Slide 1

FastFacts

Feature Presentation

January 16, 2014

To dial in, use this phone number and

participant code…

Phone number: 888-651-5908

Participant code: 182500

To participate via VoIP…

You must have a sound card

You must have headphones or

computer speakers

© 2012 The Johns Hopkins University. All rights reserved.

Slide 2

Today’s Topic

We’ll be taking a look at…

Policies and Procedures for Classifying,

Engaging, and Paying Independent

Contractors

Slide 3

Today’s Presenter

Julia J. Buick

Assistant Tax Director, JHU

Place picture of Presenter

Name here

Slide 4

Session Segments

Presentation

Julia Buick will address policies and procedures for engaging

independent contractors.

During Julia Buick’s presentation, your phone will be muted.

Q&A

After the presentation, we’ll hold a Q&A session.

We’ll open up the phone lines, and you’ll be able to ask

questions.

Julia Buick, David Thompson (JHU Tax Office), Jennifer Hipp

(Purchasing), Mark Meyerer (Accounts Payable Shared Services),

and Steve Scholz (Office of International Business Support) will

answer as many of your questions as time allows.

Slide 5

Contact Us

If you would like to submit a question during the presentation or if

you’re having technical difficulties, you can email us at:

fastfacts@jhu.edu

Slide 6

Survey

Survey

At the end of this FastFacts session, we’ll ask you to complete a

short survey.

Your honest comments will help us to enhance and improve

future FastFacts sessions.

Slide 7

How To View Full Screen

Slide 8

Policies and Procedures for

Classifying, Engaging, and Paying

Independent Contractors

Slide 9

Agenda

Independent contractor news

Classification: Independent contractor vs. employee

Domestic vs. foreign independent contractor

JHU policies for engaging independent contractors

JHU procedures for engaging independent contractors

Engaging current & former JHU employees as independent

contractors

Key forms and documents needed to process independent

contractors

Key contact information for questions relating to independent

contractor processing

Slide 10

Independent Contractor News

Policy and Procedure News

The Independent Contractor Policies and Procedures have been updated by the

Controller’s Office and will be posted on the Finance website by the end of January

2014. Please note that there have been no substantive changes to either the policies

or the procedures. The policies and procedures document was refreshed and

reorganized to make it more user-friendly to the departments. Please be sure to

familiarize yourself with this updated document.

Independent Contractor Certification (ICC) Form News

In addition, the Independent Contractor Certification (ICC) form was also updated to

streamline the determination process. The current ICC form does not ask all of the

questions necessary to make an accurate and complete determination, making it

necessary for the Tax Office to gather additional information from the departments via

email and phone calls.

Please note that the updated ICC Form requires DBO signature before

submission. This was added to streamline the DBO approval process.

If you have any question, please email: IndependentContracts@jhu.edu

Slide 11

Classification: Independent Contractor vs. Employee

Definition of Independent Contractor

No bright line test; facts and circumstances based on the “totality of the

relationship.”

In general, an individual with complete “control” and direction over how

work is completed.

Control refers to the result to be accomplished by the work and also the

means and details by which the result is accomplished.

Work outside usual course of business of the university.

Expert or specialty work not performed by current university employees.

Independent contractors responsible for their own taxes (no withholding or

employer payroll tax responsibility).

Independent contractors not covered by Maryland Workers Compensation

law or Affordable Care Act.

Independent contractors not eligible for university benefits.

Students are never eligible for independent contractor status.

Paid through Accounts Payable.

Slide 12

Classification: Independent Contractor vs. Employee

Definition of an Employee

An individual performing services for the university where the university has

the right to control the individual’s results as well as the details and means

by which that result is accomplished.

Employees are required to be paid through JHU payroll.

Employees are subject to withholding and JHU is responsible for

employment taxes on their wages.

Individuals engaged/hired as employees must be processed through

Divisional Human Resources to ensure that they are appropriately set up as

employees.

