Automotive Value Chain

advertisement

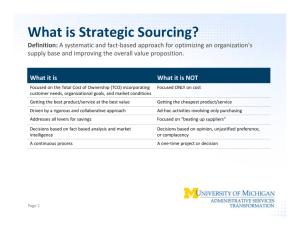

Partnering for Emerging Markets Focus on India Dr. Pawan Goenka President - Automotive Sector Mahindra & Mahindra Ltd. India Mahindra : An Introduction • Conglomerate with over 6.5 bn USD in revenues • Strong presence in six business verticals • Leading presence in the automotive business for • • • • over 63 years Lineage to the legendary Jeep Sales of over 1,80,000 vehicles in FY07 India’s largest SUV/UV player Alliances with Ford, Renault and International Truck The India Opportunity • 12th largest economy in • Source :World Development Indicators database, World Bank, 14 September 2007 terms of GDP 3rd largest economy in PPP terms The Indian Automotive Market • • • • • 11th largest car market 4th largest CV market 2nd largest 2W market Largest tractor market Largest 3W market Demonstrated Strong Growth 1,848 Four wheeler market In ‘000 vehicles 379 CVs + Cars + Uvs Source : SIAM F94 F95 F96 F97 F98 F99 Auto components $ billions F00 F01 F02 F03 F04 F05 F06 F07 15.0 3.1 Source : ACMA 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 Future Growth Drivers • • • • • • • Strong GDP growth Rapidly improving infrastructure Rising disposable incomes Favorable demographics Willingness to spend Easy finance availability Replacement of ageing vehicles AMP 2016: A Vision for Automotive Industry in India • Revenue 35 to 145 bn USD • Exports from 4 to 35 bn USD Vision 2016 “By 2016, India will emerge as the destination of choice in Asia for the design & manufacture of automobiles and automotive components. The output of the India’s automotive sector will be US$ 145 billion by 2016, contributing to 10% of India’s Gross Domestic Product and providing employment to 25 million persons additionally.” It’s Not Volume Growth Alone … • • • • • • • A global marketplace Very competitive market Technology upgradation Stringent emission and safety regulations Frequent launches of new models Low cost sourcing Increase in exports 8 out of top 10 global companies have India presence They contribute 60 % of global production but 25 % of India Production Source : World motor vehicle production by manufacturer : World Ranking 2006 OICA July 2007 and SIAM data Apr-Mar 2007 Global vs. Indian Top 5 1. 2. 3. 4. 5. GM Toyota Ford VW Group Honda 1. 2. 3. 4. 5. Maruti Suzuki Tata Motors Hyundai Mahindra Ashok Leyland Source : World motor vehicle production by manufacturer : World Ranking 2006 OICA July 2007 and SIAM data Apr-Mar 2007 Strong Capabilities of Indian OEM’s The $ 2,500 Car (The NANO) Very Competitive Market • From 20 models available in year 1995 to • 93 available today (Not counting the variants) 60 new launches planned in 2008 Source : Autocar India, The Economic Times, Dt. 26 Dec 2007 Suppliers in India MNCs MNC-JVs MNC Alliances Indian Recent Newsmakers 3Cs of Global Collaboration Strategy Cost 3Cs Capability Context Source : Innovation through Global Collaboration: A New Source of Competitive Advantage, Alan MacCormack, Harvard Business School Benefits from Collaboration Lower Costs Superior Capabilities Contextual Knowledge Low cost labor Rapid access to capacity Market access Low cost materials Technical know-how Supplier relationships Low cost suppliers Process expertise Institutional ties Low cost infrastructure Domain knowledge Government connections Strength of Indian partner Strength of MNC Source : Innovation through Global Collaboration: A New Source of Competitive Advantage, Alan MacCormack, Harvard Business School Partnership Options • Licensing • Tactical JV • Strategic JV – Escort service – Product based – Asset based – Comprehensive across the value chain Automotive Value Chain Design Engineering Sourcing Manufacturing Channel Scope of Collaboration JV Management Investment Contract Mfg. Channel Contract Mfg. Channel Product Dev. Sourcing Contract Mfg. Royalty M&M Capability M&M Evolution Licensing Scope of Collaboration Design Licensing M&M Case : Peugeot Design Engineering Sourcing Manufacturing Channel • Mid ’80s • Technical license for engines, and transmissions • Deliverables – M&M : Aggregates and related technology – Peugeot : Brand building, Commercial benefits • Pure limited life commercial transaction • As M&M matured, need diminished Tactical JV M&M Case 1 : Mahindra Ford (50:50 JV) Design Engineering Sourcing Manufacturing Channel • Mid ’90s • Ford Escort assembly at M&M plant • Deliverables – M&M – Ford : Market knowledge, Capacity, Relationships : Product engineering, Processes, Know how • Asset based partnership, as partners matured, need diminished • JV could have graduated to a higher level, but for the Scorpio development Tactical JV M&M Case 2 : Mahindra Renault (51:49 JV) Design Engineering Sourcing Manufacturing Channel • 2005 : Product specific JV for Logan • Deliverables – M&M : India knowledge, capacity, channel, relationships, engineering support, JV management – Renault : Product, Engineering for India, Global processes, Purchasing organisation • Asset based partnership but structured to meet both partners’ differing aspirations • Could graduate to a different level Strategic JV M&M Case : Mahindra ITEC (51:49 JV) Design Engineering Sourcing Manufacturing Channel • 2005 : Comprehensive global CV tie-up • JV designing full range of CVs from scratch • Deliverables – M&M – ITEC : Market knowledge, PD skills, LCVs, Capacity, Relationships, Sourcing and Engineering skills : M&HCV experience, Engines, PD skills, Global brand, Sourcing and Engineering opportunity • Structured to meet both partners’ complementary aspirations Critical Negotiation Issues • • • • • • • Shareholding Dilution Termination/exit pricing IPR Branding Management Governing Law Other Negotiation Issues • • • • • Non Solicitation Non Compete Differing return requirements Negotiations of key products and services purchased from parents Consensus decision items Issues in Negotiation Process • Bureaucracy in Global OEMs – Silo structure – Decision making power • Discipline in Indian partner teams • Strong influence of lawyers in Global OEMs • Require open mindset Why JVs Fail • • • • Inability of Indian partner to invest MNC does not need Indian partner any more Indian partner does not need MNC any more Non performance of JVs Key Success Factors • Know, appreciate and accept both partners • • objectives Good negotiating process covering all future contentious points and scenarios Build and nurture trust Key Insight Both partners must accept Equal partnership of Un-equal partners Thank You