HW 2 Solution

HW 2 Solution

1.

You have accumulated $4,400 in credit card debt. Your credit card rate is 8.5% APR and you are charged interest every month on the unpaid balance on your account. How much interest must you pay every month, assuming the balance remains unchanged?

$31.17

Interest = $4,400(0.085/12) = $31.17

2. You have accumulated $5,000 in credit card debt. Your credit card rate is 9.5% APR and you are charged interest every month on the unpaid balance on your account. If you pay $500 a month and incur no new debt, how long will it take you to pay off your credit card balance? 10.46 months

P/Y=12, I/Y=9.5, PV=5000, PMT=-500; CPT,N: N = 10.46 months

3.

Assume you want to deposit $15,000 in a commercial bank. Which savings account is better, one paying 6% with yearly compounding or one paying 5.9% with continuous compounding. Show your future value calculations.

1 st Option: P/Y=1, N=1, I/Y=6, PV=15000; CPT,FV; FV = $15,900

2 nd Option: FV = PVe rT = $15,000e 0.059 (1) = $15,911.63 Option 2 is better

4.

If you need an estimated $250,000 for your kid’s college education in 7 years, how much money should you set aside today on a U.S. savings bond earning 7.5% per year with continuous compounding?

PV = FV/e rT = $250,000 / e 0.075(7) = $250,000 / 1.690459 = $147,888.84

5. You are being offered a $50,000 loan at a quoted rate of 5% with daily compounding of interest. What is the nominal rate?

What is the periodic rate? What is the effective rate?

r nominal r periodic r effective

= 5%

= 5%/365 = 0.01367%

= (1 + r nominal

/m) m – 1 = (1 + 0.05/365) 365 -1 = 1.051267 -1 = 5.1267%

6.

You are getting a $19,500 loan from your bank to buy a car. You are required to pay it within 5 years in monthly installments of $430.00 each due at month-end. What would the periodic, nominal and effective rates be on this loan?

r nominal r periodic r effective

: P/Y=12, N=60, PV=19500, PMT= - 430.00; CPT,I/Y=, I/Y = 11.6168%

= 11.6168% /12 = 0.9681%

= (1 + 0.116168/12) 12 -1 = (1.009681) 12 – 1 = 1.122557 - 1 = 12.2557%

7.

You are getting a $3,000 loan from a dealership to buy a used car. The dealer has given you the choice between two different credit alternatives. The first one is a two-year financing deal, with payments of $142.60 per month. The other one is a threeyear financing deal, with monthly payments of $100.83. Based on effective rate of interest calculations, which of the two loans in the previous question would you chose?

1 st

2 nd

Option: P/Y=12, N=24, PV=3000, PMT= - 142.60; CPT,I/Y=, I/Y = 12.9819% r effective

= (1 + 0.129819 /12) 12 – 1 = (1.010818) 12 – 1 = 1.137829 – 1 = 13.7829%

Option: P/Y=12, N=36, PV=3000, PMT= - 100.83; CPT,I/Y=, I/Y = r effective

= (1 + 0.128256 /12) 12

12.8256%

– 1 = (1.010688) 12 – 1 = 1.136071 – 1 = 13.6071%

1

8.

Your brother-in-law is inviting you to invest some money with him. He argues that he can beat whatever effective yield you are getting form your mutual fund. He is asking you to invest $10,000 today and promises to pay you back $15,000 in five years. If your mutual fund pays you an average annual rate of return of 8%, is your brother-in-law telling the truth?

8.4472%

1) Find the total ROR over 5 years: ($15,000 - $10,000) / $10,000 = 50%

2) Find the annual ROR: (1 + ROR

Total

)

OR

1/T – 1 = (1 + 0.5) 1/5 -1 = (1.5) 0.2 – 1 = 1.084472 – 1 = 8.4472%

P/Y=1, N=5, PV=-10,000, FV=15,000; CPT I/Y; I/Y = 8.4472%

Your brother-in-law is telling the truth

9.

What is the future value of an ordinary annuity yielding 6.00% APR that pays semiannual payments of $500 for 1.5 years?

(Do the math; do not use the financial functions on your calculator. Draw a cash flow diagram) $1,545.45

FV = PV(1 + r/m) n + PV(1 + r/m)

= 500(1 + 0.06/2) 2 n-1 + …………..

+ 500(1 + 0.06/2) 1 + 500

= 500(1.0609

2 + 1.03 + 1)

= 500(3.0909)

= $1,545.45

r = 6%

0 1

1 yr

2 3

FV = ?

PMT = 500

10.