Individuals engaged/hired as employees are likely covered by Maryland

Workers Compensation law, the Affordable Care Act, and university benefits

depending on their hours and other factors.

Certain worker types are always hired as employees, such as faculty.

Slide 13

Classification: Independent Contractor vs. Employee

Determination: Independent Contractor or Employee?

IRS Revenue Ruling provides the primary guidance (Twenty Factors) for

determining whether a worker is an independent contractor or an

employee.

Twenty factors; the degree of importance/weight of each factor depends on

the occupation and factual context in which the services are performed.

Twenty factors fall into one of three general categories of facts:

Behavioral Facts (i.e., does university control the worker or provide

instruction?)

Financial Facts (i.e., reimbursement of expenses, structure of payment,

whether university provides supplies or space for work)

Type of Relationship (i.e., is there an on-going relationship, is work

performed a key aspect of university business or related to JHU’s

mission)

Slide 14

Classification: Independent Contractor vs. Employee

The Twenty Factors

1. Worker must comply with JHU instruction

about when, where, and how to do work.

2. Worker receives training by JHU.

3. Worker provides services to JHU that are

integrated into JHU programs and operations.

4. The services must be rendered personally.

5. JHU hires, supervises, and pays those assisting

in the work.

6. There is a continuing relationship between JHU

and the worker.

7. JHU sets the hours that the worker will be

working.

8. Work for JHU will require a full-time schedule

for the worker.

9. Work is performed on JHU premises.

10.JHU determines the order and sequence of the

work.

11. JHU requires worker to submit regular oral or

written reports.

12. JHU pays worker by hour, week, or month.

13. JHU reimburses for business and travel

expenses.

14. JHU furnishes tools and materials for the job.

15. Worker not investing in own facilities.

16. Worker not subject to risk of economic loss on

the engagement.

17. Worker only working for JHU (no other clients).

18. Worker not marketing services or making

services available to the public.

19. JHU has right to discharge worker.

20. Worker has right to terminate without incurring

liability.

A “yes” response indicates the factor favors an employer-employee relationship. A “no” response indicates the

factor favors independent contractor status.

Slide 15

Classification: Independent Contractor vs. Employee

“Totality of the Relationship”

All of the facts and circumstances are reviewed and the entire

relationship between JHU and the individual is weighed.

Although JHU may, in good faith, determine that a worker is an

independent contractor, an IRS agent may reach a different

conclusion by weighing the twenty factors differently.

Additionally, the IRS will focus on the intent and the substance of

the work arrangement.

Slide 16

Classification: Independent Contractor vs. Employee

Importance of Proper Classification

Proper classification of JHU workers is incredibly important to

ensure university compliance with federal, state, and international

income tax and employment laws.

Classification is also important to ensure university compliance with

Department of Labor/ERISA laws (employee benefits) and the

Affordable Care Act.

Penalties to the university if worker is misclassified as independent

contractor.

Worker classification is a key area during IRS exams.

IRS regularly launching payroll targeted audits to ensure proper

classification.

Worker classification is key issue among our peers.

Slide 17

Domestic vs. Foreign Independent Contractor

TIP! Different forms and processes are applicable for foreign

independent contractors. So before you begin processing, know

whether your potential contractor is domestic or foreign.

“Domestic” independent contractors are individuals providing

services to the university within the United States.

“Domestic” independent contractors MUST be U.S. citizens or legal

permanent residents (i.e., green card holders) who are legally

permitted to provide services within the United States.

“Foreign” independent contractors are individuals providing services

to the university in a foreign country.

“Foreign” independent contractors may include United States

citizens or foreign nationals.

Slide 18

Domestic vs. Foreign Independent Contractor

Criteria used for classifying domestic independent contractors is

useful framework for determining if a foreign worker should be an

independent contractor or employee.

However, each country has its own unique laws so the Office of

International Business Support (OIBS) will need to make a

determination on any contract over $5,000.

Individuals engaged as independent contractors in a foreign country

will likely require work authorization from the foreign country’s

immigration office.

