Jerry Pacheco

Executive Director – International Business

Accelerator

jerry@nmiba.com

Mexico Myths

‘Not a significant market, other than basic goods’

‘Continuous economic crises – no stability’

‘The peso is worthless, inflation is rampant’

‘Technological backwardness’

‘Industry is dominated by US-led maquiladoras’

‘Mexican culture is not conducive to business’

Corruption

Land of mañana

‘Mexico is a failed narco-state’

Myth: Mexico is too poor to be a significant

market for anything but basic goods

Reality:

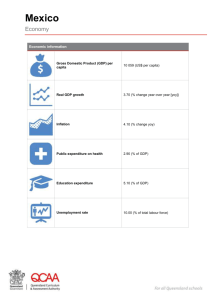

Mexico is a middle-income country

GDP per capita (nominal / PPP): $8,143 / $14,335

Comparable w/ Russia, Arg., Chile, Brazil, Turkey, Malaysia

2.5X the GDP/capita of China and 6X that of India

US GDP per capita - $45,989 / $ 45,989

China GDP per capita - $3,650 / $6,828

India GDP per capita - $1,134 / $3,270

2nd most important metropolitan market for high-end luxury

goods in the Americas – Mexico City

2nd largest market for US exports (exports to Mex > exports to

China + Japan)

Myth: Mexico has constant economic crises, the peso is

worthless, & inflation is high

Reality:

Cycle of econ. crises (1976, 1982, 1986-87, 1994) was

broken in 2000 and 2006

Avoided contagion from emerging market crises (e.g.,

Southeast Asia, Argentina)

Peso – stronger & more stable than US$ for much of the

last decade (until recently)

Inflation < 5%; investment grade status

Myth: Mexican industry is technologically backward and

dominated by US-led maquilas

Reality:

Technologically-advanced engineering & production

capabilities

Approximately 75 Mexican companies with revenues

greater than US$1billion/year

An emerging entrepreneurial culture

Dominant role of maquiladoras is limited to border

Myth: Mexican culture is not conducive to business:

corruption, land of mañana

Reality:

Carlos Fuentes:

“The Mexican mañana does not mean putting things off till

the morrow. It means not letting the future intrude on the

sacred completeness of today.”

Comparatively moderate levels of corruption & largely

limited to government

Workforce is young and ambitious, with strong

technical skills and work ethic

Important to recognize the distinction between social

culture and business culture

Myth: Mexico is now a failed narco-state

Reality:

Violence & insecurity are a huge social problem, but the

economic impact has been limited so far

Murder rate of US citizens (50/year for 1.5-2 million people) =

1/2 of Albuquerque’s or 1/4 of Houston’s.

Violence is concentrated in key states and among those involved

in drug trade, security, media

JP Morgan Chase estimates economic cost at 1.0-1.5% of GDP

Risk is no higher/lower than US in much of Mexico, just

different

Huge challenge as violence spreads to unexpected areas

(e.g., Monterrey) and in unpredictable patterns

Pre-Columbian Era to the Revolution

Mexico City – focal point of civilization

1500-100K inhabitants, 30M in Mexico

Architecture, irrigation, engineering, writing

Feudal system: caciques and tribute

1520-1810 – Spanish imperialist economy

Emergence of ‘la raza’

1810-1910 – Incomplete independence

Spanish control displaced, but feudal system remained

(caudillos)

The Revolution and the ‘Institutionalized

Revolution’

1910-Díaz regime ousted

Zapata, Villa, Carranza, Obregón

The revolution never ended, but was ‘institutionalized’

(PRI)

Economic system inspired by the revolution, but

patterned after colonialism

Unequal development; closed economy

Poor separation of firm & state

The Technocrats and ‘The Crisis’

Pattern of sexenio crises, 1976-1994

Curse of oil & ‘administering the abundance’

Technocrat Presidents

De la Madrid and the ‘lost decade’ (1980s)

Salinas de Gortari – renewed hope, shattered dreams,

and the ‘errors of December’ (1994)

Zedillo – weak but transformational sexenio

Economic Reforms, 1980-2000

Monetary & Fiscal Policy

Inflation reached 100+%, now under 5%

Balanced budgets

Deregulation & Privatization

Privatization of banks, rail, telcom, industry

FDI & franchise laws; increased transparency

Trade Liberalization – Export Orientation

GATT (max tariffs from 100% to 20%)

NAFTA (nearly all tariffs eliminated by 2003)

New Millenium: A ‘New’ Mexico?

Political change

2000 elections: Vicente Fox (PAN)

Political pluralism = Political Gridlock

PAN – Presidency

PRI – Senate and Chamber of Deputies

PRD – Governorships, Mayor of Mexico City

2006 elections: Felipe Calderon (PAN)

AMLO (Andres Manuel Lopez Obrador) factor

Gridlock continues

2012 elections: The Pena Nieto Administration

New Federalism in Estados Unidos Mexicanos

Increasing importance of states & municipios

Recent Economic Performance: Reasons for

Renewed Optimism

Consistent economic

growth 1995-2000

Change in GDP under

Zedillo:

1995: - 6.2%

1996: +5.1%

1997: +6.8%

1998: +4.9%

1999: +3.9%

2000: +6.6%

Stagnation under PAN,

2000-2010

Change in GDP under

Fox/Calderon:

