The Time for Cyber Coverage is

Now

Your insureds and clients

Are Not Immune

October 8, 2014

Kevin Ribble

E.V.P. Edgewater Holdings

President, EPRMA.org

kribble@edgewater.net

(214) 676-8662 (office)

(312) 431-1766 (fax)

Texas License # 1682508

Today’s Agenda

Introduction to Panel

Cyber Crime statistics

Why are mid-market accounts considered to Be at High-Risk?

Types of Threats

What is the potential harm to your insureds and client’s businesses?

Overview of Data Breaches

Overview of a cyber-attach

Case Studies

Risk Transfer & Risk Management

Cyber coverages recommended & broker coverage check list

Summary

Q&A

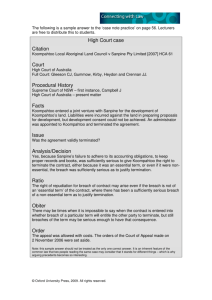

Cyber Crime Statistics

Data Under Siege

Global Cyber Event Heat Map

Cyber Event Type Composition by

Year

Cyber Events by Company Size

Number of

Employees

0 - 25

25 - 50

50 - 100

100 - 250

250 - 500

500 - 1,000

1,000 - 5,000

5,000 - 10,000

10,000+

Total

Event

Count

1,626

571

570

761

515

544

1,427

638

3,595

10,247

Percenta

ge

15.9%

5.6%

5.6%

7.5%

5.0%

5.3%

13.9%

6.2%

35.1%

100.0%

Cyber Litigation Frequency Index

700

600

Improper Collection

of Digital Data

500

400

Privacy Violations

300

200

Improper

Disposal/Distribution

Loss or Theft

(Printed Records)

100

0

2005

2006

2007

2008

2009

2010

2011

2012

2013

All

Privacy Violations

System/Network Security Violation or Disruption

Digital Data Breach, Loss, or Theft

Improper Disposal/Distribution, Loss or Theft (Printed Records)

Improper Collection of Digital Data

Data Under Siege:

Malicious Threats

Hackers, extortionists, disgruntled employees, fraudsters

Malware, spyware, spam,

Malware, short for malicious (or malevolent) software, is software used or programmed by

attackers to disrupt computer operation, gather sensitive information, or gain access to private

computer systems. It can appear in the form of code, scripts, active content, and other

software.[1] 'Malware' is a general term used to refer to a variety of forms of hostile or intrusive

software.[2]

Malware includes computer viruses, ransomware, worms, trojan horses, rootkits, keyloggers,

dialers, spyware, adware, malicious BHOs, rogue security software and other malicious

programs; the majority of active malware threats are usually worms or trojans rather than

viruses.[

Phishing, pharming

A: Both pharming and phishing are methods used to steal personal information from

unsuspecting people over the Internet.

Phishing typically involves fraudulent bulk e-mail messages that guide recipients to legitimatelooking but fake Web sites and try to get them to supply personal information like account

passwords.

Pharming tampers with the domain-name server system so that traffic to a Web site is secretly

redirected to a different site altogether, even though the browser seems to be displaying the

Web address you wanted to visit.

Data Under Siege

1992 – 2007, 2M unique malicious programs

2007 – 2009, 33.9M unique malicious programs

2010 hit new record 1.5 Billion (ump)

31% of IT specialist were unaware of most deadly

(ump)

87%, of system vulnerabilities were due to 3rd

party applications, Microsoft, Java, IT

infrastructure

“U.S. Code Cracking Agency Works as if Compromised” – Reuters News 12 16 2010

Global IT Security Risks Report, Kaspersky Lab 2012

Cyber Crime and Small Businesses

ATM skimming generates losses of $50 million

each year1

One in 20 adults is at risk of identity theft

One in 465 is a victim of identity theft

Average cost per compromised document: $214

• Not including civil damages and/or defense costs)

1 Electronic

Funds Transfer Agency

www.efta.org

Why are Small & Mid-market Businesses

considered to be at High Risk?

Cyber Crime and Small Businesses

Over 20% of small businesses have suffered a data

breach1

Number of attacks on rise, breach size declining, indicating

cybercriminals go after smaller targets e.g. small

enterprises (less security = easier attacks)

Malicious attacks (hacking or inside theft) constitute 40% of

recorded breaches in 2011

Visa reports 80% all card breaches arise from Level 4

merchants (those with fewer than 50 employees)

Each year, more than 10 million individual identity thefts

1 Poneman

Institute Study on Cyber Crime

Small Business Data Theft Risk Management Study

Threats: Not “If” but “When”

Non-Malicious Threats

Employee mistakes: Lost / stolen laptops and

portable devices

Application glitches

Network operation and “sharing” trends

Points of failure are now multiplied due to

outsourcing

Dependencies & data-sharing between biz

partners including cloud servers

Upstream & down stream vendors (ASPS,

partners, ISPs)

Methods of Fraud

What Are Thieves Looking For?

