17_accounting standard

advertisement

ACCOUNTING STANDARD – 20

EARNINGS PER SHARE

By :

CA Chandrashekhar

Shetty S

B.Com, PGDCA, PGDFM, DISA, ACS, ACWA, FCA

DISCUSSION ON :

- Why EPS ?

- For Whom EPS ?

- What is EPS ?

- How EPS ?

- When EPS ?

EPS – An Overview

Popular measure of the performance of a company

and a factor in the valuation of its shares.

It is the reward of an investor for making his

investment and it is the best measure of

performance of a firm.

Ordinary investors make their investment decision

based on EPS.

Objective of financial management to

maximize the EPS------ from the view point of both the investor

and investee

---maximization of value measure in terms

of market price of equity share

Effects Of EPS

EPS affects the following:

– Value of a Share (Price Earning Ratio)

Market Price = EPS * P/E ratio

– Valuation of the Business as a whole

– Expectations of the Investors

– Dividend Payout Ratio etc……

Legal Framework

Accounting Standard - 20 issued by ICAI

– Commenced on 1-4-2001

– Mandatory for Companies

Accounting Standard Interpretation – 12

International Accounting Standard – 33

Legal Framework

To provide for uniform computational methodology

AS – 20 was issued.

Its mandatory for– Enterprises whose equity shares or potential equity shares

are listed in India.

– Enterprises whose shares are not so listed and are willing

to disclose the EPS

– Requirement of Part IV to Schedule VI of the Companies

Act, 1956

– Applicable for Level I Enterprises.

– Level II and Level III Enterprises – No Diluted

EPS and Disclosure as per 48(ii)

ACCOUNTING STANDARDS

INTERPRETATION - 12

APPLICABILITY OF AS 20

Every company, which is required to give

information under Part IV of Schedule VI to

the Companies Act, 1956, should calculate

and disclose EPS in accordance with AS 20,

whether or not its equity shares or potential

equity shares are listed.

ACCOUNTING STANDARDS

INTERPRETATION - 12

APPLICABILITY OF AS 20

Basis For Conclusions

AS 20 does not mandate an enterprise, which has

neither equity shares nor potential equity shares

which are so listed, to calculate and disclose EPS,

but, if that enterprise discloses EPS for complying

with the requirement of any statute, it should

calculate and disclose EPS in accordance with AS

20

Areas of Concern :

1

Whether applicable for Banking and

insurance companies?

2. Disclosure in Part IV – only Basic or

Both Basic and Diluted?

Practical Issues FY 05-06

Banking

Sector

Vijaya Bank

EPS on the

face of P&L

No (But in

Notes On

A/C)

Balance Sheet No

Abstract (Part

IV)

ING VYSYA Syndicate

Bank

Yes

Yes

Yes

No

Practical Issues FY 05-06

Others

ITL

WIPRO

Separate Disclosure of

Extra-ordinary item

Yes

No

Part IV

Diluted EPS

Yes

No

Part IV – Segregation

of Extraordinary items

No

No

Objectives of AS 20

Prescribes principles for the

determination and presentation of

EPS.

The focus of this statement is on the

denominator of the EPS calculation.

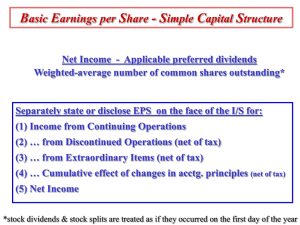

Presentation-Para 8 and 9

An enterprise should present earnings per share for all periods

Presentation on the Face of P & L A/c.

Separately for each class of equity share that has a different

right to share in profit

presented.

Types of EPS Basic EPS

Diluted EPS

A ) Whether disclosure is must when Profit is Negative?

B ) If yes, whether both Basic and Diluted EPS have to be presented?

Measurement

I. BASIC EARNINGS PER SHARE

A. Earnings – Basic = PAT – Pref. Div. incl. CDT

Points to Be Noted - Numerator

1.

Tax and impact of AS -22

2.

AS – 5 – Include Extraordinary items

3.

Preference Dividend –Non Cumulative – Deduct if

provided

-- Cumulative - Full Dividend

( only of current year)

4.

