State of the Wind Industry – by Denise Bode

advertisement

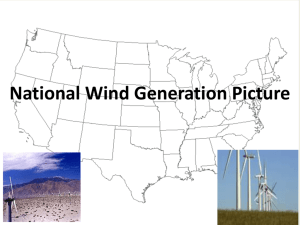

State of the Wind Industry Denise Bode CEO American Wind Energy Association American Wind Energy Association (AWEA) • Founded in 1974 • More than 2,500 business members • Wind project developers • Wind turbine manufacturers • Component manufacturers: towers, blades, gears • More than 8,000 parts in a turbine • www.AWEA.org provides extensive info on wind Perspective Global Competition • At least 37 nations have mandatory renewable energy requirements U.S. Wind Power Installations MW of Wind Installed Total Installation in 3Q 2009: 1,649 MW Source: AWEA Total Installation in 2009: 5,800 MW Total U.S. Installation through 3Q 2009: 31,100 MW Vision for the Future 20% Wind Energy by 2030 • U.S. Department of Energy: “The U.S. possesses sufficient and affordable wind resources to obtain at least 20% of its electricity from wind by the year 2030.” Wind Project Development 46 states would have wind development by 2030 under the 20% Vision Source: U.S. DOE, 20% Wind Energy by 2030 Job Projections Under 20% Report • Over 500,000 total jobs would be supported by the wind industry • In 2008, wind industry added 35,000 new jobs Source: U.S. DOE, 20% Wind Energy by 2030 Wind Manufacturing Facilities Across the U.S. • 55 manufacturing facilities opened, expanded or announced in 2008 • Wind industry now employs 85,000 in U.S. Major facilities online prior to 2008 All new online in 2008 – 2Q 2009 Announced facilities How We Get There Policy Timeline for Wind – Looking Ahead Proposed RES PTC for Wind Grant in lieu of ITC 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 Bonus Depreciation Policy Timeline for Wind – In Perspective Price-Anderson Act Credit for Non-Conventional Fossil Fuel Intangible Drilling Costs Percent Depletion Allowance Proposed RES PTC for Wind Grant in lieu of ITC 2020 2010 2000 1990 1980 1970 1960 1950 1940 1930 1920 1910 Bonus Depreciation for Wind National Renewable Electricity Standard • A strong 25% by 2025 RES would create: • 8-fold increase in homegrown renewable energy – from 28,000 MW to 248,000 MW • 297,000 new jobs • $13.5 billion in income to farmers, landowners, and ranchers • $11.5 billion in new local tax revenue • $64.3 billion savings from lower consumer expenditures • All at no cost to the taxpayer Source: Union of Concerned Scientists, 2009 25% RES by 2025 20% RES by 2021 with 5% EE 600 20% by 2021 with up to 8% EE (House Bill, H.R. 2454) 500 15% with 4% EE (Latest Senate Proposal) Existing State RPS 400 300 200 100 2021 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 0 2009 Additional Renewable Generation (billion kWh) Additional Renewable Generation Required to Meet RES Scenarios Compared to State RES Programs, Post-2009 Conceptual Vision: Green Power Superhighways Wind Power in Queues (MW) Washington 5,831 Oregon 9,361 Montana 2327 Idaho 446 Wyoming 7,870 Nevada 3,913 North Dakota 11,493 South Dakota 30,112 Nebraska 3,726 Utah 1,052 California 18,629 Arizona 7,268 Colorado 16,602 New Mexico 14,136 Kansas 13,191 VT 155 Minnesota 20,011 NH 396 Wisconsin 908 Iowa 14,569 Michigan 2,518 New York 8,000 Penn. 3,391 Indiana Ohio Illinois 8,426 3,683 WV 16,284 1,045 Missouri 2,050 Oklahoma 14,677 Arkansas 210 Texas 63,504 Maine 1,398 VA 820 RI 347 MA 492 NJ 1416 DE 450 MD 810 Under 1000 MW 1,000 MW-8,000 MW Over 8,000 MW Total 311,155 MW Adapting Power Grid to Accommodate Wind • Wind is an energy resource, not a capacity resource • ‘Reliability’ concerns often founded on serious misunderstandings of how grid operates, how wind projects fit into system operations • Wind power output is ‘variable,’ not ‘intermittent’ • Wind forecasting plays key role today, will play increasingly important role in future • There is a cost to managing wind’s variability – depends upon system’s characteristics, but is generally low • Many wind integration studies have been performed in US, EU Thank you! More information : www.awea.org | 202-383-2500 | windmail@awea.org www.awea.org/events