PII & Cardholder Data

Social security numbers, names and addresses

Health insurance applications

• Primary Account Number (PAN)

• CID number (this must never be stored)

• Sensitive authentication data = card use and cardholder’s

identity

Methods Include

• Compromised card readers

• Papers stored in unlocked filing cabinets

• Data held in a payment system database

• Hidden camera recordings entry of authentication data

• Secret “tap” on your company’s wired or wifi network

The Risk to Your Insureds

Disgruntled employees – non-disclosure

Loss of revenue, System crashes from hackers

Data Breach: Auto customer data, patient PII,

Your e-mail infects customers

Businesses utilize social media, e-marketing materials,

company blogs

Lack of knowledge & resources to respond to breach,

timely

The High Risk to Small and Mid-size

Accounts

(under 50 employees & < 10MM Gross Revenue)

Why are Small & Mid-market Businesses considered to be at

High Risk?

Hackers and thieves are targeting Small Businesses,

because:

• Small businesses typically lack the resources and expertise to

successfully fend-off – or even respond to – attacks

• Lack of a formal IT department means that Payment Card

Industry (PCI) Data Security compliance is particularly

challenging for small organizations

The Payment Card Industry Data Security Standard (PCI DSS) is a set of requirements designed to ensure that ALL

companies that process, store or transmit credit card information maintain a secure environment.

An attack or error of negligence could prove catastrophic for

the typical small business

“Over 20% of small businesses had already suffered a data breach…. small businesses do not have

adequate measures or remedies in place to protect themselves.”

- Larry Ponemon

Ponemon Institute

Small Business Data Theft Risk Management Study

Potential for Business Harm to Your Insured’s

Enterprise

What is the potential harm to your client’s enterprise?

Business fall-out can be severe (including negligence and breach)

Agency E&O / D&O

•

Failing to meet Payment Card Industry (PCI) rules or negligently managing PII

data

State statutory notification, fines and penalties

Fines and Penalties (liquidated damages)

Termination of ability to accept payment cards

Reduction in business, lost customers (20% likely)

Cost of reissuing payment cards ($100 per card VISA)

Fraud losses (see civil damages)

Legal costs, settlements, and judgments

Increase in compliance costs

Going out of business (i.e., breach exceeds net worth of company)

Joseph F. Bermudez, Esq.

Scott D. Sweeney, Esq.

Wilson Elser, LLP

October 8, 2014

Cyber Breaches and Liability

18

© 2014 Wilson Elser. All rights reserved.

Overview

•

•

•

•

Data Breach Overview

Data Breaches in the News

Life Cycle of a Breach

Are you Ready?

19

© 2013 Wilson Elser. All rights reserved.

Data Breach Overview

•

•

•

•

How do breaches occur?

Costs of a data breach

Legal liability for breaches

Data breach response and mitigation

20

© 2014 Wilson Elser. All rights reserved.

Data Breaches

Who Are the Victims?

•

•

•

•

•

•

Financial institutions

Retail and restaurant industries

Manufacturing, transportation, utilities

IT and professional services firms

Health Care organizations

Impact on larger organizations

21

© 2014 Wilson Elser. All rights reserved.

Data Breaches

Who Is Perpetrating Breaches?

•

•

•

•

•

Outsiders of the organization

Insiders of the organization

Business partners

Multiple parties

State (government) affiliated actors

22

© 2014 Wilson Elser. All rights reserved.

Data Breaches

How Do Breaches Occur?

•

•

•

•

•

•

•

•

Hacking

Insider wrongdoing

Human error

Network intrusion exploiting stolen credentials

Use of malware

Physical attacks

Leveraged social tactics such as phishing

Privilege misuse and abuse, including theft of IP

and corporate espionage

23

© 2014 Wilson Elser. All rights reserved.

Data Breach Response Costs

•

•

•

•

•

•

Avg. total organizational cost of breach ($5.8M)

Avg. detection costs ($417,700)

Avg. notification costs ($509,237)

Avg. remediation costs ($1,599,996)

Avg. lost business costs ($3,324,959)

$201 a record

Note: Figures do not include mega breaches in excess of

100,000 breached records

Source: Ponemon Institute 2014 Cost of Data Breach Study

24

© 2014 Wilson Elser. All rights reserved.

