File

advertisement

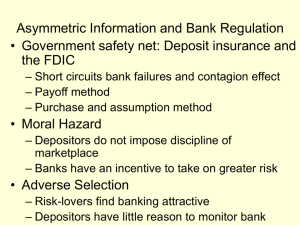

Chapter 11 – EC311 Susanto ECONOMIC ANALYSIS OF FINANCIAL REGULATION Introduction • Financial services sector heaviest regulated in U.S. economy • Historically bank panics/runs were regular events in the U.S. • After 1929 crash major reassessment of regulation of financial services in the U.S. • Deposit insurance introduced to protect depositors - $250,000 of deposits insured Asymmetric Information And Banking Regulation • The asymmetric information problem leads to two reasons why the banking system might not function well: – Bank Failure: bank is unable to meet its obligations to pay its depositors and other creditors • Depositors would have to wait to get their deposits until the bank was liquidated. – Depositors’ lack of information about the quality of bank assets can lead to bank panics • Depositors may be reluctant to put their money in the banks • Banks operate on a “ sequential service constraint” depositors have a strong incentive to be first in line to withdraw their money when uncertainties arise bank panics, which is contagious Asymmetric Information And Banking Regulation There are nine basic categories of financial regulation: 1. Government safety net 2. Restrictions on asset holdings 3. Capital requirements 4. Prompt corrective action 5. Chartering and examination 6. Assessment of risk management 7. Disclosure requirements 8. Consumer protection 9. Restrictions on competition 1. Government Safety Net • Prevents bank runs due to asymmetric information: when depositors can’t tell good from bad banks • Also provides protection for depositors • One form of safety net is deposit insurance, provided by the Federal Deposit Insurance Corporation (FDIC) • Two methods to handle a failed bank: • • Payoff method: FDIC allows the bank to fail and pays off the deposits up to the insurance limit. After liquidation, FDIC pays of creditors from liquidated assets. Typically, large account holders get > 90 cents on the dollar for their deposits. Purchase and assumption: FDIC reorganizes the bank, finds a willing merger partner to take over; no depositors or creditor loses a penny. FDIC often provides subsidized to buy the failed banks weaker assets. FDIC guarantees all liabilities and deposits (more costly, bust most commonly used up to 1991). 1. Government Safety Net • Moral Hazard – The existence of insurance increases the incentives for taking risks that might result in an insurance payoff (depositors are protected) – Depositors and creditors don’t impose market discipline on banks • Adverse Selection – Risk-seekers find banks as attractive ways to gain financing – Depositors have little incentive to monitor banks’ activities • Too big to fail – A failure of a large bank can cause a major financial disruption – Regulators are reluctant to allow big institutions to fail – Government provides repayment guarantees for large uninsured creditors of the largest banks, so nobody would suffer a loss (purchase and assumption method) – Problems: increases moral hazard for big banks (may take excessive risks); little incentive for monitoring; costs taxpayers a lot of money 1. Government Safety Net • Financial Consolidation (poses two challenges) – Increases too-big-to fail problem: there are now more large institutions whose failure would expose the financial system to systemic risk. – Financial consolidation of banks with other financial services firms: the government safety net may be extended to new activities such as securities underwriting, insurance, or real estate activities increasing incentives for greater risk taking in these activities weaken the fabric of the financial system. 2. Restrictions on Asset Holdings • Risky assets usually have higher potential earnings (when they pay off), but higher probability for default • Plus, depositors are unable to assess a bank’s risk-taking activities • Another moral hazard from too much risk taking • Bank regulations restrict banks from holding risky assets in order to avoid too much risk (e.g., banks not allowed to hold common stocks) 3. Bank Capital Requirements • Another way to reduce the bank’s incentives to take on risk, thus minimizing moral hazard • More capital, more to lose, also provides cushion • Higher capital means more collateral for FDIC • Takes two form: 1. Based on leverage ratio (amount of capital/total assets) A good leverage ratio must exceed than 5% If falls below 3%, regulatory requirements to be met 2. Risk-based capital requirements Basel Accord: required banks to hold capital at least 8% of their riskweighted assets Criticism: bank risk as stipulated by the weights can differ from the actual risk (incentive for regulatory arbitrage) 4. Prompt Corrective Action • If he amount of capital galls to low levels, two problems: 1. Bank likely to fail because smaller capital cushion 2. Less capital, less “skin in the game” moral hazard with risk-taking • FDIC is required to intervene earlier and more vigorously – “Undercapitalized” banks: required to submit a capital restoration plan, restricted asset growth, have to seek approval to open new branches 5. Bank Supervision: Chartering and Examination • Supervision allows regulators to monitor whether the bank is complying with a capital requirements and restrictions on asset holdings, also function to limit moral hazard • Charters are obtained from OCC or state banking authority • Chartering reduces adverse selection problem of risk takers or crooks running banks • Examination: through on-site investigations or call reports (periodic reporting on a bank’s balance sheets, income, etc) • Bank examiners give banks a CAMELS rating, based on 6 areas: Capital adequacy, Asset quality, Management, Earnings, Liquidity, and Sensitivity to market risk. 6. Assessment of Risk Management • Due to financial innovations, on-site examinations of banks balance sheets are often inadequate • Greater emphasis on evaluating soundness of management processes for controlling risk • Trading Activities Manual