> one class of equity shares – apportion the profits as

per dividend rights

B. Per Share - Basic = Earnings / Weighted avg. No. Of Eq. shares

Points to Ponder - Denominator

1. Consider the weighted average no. of equity shares o/s. during the

period – time weighting factor - Refer Table I

2. AS- 14 : Transferee company

a. Purchase method – from the date of acquisition

b. Merger method – From the beginning of the reporting period

3. Partly paid shares - proportion to div rights – Refer Table II

4. Rights issue – consider the bonus element – Refer – Table III

5. Bonus issue or share split - Increase in shares without increase in

resources - Computation is from the beginning of the earliest period

reported – Refer Table IV

Table I - Weighted Average Number Of Shares

(Accounting year 01-01-2001 to 31-12-2001)

NO of

Shares

Issued

No. of

Shares

Bought Back

No. of

Shares

Outstanding

1st January,

2001

Balance at

beginning of

year

1800

-

1800

31st May,

2001

Issue of

shares for

cash

600

-

2400

1st Nov,

2001

Buy Back of

Shares

-

300

2100

31st Dec,

2001

Balance at

end of year

2400

300

2100

Computation of Weighted Average No :

(1800*5/12) + (2400*5/12) +(2100*2/12) = 2100

shares

The weighted average number of shares can

alternatively be computed as follows :

(1800*12/12) + (600*7/12) – (300*2/12) = 2100

shares

Table II – Partly paid shares

(Accounting year 01-01-2001 to 31-12-2001)

No. of shares

issued

Nominal value

of shares

Amount paid

1st Jan, 2001

Balance at

beginning of

year

1800

Rs 10

Rs 10

31st October,

2001

Issue of

shares

600

Rs 10

Rs 5

Assuming that partly paid shares are entitled to participate in the

dividend to the extent of amount paid, number of partly paid equity

shares would be taken as 300 for the purpose of calculation of EPS.

Computation of Weighted Average would be as follows :

(1800*12/12) + (300*2/12) = 1850 shares

Table III – Right Issue

(Accounting year 01-01-2000 to 31-12-2000)

Net Profit

Year 20*0 : Rs 11,00,000

Year 20*1 : Rs 15,00,000

No. of shares outstanding prior to

rights issue

5,00,000 shares

Rights issue

One new share for each five

outstanding (i.e. 1,00,000 new

shares)

Rights issue price : Rs 15.00

Fair value of one equity share

immediately prior to exercise of

rights on 1st March 2001

Rs 21.00

Computation of theoretical ex-rights fair value

per share

Fair value of all outstanding shares immediately prior to exercise

of rights + total amount received from exercise

Number of shares outstanding prior to exercise + number of

shares issued in the exercise

(Rs 21 * 5,00,000 shares) + (Rs 15 * 1,00,000 shares) /

5,00,000 + 1,00,000 shares

Theoretical ex-rights fair value per share = Rs 20.00

Computation of Adjustment factor

Rs 21.00 (Fair value per share prior to exercise of rights) / Rs

20.00(Theoretical ex-rights value per share) = 1.05

Computation of EPS

Year 2000

Year 2001

EPS for the year 2000 Rs 2.20

as originally reported :

Rs 11,00,000/5,00,000

shares

EPS for the year 2000

restated for rights

issue :

Rs 11,00,000 /

(5,00,000 shares *

1.05)

EPS for the year 2001

including effects of

rights issue

Rs 15,00,000 /

(5,00,000 * 1.05 *

2/12) + (6,00,000 *

10/12)

Rs 2.10

Rs 2.55

Table IV – Bonus Issue

(Accounting year 01-01-2000 to 31-12-2000)

Net profit for the year 2000

Rs 18,00,000

Net profit for the year 2001

Rs 60,00,000

No. of equity shares

outstanding until 30th

September 2001

20,00,000

Bonus issue 1st Oct 2001

2 equity shares for each equity share

outstanding at 30th Sept, 20*1

20,00,000*2=40,00,000

Earnings per share for the year

2001

60,00,000/(20,00,000 + 40,00,000) =

Rs 1.00

Adjusted EPS for the year 2000

18,00,000/(20,00,000+40,00,000) =

Rs 0.3

Since the Bonus issue is an issue without consideration, the issue is

treated as if it had occurred prior to the beginning of the year 2000, the

earliest period reported.

Table V - Determining the Order in Which to Include

Dilutive Securities in the Computing of Weighted Average

Number Of Shares

Earnings, i.e., Net profit

attributable to equity shareholders

Rs 1,00,00,000

No. of equity shares outstanding

20,00,000

Average fair value of one equity

share during the year

Rs 75.00

Potential Equity Shares

Options

1,00,000 with exercise price of Rs

60

Convertible Preference shares

8,00,000 shares entitled to a

cumulative dividend of Rs 8 per

sahre. Each preference share is

convertible into 2 equity shares.