Other Breach Related Costs

• Litigation costs

– Consumer class actions

– Shareholder suits

– Government investigations and proceedings

• Impact on corporate finances

–

–

–

–

Cash flow

Loan covenants and credit

Shareholder value

Reputational injury and loss of business

25

© 2014 Wilson Elser. All rights reserved.

Data Breaches in the News

26

© 2014 Wilson Elser. All rights reserved.

Target Data Breach Overview

• Hackers used stolen credentials from a third

party vendor

• Inserted malware into the company’s

computerized payment systems

• Malware scraped credit card data

• Data breach compromised 40 million credit and

debt accounts

• Personal data of 110 million customers was

compromised

27

© 2014 Wilson Elser. All rights reserved.

Company’s Public Disclosures

12/19/13

• Company announced that hackers gained

unauthorized access to payment card data

• Affected credit and debit card transactions in

U.S. stores from 11/27/13 to 12/15/13

• Internal investigation of the data breach

• Retention of outside forensics firm

• Company also alerted authorities and financial

institutions

28

© 2014 Wilson Elser. All rights reserved.

Company’s Public Disclosures

1/13/14

•

•

•

•

CEO and Chairman apologized to customers

Provided status update on internal investigation

Malware removed

Company hired data security experts to investigate

causes of the breach

• Company was working with law enforcement

• Assured customers they would have “zero liability” for

fraudulent charges

• One year of free credit monitoring services

29

© 2014 Wilson Elser. All rights reserved.

Impact on Company’s Financials

• 5.5% decrease in sales in 4Q 2013

• “Meaningfully softer results” following news of

the breach

• 11% drop in stock price

• Reputational injury

30

© 2014 Wilson Elser. All rights reserved.

Data Breach Response Costs

• $61 million incurred in 4Q 2013 for data breach

response costs

• Amounts include

– internal investigation costs

– credit monitoring

– staffing call centers

• Company’s insurers agreed to pay $44 million

• Company will continue to incur breach related

costs for the foreseeable future

31

© 2014 Wilson Elser. All rights reserved.

Data Breach Lawsuits

•

•

•

•

•

80 civil lawsuits filed against company

Suits by customers

Suits by payment card issuing banks

Shareholder litigation against D&Os

Government investigations

– Federal Trade Commission

– SEC and DOJ

– 30 State Attorney Generals

32

© 2014 Wilson Elser. All rights reserved.

CFO Testifies Before U.S. Senate

• 2/4/14 – Company’s CFO testified before senate

committee

• On 12/12/13, DOJ alerted Company to “suspicious

activity”

• Internal investigation confirmed installation of malware

and potential theft of credit card data

• Company invested $5 million in a public education

campaign regarding cybersecurity

• Company launched a retail industry Cybersecurity and

Data Privacy Initiative

33

© 2014 Wilson Elser. All rights reserved.

Other Recent Data Breaches

•

•

•

•

•

•

•

•

•

Home Depot

Neiman Marcus

Advocate Healthcare

Twitter

Adobe

Facebook

Living Social

Evernote

Federal Reserve Bank

34

© 2014 Wilson Elser. All rights reserved.

Life Cycle of a Breach

• Triggering the Incident Response Team

• Making sure the right people / partners are part of the team

• Containment

• Have you stopped the “bleeding”?

• Remediation

• Have you taken steps to prevent this type of event from

occurring in the future?

• Identification of the Threat or Security Incident

• What just happened?

Notification – and beyond

Overview

You are part of a company that

operates retail stores throughout

the United States. Payment-card

and HR processing is handled by

your corporate offices for all

stores. The Company employees

approximately 20,000 employees.

Cyber Attack!

ATTACK!

What Just Happened?

•Your Company was the victim of a sql injection attack

against a web application that provided information on

customers who had purchased the Company’s

services. The hacker appears to have gained access t

o a database that was serving the web application.

•Question: What Do You Do?

Information Exposed

oThe initial investigation shows that the database contained

employees’ names, addresses, social security numbers,

driver’s license numbers, position, and bank account

information. The database has been operational for 5

years. The database appears to have stored cardholder

information for repeat customers.

oQuestion: Now what? Does this impact your initial plan of

action?

Monkey Wrench #1

You just learned that Brian Krebs, an online reporter who is

credited with breaking the story that Target had been breached,

and is followed by thousands of other publications, posted a story

on his blog that the Company appears to have been breached.

The story mentions that the Company failed to return phone calls

for two days.

Monkey Wrench #2

The CEO of the Company contacts you, and tells you that he just

received an e-mail from an unknown e-mail address, informing him

that this person has the personal information of the CEO and his

daughter, provides his driver’s license as proof, and threatens to

post it online unless the CEO pays a ransom.