of 1994 for risk management rating based on 4 elements: – – – – Quality of oversight provided Adequacy of policies and limits for all risky activities Quality of the risk measurement and monitoring systems Adequacy of internal controls • Interest-rate risk limits – Internal policies and procedures – Internal management and monitoring – Implementation of stress testing and Value-at risk (VAR) 7. Disclosure Requirements • Requirements to adhere to standard accounting principles and to disclose wide range of information • Help the market assess the quality of portfolio and the amount of risk exposure • Limit incentives to take on excessive risk and improve the information quality for investors to make informed decisions • The Sarbanes-Oxley Act of 2002 established the Public Company Accounting Oversight Board • Mark-to-market (fair-value) accounting – Assets are valued at what they could sell in the market (vs. book value) – Major flaw: when market stops working, the price of assets sold at a time of distress may not reflect its fundamental value create shortfall in capital cutback in lending assets prices go down – However, when assets prices are booming, balance sheets look good 8. Consumer Protection • Consumers may not have enough information to protect themselves fully. • Standardized interest rates (APR): Fair Credit Billing Act (1974) • Preventing discrimination: – Community Reinvestment Act (1977) which prevents “redlining” – lender’s refusal to lend in a particular area – Equal Credit Opportunity Act (1974/76) • Learning from the subprime mortgage crisis: There is a need for greater consumer protection; borrowers took out loans with terms they did not understand and that were beyond their means 9. Restrictions on Competition • Increased competition squeezes profits profitability decline may take on greater risks to make profits • Many governments institute regulations to protect financial institutions from competition – intended to reduce risk taking • Branching restrictions (eliminated in 1994) • Separation of banking and securities industries: Glass-Steagall (eliminated 1999) • Disadvantages: – Lead to higher charges to consumers – Decrease the efficiency of banking institutions (don’t have to compete too vigorously) Summary • Getting regulators to do their jobs is difficult • Financial firms have strong incentives to avoid existing regulations by finding loopholes • Subtle differences in details may have unintended consequences • Regulated firms spend a lot of money to lobby politicians to go easy on them Table 1 Major Financial Legislation in the United States Table 1 Major Financial Legislation in the United States Bank Failures in the United States, 1934–2008 Source: www.fdic.gov/bank/historical/bank/index.html. Case study: the 1980s S&L crisis Early Stages 1. Decreasing profitability due to financial innovations and disintermediation: banks take risk to keep profits up 2. Deregulation in 1980 and 1982, more opportunities for risk taking (Garn-St.Germain Act allowed S&Ls to put funds into financial markets) 3. Innovation of brokered deposits enabled circumvention of $100,000 insurance limit 4. inflation i , net worth of S&Ls A. Insolvencies B. Incentives for risk taking Result: Failures and risky loans Case study: the 1980s S&L crisis By end 1982 >50% of S&Ls with negative net worth and $10bn in losses Later Stages: Regulatory Forbearance – not closing S&Ls 1. Regulators allow insolvent S&Ls to operate because A. insufficient funds to pay depositors B. sweep problems under rug – hope they’ll go away C. FHLBB cozy with S&Ls 2. Huge increase in moral hazard for zombie S&Ls: now have incentive to “bet the bank” 3. Zombies hurt healthy S&Ls A. Raise cost of funds B. Lower loan rates 4. Outcome: Huge losses – by 1986 > $20bn 5. Late 1986 FSLIC bankrupt Financial Institutions Reform, Recovery and Enforcement Act (FIRREA) of 1989 1. New regulatory structure: Office of Thrift Supervision as new regulator, FDIC takes over FSLIC fund 2. Resolution Trust Corporation (RTC) created and given funds to close insolvent S&Ls: cost of $150bn 3. Core capital requirement from 3% to 8% 4. Reregulation: Asset restrictions like before 1982 Federal Deposit Insurance Corporation Improvement Act (FDICIA) of 1991 1. FDIC recapitalized with loans and higher premiums – /$100,000 2. Reduce scope of deposit insurance and too-big-to-fail 3. Prompt corrective action provisions 4. Risk-based premiums – based on asset risk 5. Annual examinations and stricter reporting 6. Enhances Fed powers to regulate international banking Banking Crises Throughout the World • Remarkable similarity: all started with financial liberation or innovation • Deposit insurance is not to blame for some of the crises • The common feature of these crises is the existence of a government safety net, where the government stands ready to bail out troubled financial institutions. FIGURE 2 Banking Crises Throughout the World Since 1970 Source: Gerard Caprio and Daniela Klingebiel, “Episodes of Systemic and Borderline Financial Crises” mimeo., World Bank, October 1999. Table 2 The Cost of Rescuing Banks in Several Countries Whither Financial Regulation After the Subprime Financial Crisis? • Regulation should focus on limiting the agency problems created by the “originate-to-distribute” business model • Increased regulation of mortgage brokers – Tighten licensing requirements – Require to disclose information • • • • Fewer subprime mortgage products. Regulation of compensation Higher capital requirements Increased regulation of credit-rating agencies – Restrict conflicts of interest • Additional regulation of derivatives Whither Financial Regulation After the Subprime Financial Crisis? • Additional regulation of privately owned government sponsored enterprises (four options) – Fully privatize them – Completely nationalize them – Leave them as privately owned government sponsored enterprises but strengthen regulation – Leave them as privately owned government sponsored enterprises but reduce their size