10%

Attributable tax, e.g., corporate

dividend tax

12% Convertible Debentures of Rs

100 each

Nominal amount Rs 10,00,00,000.

Each debenture is convertible into

4 equity shares.

Tax rate

30%

Increase in Earnings Attributable to Equity

Shareholders on Conversion of Potential Equity

Shares

Increase in

Earnings

Increase in no. Earnings per

of Equity

Incremental

Shares

share

Options

Increase in

earnings

No. of

incremental

shares issued

for no

consideration{1.

00,000*(7560)/75}

Nil

20,000

Nil

Convertible

Preference

shares

Increase in net

profit

attributable to

equity

shareholders as

adjusted by

attributable tax

[Rs

8*8,00,000)+10

%(8*8,00,000)]

No. of

incremental

shares{2*8,00,0

00)]

Rs 70,40,000

16,00,000

Rs 4.40

12%

Convertible

Debentures

Increase in net

profit {Rs

10,00,00,000*0.

12*( 1 – 0.30)}

No. of

incremental

shares{10,00,00

0*4}

Rs 84,00,000

40,00,000

Rs 2.10

It may be noted from the above that options are most dilutive as their earnings per

Incremental shares is nil. Hence, for the purpose of computation of diluted EPS, options

will be considered first. 12% convertible debentures being second most dilutive will be

considered next and thereafter convertible preference shares will be considered (see para

42)

Computation of Diluted EPS

As reported

Net Profit

Attributable

(Rs)

No. of Equity Net profit

attributable

shares

1,00,000

20,00,000

Options

12%

Convertible

Debentures

Convertible

Pref shares

per share (Rs)

5.00

20,000

1,00,00,000

20,20,000

84,00,000

40,00,000

1,84,00,000

60,20,000

70,40,000

16,00,000

2,54,40,000

76,20,000

4.95

Dilutive

3.06

Dilutive

3.34

Ati-Dilutive

Since diluted EPS is increased when taking the convertible pref shares in A/C (from

Rs 3.06 to Rs 3.34), the convertible pref shares are anti-dilutive and are ignored in the

calculation of diluted EPS. Therefore, diluted EPS is Rs 3.06.

II. DILUTED EARNINGS PER SHARE

A. Earnings – Diluted

Points to Ponder

1.

Nr and Dr. – adjusted for effects of dilutive potential

equity shares.

- Potential equity share is a financial instrument or other contract

that entitles, or may entitle, its holder to equity shares

-Potential equity shares should be treated as dilutive

when, and only when, their conversion to equity shares

would decrease net profit per share from continuing

ordinary operations (PARA 39)

--Ignore Anti-dilutive potential equity shares`

Net Profit for the period attributable to

equity shares

- increased by dividends and tax

- increased by interest subject to

tax

- any other item affecting profits

B. Per Share – Diluted

Dilutive potential equity shares should be deemed

to have been converted into equity shares at the

beginning of the period or, if issued later, the date

of the issue of the potential equity shares.

-Share application money or advance share

application money is to be treated in same

manner as dilutive potential equity shares.

Steps : Para 35 to 37

1. Assume the exercise of dilutuve securities e.g. ESOP

2. Determine the fair value of share( e.g. avg. of last 6

months’ weekly closing prices)

3. Determine the exercise price

4. Shares issued for no consideration = Step 2 - Step 3

5. Dilutive shares only to the extent of Step No. 4 ( Refer

Table V)

6. Sequence – Most dilutive to least dilutive

Most Dilutive = Earnings per Incremental Share is least

Free shares considered

A. Right and Buy back--- Both for

Basic and Diluted

B. Options -- Only for Diluted (

Potential shares)

Factors Affecting EPS

Bonus issues, stock-splits and reverse stocksplits (consolidation of shares) change the

number of outstanding shares without

changing the resources available to the firm.

Therefore, companies adjust the number of

equity shares outstanding for those periods

for bonus issues, stock-splits and reverse

stock-splits while calculating the EPS.

RESTATEMENT

If the shares outstanding increases as a result of a

bonus issue or decreases as a result of basic and

diluted earnings per share should be adjusted for

all the periods presented.

An enterprise does not restate diluted earnings

per share of any prior period presented for

changes in the assumptions used or for the

conversion of potential equity shares into equity

shares outstanding.

Normally, EPS is not adjusted for transaction

occurring after the balance sheet date – no effect

on capital used.

Example

A firm XYZ whose net profit attributable to equity

share holders for 2005 was Rs 10,00,000 and the

number of outstanding shares 50,000. The EPS for

2005 will be 20.

