss & ALAE Loss Trend Catastrophe Adjustments LOSS ADJUSTMENTS Loss Development Analysis Adjust historical losses to an expected ULTIMATE value Reflects revisions to claim values as claims are settled Used with policy and accident year data Reflects IBNR reporting. Reflects development on reported claims. Key Factors for Consideration Observation of historical patterns Incurred and Paid developments Development period Accident Year Loss Development Analysis INCURRED METHOD - Recognizes SYSTEMATIC inaccuracy of case reserves INCURRED LOSSES & ALAE Adjusted for Deductibles and Cats, (000’s) ACCIDENT YEAR 2001 2002 2003 2004 2005 2006 12 mos 1,200 1,300 1,400 1,500 1,600 1,900 Reported as of: 24 mos 36 mos 1,488 1,548 1,755 1,843 1,708 1,691 1,800 1,836 1,968 48 mos 1,548 1,843 1,691 Age to Age Development Factor = Incurred Loss @ Later Report Period divided by Loss @ Prior Report Period AY 2004 12 mos TO 24 mos Factor = $1,800 / $1,500 = 1.20 Accident Year Loss Development Analysis INCURRED AGE-TO-AGE FACTORS ACCIDENT YEAR 12-24 mos 24-36 mos 36-48 mos 2001 2002 2003 2004 2005 1.24 1.35 1.22 1.20 1.23 1.04 1.05 0.99 1.02 1.00 1.00 1.00 Average 1.248 1.025 1.000 Selected 1.248 1.025 1.000 x Cumulative Age-to-Age Factors 1.279 x 1.025 1.000 LOSS DEVELOPMENT ANALYSIS (1) Accident Year 2003 Incurred Loss & ALAE @ 12/06 1,691 (2) Cumulative Age to Ultimate Factor 1.000 (3) Estimated Ultimate Loss (1) * (2) 1,691 2004 1,836 1.000 1,836 2005 1,968 1.025 2,017 2006 1,900 1.279 2,430 RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . . 3,690 1.103 1.051 4,278 (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . . . 2,430 (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . . (7) Annual Loss Trend ___% Trend Period: 2.5 years (8) Exponential Trend Factor [1.0 + (7)] ** 2.5. . . . . . . . . . . . . . . . . . . . (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . . (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . . C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0 . . . . . . . . . . . . . . . EXPENSE ANALYSIS Unallocated Loss Adjustment Expense Countrywide Figures (in $ millions) Year Incurred Losses & ALAE Unallocated Loss Adjustment Expenses ULAE to Losses & ALAE Ratio 2004 2005 2006 $61,200 79,000 82,300 $6,500 7,800 8,300 10.6% 9.9% 10.1% Estimated Future ULAE Percentage as a percentage of Incurred Losses & ALAE 10.0% RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . . 3,690 1.103 1.051 4,278 (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . . . 2,430 (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . . 1.10 (7) Annual Loss Trend ___% Trend Period: 2.5 years (8) Exponential Trend Factor [1.0 + (7)] ** 2.5. . . . . . . . . . . . . . . . . . . . (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . . (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . . C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0. . . . . . . . . . . . . . . 29 LOSS ADJUSTMENTS Loss Trend Analysis Project to the loss level predicted to exist during pricing period Data Issues • Separate Claim frequency and Severity Trends? • Internal Vs. External Data ? • Paid, Incurred, Reported data ? • Calendar Vs. Accident year ? • Length of Historical period ? • Credibility ? • Extrapolations of Historical Data? (Least Squares Regression, Time Series, Econometric Models) LOSS TREND ANALYSIS Calendar Year 1999 2000 2001 2002 2003 2004 2005 2006 Paid Losses Earned Exposures ($ 000’s) (000’s) Premium 1,212 13.0 1,356 13.2 1,496 13.3 1,726 13.4 1,730 13.6 1,839 13.7 1,984 13.8 2,108 14.0 Pure $ 93.23 $102.73 $112.48 $128.81 $127.21 $134.23 $143.75 $150.57 Annual Trend based on Least Squares (exponential ) 6.6% Most Recent Annual Change (150.57 / 143.75) 4.7% Other Possible Trend Sources C.P.I. Medical Care Index C.P.I. Auto Body Work Index C.P.I. Home Maintenance & Repair Index 3 - 4% 4 - 5% 3 - 4% RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . . 3,690 1.103 1.051 4,278 (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . . . 2,430 (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . . 1.10 (7) Annual Loss Trend _5.0__% Trend Period: 2.5 years (8) Exponential Trend Factor [1.0 + (7)] ** 2.5. . . . . . . . . . . . . . . . . . . . 1.13 (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . . 3,020 (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . . (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . . C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0. . . . . . . . . . . . . . . LOSS ADJUSTMENTS CATASTROPHES Catastrophes should be eliminated from losses Average provision should be used as a loss loading Example: (1) Expected Annual Catastrophe Loss & ALAE for Projection Period 394 (2) Projected Premium 4,278 (3) Catastrophe Load (1) / (2) 9.21% RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . . 3,690 1.103 1.051 4,278 (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . . . 2,430 (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . . 1.10 (7) Annual Loss Trend _5.0__% Trend Period: 2.5 years (8) Exponential Trend Factor [1.0 + (7)] ** 2.5. . . . . . . . . . . . . . . . . . . . 1.13 (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . . 3,020 (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . . 394 (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . . C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0. . . . . . . . . . . . . . . UNDERWRITING EXPENSE ANALYSIS Direct Expenses Other Than Loss Adjustment Countrywide Figures (In $ Millions) 2004 Written Premium Commissions 2005 2006 Selected $ % $ % $ % 107,400 100 121,600 100 142,400 100 16,647 15.5 % 18,850 15.5 22,100 15.5 15.5 Other Acquisition 6,703 6.2 7,250 6.0 8,235 5.8 5.8 Administrative 7,332 6.8 7,977 6.6 9,101 6.4 6.4 3,652 3.4 4,100 3.4 4,900 3.4 3.4 Taxes, Licenses & Fees Commissions and Premium Taxes vary directly with premiums Other acquisition and general expenses are “fixed” expenses • Not really fixed - vary with inflation DEVELOPMENT of EXPECTED LOSS RATIO & FIXED EXPENSE RATIO Total Commissions Variable Fixed 15.5% 15.5% Other Acquisition 5.8 0.0 5.8 General 6.4 0.0 6.4 Taxes, Licenses & Fees 3.4 3.4 0.0 Profit & Contingency 4.0 4.0 0.0 Other Costs * 0.5 0.5 0.0 35.6% 23.4% 12.2% TOTAL TARGET Loss, LAE & Fixed Expense Ratio = 100.0% - 23.4% = 76.6% * Policyholder Dividends, Involuntary Market Costs, Guaranty Fund Assessments, Etc. (if allowable) 0.0% RATE INDICATION WORKSHEET Loss Ratio Methodology - Fixed Expense Approach A. EXPERIENCE Loss + Fixed Expense Ratio = (9 + 10+ 12) / (4).. . . . . . 90.3% (1) (2) (3) (4) 2006 Earned Premium . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Current Rate Level Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Premium Trend Factor . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Trended Premium @ Current Rate Level = (1)*(2)*(3) . . . . . . . . . . 3,690 1.103 1.051 4,278 (5) Accident Year 2006 Ultimate Losses & ALAE . . . . . . . . . . . . . . . . . . 2,430 (6) Unallocated Loss Adjustment Expense (ULAE) Factor. . . . . . . . . . . 1.10 (7) Annual Loss Trend _5.0__% Trend Period: 2.5 years (8) Exponential Trend Factor [1.0 + (7)] ** 2.5. . . . . . . . . . . . . . . . . . . . 1.13 (9) Trended Ultimate Losses and LAE = (5) * (6) * (8) . . . . . . . . . . . . 3,020 (10) Expected Catastrophe Loss & LAE for Projection Period. . . . . . . . . 394 (11) Fixed Expense Ratio (FER). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12.2% (12) Fixed Expenses = (1) * (11). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 450 B. EXPECTED (Target) Loss + Fixed Expense Ratio. . . . . . . . . . . . . . . . . . . . . 76.6% C. INDICATED RATE LEVEL CHANGE = (A / B) - 1.0. . . . . . . . . . . . . . . +17.9% Introduction to Ratemaking Relativities Why are there rate relativities? Considerations in determining rating distinctions Basic methods and examples Advanced methods Why are there rate relativities? Individual Insureds differ in . . . Risk Potential Amount of Insurance Coverage Purchased With Rate Relativities . . . Each group pays its share of losses We achieve equity among insureds (“fair discrimination”) We avoid anti-selection What is Anti-selection? Anti-selection can result when a group can be separated into 2 or more distinct groups, but has not