The RMB goes global case

advertisement

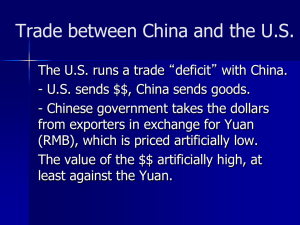

RMB going global Exhibit 1 The Gradual Revaluation of the RMB (1994–2010) Peg to dollar One currency rate Managed float Gradually appreciating Huge reserves Biggest financier of government bonds Growing confidence in world market Second largest economy, (though not in per capita terms) Problem area: Lack of convertibility Capital control 2004 establishing ‘Offshore RMB Market’ in Hong Kong, more and more trade handled in RMB (RQFII* and RQFLP* scheme) Market size grows steadily, rules lessened. Used as settlement currency at cross border trade Currency swaps with other economies: EU. UK, Astralia, Turkey, etc. This Allows other countries to finance their importers with RMB to be used at trade settlement Chile, Tanzania, and Nigeria diversified their reserves into RMB holding. *Renminbi Qualified Foreign Institutional Investor scheme (RQFII) **Renminbi Qualified Foreign Limited Partner Program (RQFLP), Used in international transactions freely and commonly Stable in value Credible monetary policy Credit worthiness US$ (60% held outside US), Euro€ (14% held outside EU as of 2010), £, yen, a) the size of the economy and the trade sector, b) the size of the financial market, c) capital account openness, and d) the stability of the economic and political conditions. These attributes are necessary, but not sufficient conditions for an international currency The yuan is currently traded in specific markets in specific ways Exhibit 2 Evolution of Trading in the Chinese Renminbi CNY-NDF market not important anymore since 2010 due to CNH market development The yuan is inevitably headed towards a major global role Exhibit 3 Necessary Medium for the Growth of the RMB A no brainer? the so-called “Dim Sum” bonds – bonds denominated in RMB and issued in Hong Kong - in 2007. 24 issues up to 2011. altogether 60 billion RMB denominated debt certificate in total. The yuan is rapidly developing along the Exhibit 4 A Score Board of criteria for an international currency status International Currency Status The Yuan Goes Global: Case Questions 1. 2. 3. 4. How does the Chinese government limit the use of the Chinese currency, the RMB, on the global currency markets? What are the differences between the RMB, the CNY, the CNH, and the CNY-NDF? Why was the McDonald’s bond issue so significant? Will – if ever – the RMB become a truly global currency? Case questions: answer 1. How does the Chinese government limit the use of the Chinese currency, the RMB, on the global currency markets? ▪ The Central bank of China is under the guidance of the Polit bureau ▪ All trading inside china between the RMB and foreign currencies, is conducted according to Chinese regulations. License needed. ▪ On shore and off shore market not freely connected. Case questions: answer 2. What are the differences between the RMB, the CNY, the CNH, and the CNY-NDF? ▪ CNY. This is the trading of the Yuan or RMB in the onshore market. This is a highly regulated market ▪ CNH. This is trading of the RMB in the Hong Kong market – “offshore”. This market, however, is showing signs of increasing regulatory release contributing to rapidly increasing currency exchange volumes. ▪ CNY-NDF. NDF: Non deliverable forward contracts. These are forward contracts, traded in the Hong Kong offshore market. The non-deliverable forwards are not important as of now, due to the rule changes that RMB settlement is allowed as of 2010. 3. Why was the McDonald’s bond issue so significant? ▪ The McDonald's bond was the first issue denominated in RMB by a non-financial non-Chinese firm in the global market at the Dim Sum Bond Market ▪ Although small in size, roughly $30 million, the issue has significant signaling effect: for companies to both operate and fund their business growth in Chinese RMB. ▪ The McDonald’s issuance was followed in November 2010 by a larger $150 million RMB-bond by Caterpillar Corporation (US), and in January 2011 by a CNY 500 million ($75.9 million) issuance by the World Bank. 4. Will the RMB become a truly global currency? ▪ The primary impediment to the RMB’s growth as a global currency are the capital market restrictions, on shore off shore differences, and residents and non residents treatment. ▪ The Chinese government has made it very clear that it has no ambition to become an international currency, particularly as a reserve currency. ▪ Etc. The use of RMB in trade is limited to small portion of the total trade with China. Countries who accepted RMB as payment intend to use RMB to hedge their RMB exposure. Not for ‘store of value’ (reserve currency) purposes per se.