Prior to the engagement of any foreign independent contractor, the

department should obtain proof that the individual has obtained

necessary work authorization to provide services in the proposed

country.

Slide 19

JHU Policies for Engaging Independent Contractors

Domestic Independent Contractors: Engagements $5,000 and Higher

Definition: Contracts (or group of contracts) with domestic independent

contractors that will reach $5,000 or higher in a 12-month period.

Tax Office Determination of Worker Status (determination letter) is required

to set up P.O. or make any payments.

Tax Office determination MUST be obtained by the department prior to the

commencement of any work by the proposed independent contractor.

Foreign Independent Contractors: Engagements $5,000 and Higher

Definition: Contracts (or group of contracts) with foreign independent

contractors that will reach $5,000 or higher in a 12-month period.

Tax Office coordinates with Office of International Business Support (OIBS)

for Foreign Determination of Worker Status (determination letter).

OIBS determination MUST be obtained by the department prior to the

commencement of any work by the proposed independent contractor.

Slide 20

JHU Policies for Engaging Independent Contractors

Domestic & Foreign Independent Contractors: Engagements <$5,000

Contracts/Engagement/Cost under $5,000 for a 12 month period.

Determination from Tax Office/OIBS NOT required.

“Short Form Independent Contractor Agreement” required to be provided to

Accounts Payable Shared Services before any work commences.

TIP! How do I know if my independent contractor has exceeded

$5,000 in a 12-month period?

Effective 2014, Accounts Payable Shared Services (APSS) is running quarterly

reports to monitor payments to independent contractors. If a particular

independent contractor has exceeded the $5,000 threshold, then APSS will

send an email to the department administrator and DBO informing them that

the independent contractor must go through the independent contractor

determination process before any additional payments will be made to the

vendor. The vendor number for the independent contractor will be blocked so

that no future payments can be made until the certification process is

complete.

Slide 21

JHU Policies for Engaging Independent Contractors

Services Exempt from Independent Contractor Review

Transaction Type

IC Certification

Required?

Purchase Order

(PO) Required?

Method of

Payment

Contractual

Agreement Required?

Single Payment

Engagements < $5,000

(Domestic and

Foreign)

No

No

Online Payment

Request

Yes - Short Form

Independent Contractor

Agreement

Study Participant

No

No

No

Caterer

No

No

Online Payment

Request

Vendor Invoice or

Online Payment

Request

Special Event/

Entertainment

No

No

Vendor Invoice or

Online Payment

Request

Depends on

scope of engagement

Lecturer/Honorarium

No

No

No

Athletic

Official/Referee

No

No

Online Payment

Request

Online Payment

Request

Royalty Fees

No

No

Online Payment Request

No

Gifts, Prizes, and

Awards

Non-Employee

Reimbursements**

No

No

Online Payment Request

No

No

No

Online Payment Request

No

Depends on

scope of engagement

Yes - Short Form

Independent Contractor

Agreement

Slide 22

JHU Policies for Engaging Independent Contractors

Engaging JHU Employees as Independent Contractors

Employee: If the proposed independent contractor is a current or

former university employee (including retirees) and is providing a

service that is related or similar to current or past work, the

individual will generally be classified as an employee and will be

paid through the payroll system.

Independent Contractor: If the current university employee or

former employee is providing a service that is significantly different

than current or past work, the individual will be reviewed to see if

he or she meets the qualifications for independent contractor

certification.

Slide 23

JHU Procedures for Engaging Independent Contractors

IMPORTANT! To ensure that the Tax Office is

positioned to make timely and appropriate

determinations, the requesting department must

submit an accurate and complete Independent

Contractor Certification (ICC) form PRIOR to the

commencement of ANY work under the contract.

Slide 24

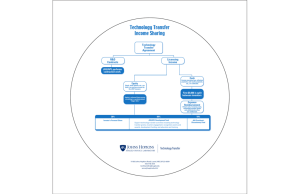

JHU Procedures for Engaging Independent Contractors

Flow Chart of Procedures for Independent Contractors

START

Department complete Short Form

Independent Contractor Agreement

(ICC Short Form)

YES

Is the contract expected to exceed $5,000 in a 12 month period?