In the year 2006 if the profit is 15,00,000 and

company issues 1:1 bonus.

In the financial statement of 2006 the EPS for 2005

would be readjusted to Rs 10

(Rs10,00,000/1,00,000) to ensure comparability,

even though it was reported at Rs 20 in financial

statements for the year 2005.

DISCLOSURE - Para 48 to

51

48 (i)Where the statement of profit or

loss includes extraordinary items, the

enterprise should disclose basic and

diluted EPS computed on the basis of

earnings excluding extraordinary

items

--- Prior period items ?

DISCLOSURE

48( ii) (a)the amounts used as

numerators, and a reconciliation of

those amounts to net profits or loss;

(b) the weighted average number of

equity shares used as the

denominator;

© the nominal value of shares along

with EPS figures.

AS – 20 and other AS Interconnection

As - 1

AS – 2

AS – 4

AS – 5

AS – 6

AS – 7

AS

AS

AS

AS

AS

AS

AS

–9

– 10

-11

– 12

– 13

– 14

– 15

AS

AS

AS

AS

AS

AS

AS

–

–

–

–

–

–

–

19

21

22

24

25

28

29

Other Matters :

IAS – 33

January 1996

February 1997

1 January 1999

18 December

Exposure Draft -- Earnings Per Share

IAS 33 Share

Earnings Per

Effective Date of IAS 33 (1997)

Revised version of IAS 33 issued by the IASB

2003

1 January 2005

Effective date of IAS 33 (Revised 2003)

Objective of IAS 33

to improve performance comparisons

between different enterprises in the same

period and between different accounting

periods for the same enterprise.

Scope

IAS 33 applies to entities whose securities

are publicly traded or that are in the process

of issuing securities to the public. [IAS 33.2]

Other entities that choose to present EPS

information must also comply with IAS 33.

[IAS 33.3]

Shortcomings of EPS

Does not consider the opportunity cost

of capital and can be manipulated by

short-term actions.

Let us take an example. Assume that a company

has 20,000 outstanding shares and earnings

available to shareholders is Rs 200,000. The EPS is

(Rs 2,00,000/ 20,000), or Rs 10. Assume that the

company borrows Rs 10,00,000 at an interest rate

of 8 per cent to buy back 10,000 shares. Assuming

an income tax rate of 40 per cent, the earnings

available to shareholders after the shares are

bought back will be [Rs 2,00,000 - (1.00 - 0.40) x

Rs. 80,000] or 1.52,000. Accordingly, EPS will be

reported at [Rs 1,52,000/10,000] or Rs 15.20.

Shortcomings of EPS

Indeed, financial economics tells us that (in the first approximation)

these two effects cancel out exactly and the return on invested

capital (ROIC) and the cost of capital do not change with a change in

the capital structure. Accordingly, economic profit (often called EVA)

too does not change with the change in the capital structure. Yet,

the example above shows that the EPS can increase in such

circumstances.

Therefore, it is not correct to conclude that the increase in EPS

always reflects better performance by the company.

For example, if a company finances a new project totally by

debt, EPS will increase if the project returns are higher than

the after-tax cost of debt, even if the project earns a return

lower than the cost of capital (WACC) of the company.

Although the EPS increases, such a project destroys value.

Shortcomings of EPS

Another important shortcoming of EPS

is that it does not relate EPS with the

invested capital. For example, two

companies may have same EPS, even

if one company has lower invested

capital as compared to the other.

Ignores the Scale and size of

operations

Problems with EPS

Reporting Standards

Complex Computation mechanism of

Diluted EPS

Basic EPS is subject to replacement on

the income statement by two

hypothetical EPS numbers.

The test used to identify common

stock equivalent securities is among

the most controversial of those rules

Inability to pinpoint the meaning of

common stock equivalency

Changing relationships between the

terms of particular securities and

prevailing market conditions are not

considered in the computational rules

for EPS.

Do these complicated EPS disclosures assist

investors and creditors in decision making? The

answer is unclear. Millar, et. al., report in the

September-October, 1987 Financial Analysts journal

that basic EPS and cash flow per share numbers are

more closely related to stock returns than either

primary or fully diluted EPS. Additional research is

needed to ascertain the relative usefulness of basic,

primary and fully diluted EPS.

In the mean time, accountants and auditors are

saddled with complicated rules of questionable

usefulness.

WRAP UP

Adhere to AS – 20

Be practical and objective oriented

Make no little plans ; they have

no magic to stir men’s blood –

Daniel Hudson Burnham

THANK

YOU

ONE AND ALL