been. Consider a group with average cost of $150 Subgroup A costs $100 Subgroup B costs $200 If a competitor charges $100 to A and $200 to B, you are likely to insure B at $150. You have been selected against! Considerations in Setting Rating Distinctions OPERATIONAL Objective definition Administrative expense Verifiability LEGAL Constitutional Statutory Regulatory SOCIAL Privacy Causality Controllability Affordability ACTUARIAL Accuracy Homogeneity Reliability Credibility Basic Methods for Determining Rate Relativities Loss ratio relativity method Produces an indicated change in relativity Pure premium relativity method Produces an indicated relativity The methods produce identical results when identical data and assumptions are used. Loss Ratio Relativity Method Class Premium @CRL Losses Loss Ratio Loss Ratio Relativity Current Relativity New Relativity 1 $1,168,125 $759,281 0.65 1.00 1.00 1.00 2 $2,831,500 $1,472,719 0.52 0.80 2.00 1.60 Pure Premium Relativity Method Class Exposures 1 6,195 2 7,770 Losses Pure Premium Pure Premium Relativity $759,281 $123 1.00 $1,472,719 $190 1.55 Incorporating Credibility Credibility: how much weight do you assign to a given body of data? Credibility is usually designated by Z Credibility weighted Loss Ratio is LR= (Z)LRclass i + (1-Z) LRstate Methods to Estimate Credibility Judgmental Bayesian Z = E/(E+K) E = exposures K = expected variance within classes / variance between classes Classical / Limited Fluctuation Z = (n/k).5 n = observed number of claims k = full credibility standard Loss Ratio Method, Continued Class Loss Ratio Credibility Credibility Weighted Loss Ratio Loss Ratio Relativity Current Relativity New Relativity 1 0.65 0.50 0.61 1.00 1.00 1.00 2 0.52 0.90 0.52 0.85 2.00 1.70 Total 0.56 Off-Balance Adjustment Class Premium @CRL Current Relativity Premium @ Base Class Rates Proposed Relativity Proposed Premium 1 $1,168,125 1.00 $1,168,125 1.00 $1,168,125 2 $2,831,500 2.00 $1,415,750 1.70 $2,406,775 Total $3,999,625 $3,574,900 Off-balance of 11.9% must be covered in base rates. Expense Flattening Rating factors are applied to a base rate which often contains a provision for fixed expenses Multiplying both means fixed expense no longer “fixed” Example: $62 loss cost + $25 VE + $13 FE = $100 Example: (62+25+13) * 1.70 = $170 Should charge: (62*1.70 + 13)/(1-.25) = $158 “Flattening” relativities accounts for fixed expense Flattened factor = (1-.25-.13)*1.70 + .13 = 1.58 1 - .25 Deductible Credits Insurance policy pays for losses left to be paid over a fixed deductible Deductible credit is a function of the losses remaining Since expenses of selling policy and non claims expenses remain same, need to consider these expenses which are “fixed” Deductible Credits, Continued Deductibles relativities are based on Loss Elimination Ratios (LER’s) The LER gives the percentage of losses removed by the deductible Losses lower than deductible Amount of deductible for losses over deductible LER = (Losses<= D)+(D * # of Clms>D) Total Losses Deductible Credits, Continued F = Fixed expense ratio V = Variable expense ratio L = Expected loss ratio LER = Loss Elimination Ratio Deductible credit = L*(1-LER) + F (1 - V) Example: Loss Elimination Ratio Loss Size # of Claims Total Losses Average Loss Losses Net of Deductible $100 $200 $500 0 to 100 500 30,000 60 0 0 0 101 to 200 350 54,250 155 19,250 0 0 201 to 500 550 182,625 332 127,625 72,625 0 501 + 335 375,125 1120 341,625 308,125 207,625 Total 1,735 642,000 370 488,500 380,750 207,625 153,500 261,250 434,375 0.239 0.407 .677 Loss Eliminated L.E.R. Example: Expenses Total Variable Fixed 15.5% 15.5% 0.0% Other Acquisition 5.8% 0.0% 5.8% General 6.4% 0.0% 6.4% Unallocated Loss Expenses 6.0% 0.0% 6.0% Taxes, Licenses & Fees 3.4% 3.4% 0.0% Profit & Contingency 4.0% 4.0% 0.0% Other Costs 0.5% 0.5% 0.0% 41.6% 23.4% 18.2% Commissions Total Use same expense allocation as overall indications. Example: Deductible Credit Deductible Calculation Factor $100 (.614)*(1-.239) + .182 (1-.234) 0.848 $200 (.614)*(1-.407) + .182 (1-.234) 0.713 $500 (.614)*(1-.677) + .182 (1-.234) 0.497 Advanced Techniques