Update From Investigation

The database contained a link to an application that was connected to

the Company’s payment processing system, which is centrally located at

the Company’s headquarters. The application automatically updated

information for repeat customers, but also allowed the hacker to

potentially access the payment card information of all customers,

exposing over 2 million credit cards.

Monkey Wrench #3

The FBI has just showed up at your door, and wants access to

your data center so it can image your computers and servers in

order to investigate the cyber attack.

Money Wrench #4

In the midst of your investigation, you receive an Inquiry from

regulatory agency requesting more information about the event,

asking for policies and procedures, and seeking a meeting.

Summary

Responding Quickly, But Effectively Matters

Know Who Your “Team” Members Are Before You Have An Event Internal And External

Training And Education Matters!

No Two Events Are Alike - Expect The Unexpected

Cyber Stress Test

Are you Prepared?

How many of the following does your company

have?

1.

Do you process or store credit cards for payments?

2.

Have you had a PCI compliance audit conducted or have you had any external assessment to

confirm you are compliant with the PCI standards?

3.

Do you store any of the following information about your customers or employees: social security

number, name and address, credit card or bank details?

4.

Do you maintain an active presence on any major social media sites (e.g.? Facebook, Twitter,

YouTube, Trip Advisor, etc.)?

5.

Do you store any business critical data or information on your systems (e.g. financial / accounting

records, client lists, claim data, etc.?)

6.

Do you use a voice over IP telephony system (VoIP)?

7.

Do you have any individuals within the business that can authorize online payments of more than

$5,000?

8.

Do you rely on any technology systems in order to collect payments from customers?

9.

Do you encrypt all data delivered to credit card vendor?

10. Do you rely on any third party systems in order to secure bookings

Mid-Markeet Business Owners Cyber Stress

Test

How many of the following does your company have?

Do you process or store credit cards for payments?

This function captures PII and exposes to hacking PII = contract damages ($100 per replaced

card) ($214 credit monitoring etc. per customer)

Have you had a PCI compliance audit conducted or have you had any external assessment to confirm

you are compliant with the PCI standards?

This is the legal test to legal liability if hacked. The vendor can hold credit equal to the potential

legal exposure and hold until issue resolved, includes charges for replacement of credit card

Do you store any of the following information about your customers or employees: social security

number, name and address, credit card or bank details?

HIPPA exposure – hurricane

Do you maintain an active presence on any major social media sites (e.g? Facebook, Twitter,

YouTube, Trip Advisor, etc.)?

Copyright Violations, Reputation damages – not covered by GL

Stress Test continued

Do you store any business critical data or information on your systems (e.g. financial / accounting

records, customer lists, customer reservations, etc?)

Release of business personal information without consent and PII

Do you use a voice over IP telephony system (VoIP)?

Easy access point for hackers, increase exposure to privacy violations

Do you have any individuals within the business that can authorize online payments of more than

$5,000?

Security control requirements are much greater if this is in practice

Do you rely on any technology systems in order to collect payments from customers?

Another method for hackers to access PII exposing owner to breach and contract damages

9. Do you encrypt all data delivered to credit card vendor?

This is an automatic violation of PCI standards and most state codes

10. Do you rely on any third party systems in order to secure bookings (e.g. Open Table?)

Up-stream data retention facilities / clouds, if breached by your stored data can infect others data

= legal exposure to large number of PII that are not your clients.

Best Solution

Risk Transfer &

Risk Management

How to Protect Your

Company’s Data

Comply with the golden 12 Rules

Goal

Rule

Build and Maintain a Secure

Network

Install and maintain a firewall configuration to protect data

Do not use vendor-supplied defaults for system passwords and other security

parameters

Protect Cardholder and

HIPPA Data

Protect stored data

Encrypt transmission of cardholder data and sensitive information across

public networks

Maintain a Vulnerability

Management Program

Use and regularly update anti-virus software

Implement Strong Access

Control Measures

Restrict access to data by business need-to-know

Develop and maintain secure systems and applications

Assign a unique ID to each person with computer access

Restrict physical access to cardholder data

Regularly Monitor and Test

Networks

Track and monitor all access to network resources and cardholder data

Maintain an Information

Security Policy

Maintain – and update – a policy that addresses information security

Regularly test security systems and processes

How to Protect Your

Company’s Data

Comply with the golden 12 Rules

Goal

Rule

Build and Maintain a

Secure Network

Install and maintain a firewall configuration to protect

Protect Cardholder

and HIPPA Data

Protect stored data

data

Do not use vendor-supplied defaults for system

passwords and other security parameters

Encrypt transmission of cardholder data and sensitive

information across public networks

Maintain a

Vulnerability

Management

Program

Use and regularly update anti-virus software

Implement Strong

Access Control

Measures

Restrict access to data by business need-to-know

Regularly Monitor

and Test Networks

Track and monitor all access to network resources and

Maintain an

Maintain – and update – a policy that addresses

Develop and maintain secure systems and applications

Assign a unique ID to each person with computer access

Restrict physical access to cardholder data

cardholder data

Regularly test security systems and processes

Recommended Cyber Coverage

What does System Damage &

Interruption cover?