NO

Is Vendor set up in

Vendor Master File (SAP)

Foreign

Domestic

Is the proposed independent

contractor domestic or foreign?

Department obtain W-9/W-8BEN

from vendor and complete

Vendor Data Entry Sheet. Then

email all documents to

Purchasing (or APSS for

contracts under $5,000). (Allow

3 business days for set up.)

Complete

Domestic ICC

form & submit

to Tax Office

Complete

International ICC

form & submit to

Tax Office

No

Determination of Worker Status:

“Approved Independent Contractor”?

Contact Divisional Human Resources

Department to set up employment

Yes

Complete/obtain

Independent

Contractor

Agreement

Department initiate

SAP Online Payment

Request (FV 60)

(Attach ICC Short

Form)

(Over $5,000) Department submit SAP

Shopping Cart to Purchasing to initiate

PO. (Attach Determination and

Independent Contractor Agreement.)

Process Goods Received & email invoice to APSS

APSS will process payment upon receipt of invoice

APSS

review/approve

SAP Online

Payment Request

Slide 25

JHU Procedures for Engaging Independent Contractors

Procedures for Engagements $5,000 and Higher

Step 1: Determine if the proposed contractor is domestic or foreign; this will

determine the next step.

Step 2A (Domestic): Complete Domestic Independent Contractor Certification form

(ICC form).

Step 2B (Foreign): Complete the International Independent Contractor Certification

form (International ICC form).

Step 3: Submit the ICC form/International ICC form to the Tax Office via email:

independentcontracts@jhu.edu or fax: (443) 997-8688.

DON’T FORGET! to submit the resume and/or CV with the ICC/IICC!

Step 4: Tax Office/OIBS (via the Tax Office) will issue (via email) a “Determination of

Worker Status” (“determination” letter) back to the department.

Step 5A: If the Determination of Worker Status is an Approval of Independent

Contractor Status, the department is ready to proceed to purchasing. (See next

slide.)

Step 5B: If the Determination of Worker Status is a Denial of Independent Contractor

Status, the department should contact the Divisional Human Resources Department

to set up employment.

Slide 26

JHU Procedures for Engaging Independent Contractors

Procedures for Engagements $5,000 and Higher – Continued

Step 6: Check SAP to determine if the vendor is set up in the Vendor Master File.

Step 7A: If the vendor is domestic and does not exist in SAP, the department will first

need to obtain a W-9 from the vendor and complete the Vendor Data Entry Sheet.

Both of these documents plus the determination letter should be emailed to

purchasing@jhu.edu. Please allow 3 business days for set up.

Step 7B: If the vendor is foreign and does not exist in SAP, the department will first

need to obtain a W-8BEN and International Banking Wire form from the vendor and

complete the Vendor Data Entry Sheet. All three of these documents plus the

determination letter should be emailed to purchasing@jhu.edu. Please allow 3

business days for set up.

Step 8: Once the vendor is set up in SAP, Purchasing Services will email the requester

the vendor number.

Step 9: The department should complete/obtain the appropriate Independent

Contractor Agreement (see later slide).

Slide 27

JHU Procedures for Engaging Independent Contractors

Procedures for Engagements $5,000 and Higher – Continued

Step 10: Once the vendor is set up in SAP, the department should submit an SAP

shopping cart to Purchasing to initiate a Purchase Order.

DON’T FORGET! to attach the Determination Letter, Independent Contractor

Agreement, and appropriate documentation summarizing the basis for vendor

selection and cost reasonableness.

Step 11: After review, Purchasing Services will sign the Independent Contractor

Agreement and issue a Purchase Order.

Step 12: The department should then confirm goods and services in SAP.

Step 13: The department or independent contractor should email Accounts Payable

Shared Services (APSS) the invoice (apssc@jhmi.edu) for payment.