Multivariate techniques Why use multivariate techniques Minimum Bias techniques Example Generalized Linear Models Why Use Multivariate Techniques? One-way analyses: Based on assumption that effects of single rating variables are independent of all other rating variables Don’t consider the correlation or interaction between rating variables Examples Correlation: Car value & model year Interaction Driving record & age Type of construction & fire protection Multivariate Techniques Removes potential double-counting of the same underlying effects Accounts for differing percentages of each rating variable within the other rating variables Arrive at a set of relativities for each rating variable that best represent the experience Minimum Bias Techniques Multivariate procedure to optimize the relativities for 2 or more rating variables Calculate relativities which are as close to the actual relativities as possible “Close” measured by some bias function Bias function determines a set of equations relating the observed data & rating variables Use iterative technique to solve the equations and converge to the optimal solution Minimum Bias Techniques 2 rating variables with relativities Xi and Yj Select initial value for each Xi Use model to solve for each Yj Use newly calculated Yjs to solve for each Xi Process continues until solutions at each interval converge Minimum Bias Techniques Least Squares Bailey’s Minimum Bias Least Squares Method Minimize weighted squared error between the indicated and the observed relativities i.e., Min xy ∑ij wij (rij – xiyj)2 where Xi and Yj = relativities for rating variables i and j wij = weights rij = observed relativity Least Squares Method Formula: Xi = ∑j wij rij Yj ∑j wij ( Yj)2 where Xi and Yj = relativities for rating variables i and j wij = weights rij = observed relativity Bailey’s Minimum Bias Minimize bias along the dimensions of the class system “Balance Principle” : ∑ observed relativity = ∑ indicated relativity i.e., ∑j wijrij = ∑j wijxiyj where Xi and Yj = relativities for rating variables i and j wij = weights rij = observed relativity Bailey’s Minimum Bias Formula: Xi = ∑j wij rij ∑j wij Yj where Xi and Yj = relativities for rating variables i and j wij = weights rij = observed relativity Bailey’s Minimum Bias Less sensitive to the experience of individual cells than Least Squares Method Widely used; e.g.., ISO GL loss cost reviews Can be multiplicative or additive Can be used for many dimensions (convergence may be difficult) Easily coded in spreadsheets Generalized Linear Models Generalized Linear Models (GLM) provide a generalized framework for fitting multivariate linear models Statistical models which start with assumptions regarding the distribution of the data Assumptions are explicit and testable Model provides statistical framework to allow actuary to assess results Generalized Linear Models Can be done in SAS or other statistical software packages Can run many variables Many Minimum bias models, are specific cases of GLM e.g., Baileys Minimum Bias can also be derived using the Poisson distribution and maximum likelihood estimation Generalized Linear Models ISO Applications: Businessowners, Commercial Property (Variables include Construction, Protection, Occupancy, Amount of insurance) GL, Homeowners, Personal Auto Suggested Readings ASB Standards of Practice No. 9 and 12 Foundations of Casualty Actuarial Science, Chapters 2 & 5 Insurance Rates with Minimum Bias, Bailey (1963) A Systematic Relationship Between Minimum Bias and Generalized Linear Models, Mildenhall (1999) Something Old, Something New in Classification Ratemaking with a Novel Use of GLMs for Credit Insurance, Holler, et al (1999) The Minimum Bias Procedure – A Practitioners Guide, Feldblum et al (2002) Suggested Readings (Continued) A Practitioners Guide to Generalized Linear Models, Anderson, et al (2004) Statement of Principles Regarding P&C Insurance Ratemaking Insurance Operations, Webb et al (CPCU) Chapters 10 & 11 Introduction to Ratemaking and Loss Reserving for P&C Insurance, Robert L. Brown Chapter 3 Trend and Loss Development Factors, Cook (1970)