2001: - 0.2%

2002: +0.8%

2003: +1.4%

2004: +4.2%

2005: +3.2%

2006: +4.8%

2007: +3.2%

2008: +1.8%

2009: -6.5%

2010: +5.4%

2011: +5.0%

Lingering Pessimism:

Limits to Development

Economic, Political & Social Issues:

‘So far from God, so close to the US…’

Dependence on oil, maquiladoras, exports

Unequal living standards/poverty/stagnant real wages

Drugs & drug-related violence, lawlessness

Immigration & the loss of human capital

The natural environment & water

Indigenous issues & Chiapas

Legal, tax, labor reforms

Deregulation (telecommunications, electricity)

Demographics

2010 Population: 110 Million (1950-25M)

93% literacy

Education expenditures: 6% of GDP (US-5%)

Life expectancy: 75 years (US-78 years)

Urbanization: 77% (US-82%)

Access to potable water: 83% (Korea-83%)

Physicians/100,000 people: 120 (US-280)

GDP/capita (nom/PPP) = $8,143 / $14,335

The Many Mexicos: Mexico City

The Capital: 25M inhabitants

Largest city in the world (along with others)

Distrito Federal: Seat of power for government,

financial, & corporate (domestic & MNCs) sectors

No manufacturing

Los chilangos:

Fast-paced, chaotic lifestyle

Cosmopolitan, status-conscious culture

The Many Mexicos: Monterrey

The Sultan of the North

Economic Sectors:

Traditional strength in heavy industry (steel, autos,

other manufacturing)

Migrating to new economy & higher value-added

Cemex, Alfa (Alpek, Nemak), Vitro, Femsa

Los regiomontanos:

The Texans of Mexico

The Many Mexicos: Jalisco

Guadalajara: The ‘Mexican’ City

Economy oriented toward:

Traditional sector (textiles, furniture, ceramics, tequila,

mariachis)

High-Tech (IBM, Acer, other telcom/IT equip)

Los tapatios:

Unique mixture of traditional Mexico with global

orientation

The Many Mexicos: The Border

2,000 miles and 10%-25% of Mexico’s pop.

Historical importance is less than the rest of Mexico

1940-1970: Border population grew 10 times

High interdependence with US economy

For better and for worse

Does NAFTA make the border more relevant, or less

relevant?

Manufacturing

Traditional strength: low-tech & heavy mfg.

Steel, auto parts, products for domestic market

Low-end export items (golf club shafts)

Transformation of Mexican manufacturing:

Emphasis on ISO 9000

Capital-intensive activities

From wire harnesses to electronics systems

Maquiladoras

~$120B/year in exports (half of Mexico’s total)

But only ~1/5 is value added

Highly cyclical, vulnerable to global econ.

Sectors: autos, electronics, apparel

Locations: Cd. Juárez, Tijuana, border

First-generation maquilas no longer competitive;

upgrading is essential

Non-Maquila Manufacturing

There’s more to manufacturing in Mexico than the

maquiladoras; line is blurring

IMMEX: new umbrella for maquila, Pitex (preferential

tariff treatment for temporary imports), other

The border v. the interior.

Border plants tend to follow ‘twin-plant’ model.

Plants in the interior are more likely to serve the

Mexican market.

Financial Sector

Tumultuous history of banking sector

Nationalized, then privatized, then bankrupt, then sold

off to foreigners; now stable

Bank loans as % of GDP: 40% in 1994, then down to

10%, now 15% (global average=136%)

Leading players are foreign: Citibank (Banamex), BBVA

(Bancomer), Santander (Serfin)

(Re-)Emergence of middle class creating

opportunity for insurance/other fin. Services

Interest rates have declined, but credit is still scarce for

the private sector

Credit available for consumption, not investments

Other Sectors

Energy: continued state dominance

Pemex (oil), CFE (electricity)

Tourism

Traditional emphasis on state-led developments

Transition to diffused & sustainable development

Professional services

Potential competitive advantage for NM & Hispanicowned firms

The ‘Grupos’

Importance of the diversified conglomerate

Relation to other emerging markets

Spin-offs of historic Grupo Monterrey

Alfa, Vitro, Femsa and many subsidiaries

Other important grupos:

Grupo Carso (America Movil, Telmex, Telcel, Prodigy,

Sanborns, CompUSA, Xignux, Frisco, banks)

Grupo Bimbo

Televisa

Entrepreneurship in Mexico

There’s more to Mexico than maquilas, PEMEX, and

the grupos.

Mexico has one of the highest rates of

entrepreneurship in the world.

Entrepreneurial activity is driven both by necessity and

by opportunity.

Economic activity in Mexico remains regionalized or

localized.

Growth in microfinance & social entrepreneurship

New Mexico and Old Mexico

Where does NM stand in terms of trade and

investment ties with Mexico?

NM exports are climbing to $500/year to Mexico (of

$1.5B/year to all countries)

Mexico is #1 market for NM in dollar terms and in number of

products.

NM imports about $652M/year from Mexico, of $2B total

35th state in exports to Mexico; 46th in exports to world

BUT, we must account for the nature of NM’s economy.

43rd state in terms of exports as % of GSP

20th state in terms of exports to Mexico as % of GSP

0

0