TIP! Do not confirm goods through ECC.

TIP! The Independent Contractor Agreement is different from the Independent

Contractor Certification form.

Slide 28

JHU Procedures for Engaging Independent Contractors

Procedures for Engagements under $5,000

Step 1: Department completes Short Form Independent Contractor Agreement (ICC

Short Form).

Step 2: Department checks SAP to determine if the vendor is set up in the Vendor

Master File.

Step 3A: If the vendor is domestic and does not exist in SAP, the department will first

need to obtain a W-9 from the vendor and complete the Vendor Data Entry Sheet.

Both of these documents should be emailed/faxed to Accounts Payable Shared

Services (APSS). Please allow 3 business days for set up.

Step 3B: If the vendor is foreign and does not exist in SAP, the department will first

need to obtain a W-8BEN and International Wire form from the vendor and complete

the Vendor Data Entry Sheet. All three of these documents should be emailed/faxed

to Accounts Payable Shared Services (APSS). Please allow 3 business days for set

up.

Slide 29

JHU Procedures for Engaging Independent Contractors

Procedures for Engagements under $5,000 – Continued

Step 4: Once set up in SAP, department can initiate an Online Payment

Request (FV 60).

DON’T FORGET! to attach the Short Form Independent Contractor

Agreement and corresponding invoice to the Online Payment Request.

Please note that the Short Form Independent Contractor Agreement is

the appropriate agreement for both domestic and foreign independent

contractors when the total cost of the engagement does not exceed

$5,000 in a 12-month period.

Slide 30

JHU Procedures for Engaging Independent Contractors

Services Generally Classified as Employee

Instructors and Lecturers

Academic Services (advisors, tutors, athletic coaches, and trainers)

Accounting and Financial Services (budget analysts and internal auditors)

Administrative/Management Services (directors, managers, supervisors, and

coordinators)

Clinical/Research Services (physicians, scientists, therapists, and lab

technicians)

Information Technology Services (computer operators and systems

administrators)

Library Services (librarians and curators)

Support Services (ground maintenance and security)

Rehires (anyone who was previously employed)

Slide 31

JHU Policies for Engaging Independent Contractors

Services Generally Classified as Independent Contractor

Specialty services

Conservation treatment of archaeological

artifacts

Photographic services

Book designer

Copyeditor/proof reader

Website designer

Certified registered nurse anesthetist (limited

basis to fill operating room schedules)

Translator

Statistician

Video production services

Telescope repair services

Graphic design services

Message therapy services

Consultant/expert

Advisor on analyzed crime data

Specialized accounting services

Specialized legal services

Management consulting (specified

project/assignment with a finite duration)

Writer for a specified topic (expert in the field)

Executive search services

Professional Development consultants

(instructors/trainers)

Business plan development services

Evaluation services

Physician supervisors

Slide 32

Key Forms and Documents

PLEASE REVIEW the Independent Contractor Policies and Procedures. They

can be found on the JHU Finance website under the department of Accounts

Payable:

http://finance.jhu.edu/policy_procedures/dept_policy_procedures.html

Key Documents

Independent Contractor Certification (ICC) Form – Completed by department and

submitted to Tax Office for contracts over $5,000. Used by Tax Office to make

determination as to whether the worker should be an IC or EE. (Link:

http://ssc.jhmi.edu/supplychain/forms/jhu_forms/icc.pdf )

International Independent Contractor Certification (IICC) Form – Completed by

department and submitted to Tax Office/OIBS for contracts over $5,000. Used by

OIBS to make determination as to whether the worker should be an IC or EE. (Link:

http://ssc.jhmi.edu/supplychain/forms/jhu_forms/international_independent_contract

or_certification_interactive.pdf

Determination of Worker Status – a.k.a. “Determination Letter.” Issued by Tax

Office/OIBS after review of the ICC/IICC form. Required before any work commences

or payment issued for contracts over $5,000. (No link. This is issued by the Tax

Office/OIBS).

