Economics Systems 121208 Stringfellow CMS

advertisement

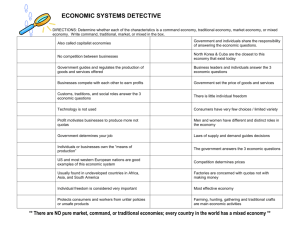

Terms to Know Free Market Command Traditional Mixed Capital Land Labor Natural Resources Entrepreneur Trade Barriers Tariffs Quotas Embargo Currency Exchange Specialization Why do we study Economics? The fundamental economic problem in any society is to provide a set of rules for allocating resources and/or consumption among individuals who can't satisfy their wants, given limited resources. Graphic Organizer In every nation, no matter what the form of government, what the type of economic system, who controls the government, or how rich or poor the country is, three basic economic questions must be answered. They are: What and how much will be produced? Literally, billions of different outputs could be produced with society's scarce resources. (Scarcity- In economics, scarcity is the problem of infinite human needs and wants, in a world of finite resources. In other words, society does not have sufficient productive resources to fulfill those wants and needs How will it be produced? There are many ways to produce a desired item. It may be possible to use more labor and less capital, or vice versa. It may be possible to use more unskilled labor to substitute for fewer units of skilled labor. For whom will it be produced? Once a commodity is produced, some mechanism must exist that distributes finished products to the ultimate consumers of the product. The mechanism of distribution for these commodities differs by economic system. Graphic Organizer What and How Much will be produced? Economics Questions For whom will it be produced? How will it be produced? While there are many terms that are used to describe the types of economies that exist in the world, most economists agree that there are four major types of economic systems. On the RIGHT side of your paper draw this chart, take up the whole page! TYPES OF ECONOMIC SYSTEMS Definition 1) Market economy 2) Command economy 3) Traditional economy 4) Mixed economy Associated Terms Examples in Practice Market economy An economic system in which individuals own and operate the factors of production. AKA: Free enterprise, Capitalism United States, Great Britain, Japan Command economy An economic system in which the government owns and operates the factors of production. AKA: Socialism, Communism Cuba, China, Laos Binder Question What is the difference between a Market Economy and a Command Economy? Traditional economy An economic system based upon customs and traditions. Economy is based upon agriculture and hunting. AKA: Non-Industrialized, Agrarian societies Chad, Haiti, Rwanda Mixed economy An economic system that has features of both market and command economies. In reality there are no pure market economies, nor are there any pure command economies. For example, even in the United States, where free enterprise reigns, the government plays a major role in the economy. Minimum wages, social security, and regulatory policies are examples of government involvement. In China, for example, some private ownership of businesses is allowed, however the government still maintains tight control over the factors of production and prices. While we could say that both the United States and China are mixed economies because they contain both market and command economic features, to do so would be misleading because the role that the respective governments play in the economy are quite different. TYPES OF ECONOMIC SYSTEMS 1) Market economy Definition Associated Terms An economic system in which individuals own and operate the factors of production. Free enterprise Capitalism 2) Command economy An economic system in which the government owns and operates the factors of production. 3) Traditional economy An economic system based upon customs and traditions. Economy is based upon agriculture and hunting. 4) Mixed economy An economic system that has features of both market and command economies. Examples in Practice United States Great Britain Japan Socialism Communism Cuba China Laos Non-Industrialized Agrarian societies Chad Haiti Rwanda Binder Question What type of Economy is in Japan? Answer: Market Gross domestic product (GDP) is one of the measures of national income and output for a given country's economy. GDP is defined as the total market value of all final goods and services produced within the country in a given period of time (usually a calendar year). Map of countries by 2007 GDP (nominal) per capita (IMF, April 2008). Factors of Production Land Labor Capital Resources Entrepreneur Land Land in economics comprises all naturally occurring resources whose supply is inherently fixed. Such as mineral deposits. In classical economics it is considered one of three factors of production (along with capital and labor). Labor (Human Capital) In economics, labor is a measure of the work done by human beings. There are theories which have created a concept called human capital (referring to the skills that workers possess, as in the education and training the workers have