This is first party cover that protects companies against their own losses resulting from damage to

data caused either deliberately by a malicious employee or hacker, or totally accidentally (the

infamous “fat finger”). The system interruption cover stems directly from this but is restricted to

malicious employees, hackers or computer viruses. This provides protection against loss of profits

arising directly from these perils.

What does Cyber & Privacy

Liability cover? (includes PCI

fines and penalties)

This provides liability coverage – including legal defense costs and indemnity payments – for claims

brought against you arising from a data security breach, whether through electronic means or

otherwise. This is provided on an “all risks basis”. The coverage is also extended to include liability

protection against claims arising from you spreading a computer virus or from your systems being

used to hack a third party.

What does Breach Response

cover?

This provides first party cover for the cost of complying with breach notification laws. Coverage is

also included for voluntary security breach notification, where this helps to mitigate adverse impact

upon the company’s brand or reputation. The coverage itself will pay for the legal costs of drafting a

breach letter, the cost of printing and posting the letter, credit monitoring costs, and forensic costs

that may be required to identify the extent of the breach.

What does Media Liability

cover? (limited to web site

unless add endorsement) PL

& GL duplicate cover

This provides comprehensive liability coverage including legal defense costs as well as indemnity for

damages and fines (where insurable). Essentially, this coverage protects against claims for intellectual

property rights infringement (excluding patent) and defamation arising from content published by

the company or on its behalf. This coverage also extends to social media and user generated content,

including company and employee blogs.

What does regulatory

privacy cover?

This provides coverage for the costs associated with defending yourself against a regulatory action

brought against you as a direct result of a privacy breach. This includes actions brought by federal

regulators such as the FTC and similar state or industry bodies. Coverage is also extended to include

fines and penalties that are issued as a result, where these are insurable by law.

Recommended Cyber Coverage Limits

System Damage & Interruption - (minimum $250k)

Regulatory Fines & Penalties – $1M limits

Privacy Breach Notification – $250k / $1M limits

Media Liability - $1M limits

PCI Fines & Penalties – $250k, $1M limit

Policy Review Questions

First & Third-Party Liability

Coverage for transmission of virus to third party and 3rd party to others

Copyright infringement from website

Forensic investigation covered as part of breach notification?

Coverage applies to both electronic and physical data breaches e.g. paper,

laptop, disks, PDA etc. ?

Coverage applies to both personal and company information? (IFI 1st Co)

Coverage applies to employee and customer information

Information in care custody or control of insured’s vendors include cloud

servers and paper records being transported?

Policy apply to accidental losses and leaks?

Does application require PCI compliance or encryption?

No insider exclusion?

Direct intentional attacks are covered is “wild viruses” those not specifically

targeting insured?

Liquidated damages and fines and penalties? Know position, provable court

Policy Review Questions

Media liability

Media Liability is valid anywhere in world?

Coverage extend to include social networking , emails, twitter? (PL & GL)

Coverage apply to user-generated content (opinion boards for feedback)

Extortion – no limit to threat method

Breach Response – Crisis Management

Policy apply to attorney fees to draft response to breach and related deliver costs?

Is credit monitoring included for individuals? (employees? )

Will policy provide options to notification methods?

Coverage include forensic investigation?

First Party business interruption

Forensic Investigation covered?

Do they offer contingent period after system restored?

Based on time system is down or a stated time period?

Wild & targeted viruses included ?

Loss of Reputation ?

Summary

Questions?

58

© 2014 Wilson Elser. All rights reserved.

Contact

Melissa Ventrone

Wilson Elser LLP (Chicago)

Phone: 312-821-6105

Email: Melissa.Ventrone@wilsonelser.com

Joseph F. Bermudez, Scott D. Sweeney

Wilson Elser LLP (Denver)

Phone: 303-572-5310; 303-572-5324

Email: Joseph.Bermudez@wilsonelser.com

Scott.Sweeney@wilsonelser.com

59

© 2014 Wilson Elser. All rights reserved.

Questions?