Slide 33

Key Forms and Documents – Continued

Key Documents – Continued

Short Form Independent Contractor Agreement – Completed by department and

submitted to APSS via Online Check Request before payments on contracts less than

$5,000 in a 12-month period. (Link:

http://ssc.jhmi.edu/supplychain/forms/jhu_forms/ica_short.pdf )

Independent Contractor Agreement – Should be used when a project is for a fixed

duration, a period of no more than 12 months, the services are $5,000 or greater and

less than $50,000, and when no intellectual property, computer software, or web

pages are expected to be produced. (Link:

http://ssc.jhmi.edu/supplychain/forms/jhu_forms/ica.pdf)

Master Consulting Services Agreement – Should be used when the cost of the project

exceeds $50,000 or when intellectual property (other than computer software and

web pages) is produced as a result of the hire or for projects of longer duration.

(Link: http://ssc.jhmi.edu/supplychain/forms/jhu_forms/mcsa.pdf )

Independent Computer Technology Services Agreement – Should be used when

computer software or web pages are expected to be produced. (Link:

http://ssc.jhmi.edu/supplychain/forms/jhu_forms/itcsa.pdf )

Slide 34

Key Forms and Documents – Continued

Key Documents – Continued

International Independent Contractor Agreement – Should be used when a foreign

independent contractor is engaged by the university. (Link:

http://ssc.jhmi.edu/supplychain/forms/jhu_forms/ic_international_ic_agreement.pdf)

Vendor Data Entry Sheet – Used to provide Purchasing/Accounts Payable Shared

Services with information necessary to set up a vendor in SAP. (Link:

http://ssc.jhmi.edu/accountspayable/DataFiles/VendorAddChange.pdf )

Slide 35

Key Contact Information

Questions Regarding:

Domestic Independent Contractor

Certification Forms

Questions Regarding:

Independent Contractor Agreements,

Shopping Carts, Purchase Orders, or

Vendor Set Up ($5,000 or greater)

Call/Email

Call/Email

Questions Regarding:

Foreign Independent Contractors

Email: independentcontracts@jhu.edu

Call: (443) 997-8688

Purchasing Services

Email: purchasing@jhu.edu

Call: (443) 997-1000

Call/Email

Accounts Payable Shared

Services

Call/Email

Office of International

Business Support

Questions Regarding:

Short Form Independent Contractor

Agreements, Vendor Set-up (under

$5,000), or Payment Matters

Tax Office

Email: apssc@jhmi.edu

Call: (443) 997-6688

Email: independentcontracts@jhu.edu

Call: (443) 997-8688

Slide 36

Conclusion

For contracts over $5,000, departments must first obtain a

“Determination of Worker Status” from the Tax Office/OIBS before

any work begins.

Please note that foreign independent contractors with contracts

over $5,000 in a 12-month period require the completion of the

International ICC form, not the domestic ICC form.

Please review the new and improved Independent Contractor

Policies and Procedures located on the Finance website at

http://finance.jhu.edu/policy_procedures/dept_policy_procedures.html.

Please direct questions to the appropriate departments (i.e., Tax,

Purchasing, Accounts Payable) to ensure the most timely response.

(See Key Contact slide.)

Slide 37

Q&A

We’re going to open the phone lines now!

There will be a slight pause, and then a recorded voice will provide

instructions on how to ask questions over this conference call line.

We’ll be answering questions in the order that we receive them.

We’ll also be answering the questions that were emailed to us

during the presentation.

If there’s a question that we can’t answer, we’ll do some research

after this session, and then email the answer to all participants.

Slide 38

Thank You!

Thank you for participating!

We would love to hear from you.

Are there certain topics that you would like us to cover in future

FastFacts sessions?

Would you like to be a FastFacts presenter?

Please email us at: fastfacts@jhu.edu

Slide 39

Survey

Before we close, please take the time to complete a short survey.

Your feedback will help us as we plan future FastFacts sessions.

Click this link to access the survey…

http://connect.johnshopkins.edu/fastfactssurvey/

Thanks again!