had). LFS Question 3-2-1 Give 3 examples of LAND in economics. Lists 2 FACTORS OF PRODUCTION. Provide 1 skill a worker might have. Capital In economics, capital or capital goods or real capital refers to items of extensive value, it can also be applied to the amount of wealth a person controls or is capable of controlling. In classical economics, capital is one of three (or four, in some formulations) factors of production. The others are land, labor and (in some versions) organization, entrepreneurship, or management. Goods with the following features are capital: It can be used in the production of other goods (this is what makes it a factor of production). It was produced, in contrast to "land," which refers to naturally occurring resources such as geographical locations and minerals. Natural resources There are 2 types of natural resources: Renewable and Nonrenewable. Natural resources include soil, timber, oil, minerals, and other goods taken more or less from the Earth. Both extraction of the basic resource and refining it into a purer, directly usable form, (e.g., metals, refined oils) are generally considered natural-resource activities. A nation's natural resources often determine its wealth in the world economic system, and in determining its political influence. In recent years, the depletion of natural resources has become a political and economic issue. This is of particular concern in rainforest regions, which hold most of the Earth's natural biodiversity. Conservation of natural resources is the major focus of natural capitalism, environmentalism, the ecology movement, and Green Parties. Some view this depletion as a major source of social unrest and conflicts in developing nations. Binder Question 3-2-1 List three renewable natural resources. List two non-renewable natural resources. Give one reason why natural resources are running out. Entrepreneur An entrepreneur is a person who has possession over a company, enterprise, or venture, and assumes significant accountability for the inherent risks and the outcome. Trade Barriers A trade barrier is a general term that describes any government policy or regulation that restricts international trade. The barriers can take many forms, including: quotas Tariffs Embargo Most trade barriers work on the same principle: the imposition of some sort of cost on trade that raises the price of the traded products. If two or more nations repeatedly use trade barriers against each other, then a trade war results. Economists generally agree that trade barriers are detrimental and decrease overall economic efficiency, this can be explained by the theory of comparative advantage. Tariffs A tariff is a tax on goods when they cross a national border. A "protective tariff" is intended to artificially inflate prices of imports and "protect" domestic industries from foreign competition. For example, a 50% tax on an imported machine raises the price from $100 to $150. Without a tariff, the local manufacturers could only charge $100 for the same machine; now they can charge $149 and make the sale. Quotas An import quota is a type of protectionist trade restriction that sets a physical limit on the quantity of a good that can be imported into a country in a given period of time. For example, a country might limit sugar imports to 50 tons per year. Quotas, like other trade restrictions, are used to benefit the producers of a good in a domestic economy at the expense of all consumers of the good in that economy. Embargo An embargo is the prohibition of trade with a certain country, in order to isolate it and to put its government into a difficult internal situation, given that the effects of the embargo are often able to make its economy suffer from the initiative. The embargo is usually used as a political punishment for some previous disagreed policies or acts, but its economic nature frequently raises doubts about the real interests that the prohibition serves. Currency Exchange Every country has a different kind of currency, or monetary system. Some examples of African money are the Egyptian pound, the South African rand, the Nigerian naira, and Chad’s franc (many of these will eventually be replaced by the African Union afro. An exchange rate is the price that one country’s currency has compared to another country’s currency. For example, one U.S. dollar is worth over one hundred Nigerian naira. Without an exchange rate, global trade would be impossible to conduct. Exchange rates change daily. The changes are based on factors like government stability and the strength of a country’s market. Specialization Specialization encourages trade and can be a positive factor in a country’s economy. Specialization focuses on the development and production of one product or service. Binder Learning Log Today I I learned… am still struggling with… Bibliography Everything You Need to Teach, The Middle East. InspirEd. 2000. Georgia Department of Education. Types of government Worksheets for Unit 2. 06/30/2007. Grade Seven GPS. Georgia Department of Education. September 2, 2008.