You are considering financing a new car which cost $48,999 with an amortized loan. Your bank offers a nominal rate of

7.200% for a 6 year loan with monthly payments. How much will each payment be? (Draw a cash flow diagram) $840.10

Solution Opt 1: r periodic

= r nominal

/ m = 7.2%/12 = 0.60%

P/Y=1, N=72, I/Y=0.6, PV=48999; CPT,PMT: PMT = $840.10

Solution Opt 2: P/Y=12, N=72, I/Y=7.2, PV=48999;

CPT,PMT: PMT = $840.10

0

PV = $48,999 m=12, T=6; n = m x T = 12 x 6 = 72

6 yrs

1 2 70 71 72

PMT = ?

11. Today you deposit $2000 in a bank account that pays 3.6% APR compounded weekly. How much money would you have in that account 21 months from now. Do not assume there are 4 weeks per month. There are 52 weeks per year.

$2,130.01

m = 52, T = 21 mos/12 mos per yr = 1.75; n = 52 x 1.75 = 91

P/Y=52, N=91, I/Y=3.6, PV=2000; CPT,FV= $2,130.01

12.

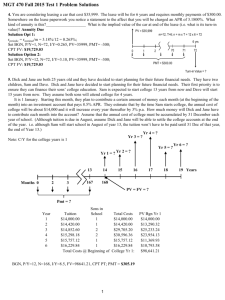

You are tasked with estimating the fair market value of a security that promises uneven future payments. The table below shows the quarterly payment schedule (each cash flow occurs at the end of the quarter ). You consider 7.2% p.a. to be the appropriate opportunity cost. What is the theoretical value of this security? (Draw a cash flow diagram) $1,806.41

1 st Qtr

$300

2 nd Qtr

$400 m = 4; r periodic

= r nominal

= 7.2%/4 = 1.8%

CF, 2nd, CLR WORK (Clears Cash Flow Registers)

0, ENTER,

↓, 300, ENTER

↓, ↓, 400, ENTER

↓, ↓, 500, ENTER

↓, ↓, 700, ENTER

NPV, 1.8, ENTER

↓, CPT = $1,806.41

0 1

300

3 rd Qtr

$500

2

400

3

500

1 yr

4

700

4 th Qtr

$700

2

13.

You are considering leasing a small warehouse for 3 years. The lease requires monthly payments of $448.00. Somewhere on the lease paperwork you notice a statement to the affect that you will be charged an nominal rate of 4.800%. Ignore the turn-in value or salvage value of the warehouse. What is the value of the lease? (Draw a cash flow diagram) $15,052.68

Solution Opt 1: r periodic

= r simple

/m = 4.8%/12 = 0.4%

Set to BGN mode, P/Y=1, N=36, I/Y=0.4, PMT=448; CPT,PV:

PV = $15,052.68

Solution Opt 2: Set to BGN mode: P/Y=12, N=36 I/Y=4.8,

PMT=448; CPT,PV: PV = $15,052.68

0

PV = ?

r simple

= 4.8%

1 2 m=12, T=3; n = m x T = 12 x 3 = 36

34 35

3 yrs

36

PMT =448

14.

Fly By Night Trucking Company is financing a new truck with an amortized loan of $50,000 to be repaid in 11 semi-annual installments of $5,776.92, paid at the end of each six months. (Draw a cash flow diagram) What type of annuity is this?____________________. What is the annual cost of debt for this loan? 8.4500%

PV = 50,000 m = 2

Ordinary Annuity or Annuity in Arrears

Solution Opt 1:

1) P/Y=1, N=11, PV=50000, PMT=-5776.92; CPT,I/Y; I/Y = 4.225% This is a periodic rate!

2) Find APR: r nominal

= r periodic x m = 4.225% x 2 = 8.4500%

Solution Opt 2: P/Y=2, N=11, PV=50000, PMT=-5776.92; CPT,I/Y; I/Y = 8.4500%

0 1 2 9 10

6 yrs

11

PMT = 5,776.92

15. Today you deposit $90,000 of your company's money in an investment account that pays 7.97% p.a. compounded weekly.

How much money would you have in that account 11 months from now? Do not assume there are 4 weeks per month. There are 52 weeks per year. $96,815.98

m = 52, T = 11 mos/12 mos per yr = 0.916667 yr; n = 52 per/yr x 0. 916667 yr = 47.666667 periods

P/Y=52, N= 47.666667, I/Y=7.97, PV=90000; CPT,FV= $96,815.98

16.

Today is 1 January and you plan to start investing in a stock mutual fund that pays quarterly dividends. The fund’s value has grown at an average rate of 9.42% p.a. for the past 3 years. Today you deposited $1,500 into this account and will continue to deposit that amount at the beginning of every 3 months thereafter. What type of annuity is this? _________________. How much money would you have in this account after 5 1/2 years? (Draw a cash flow diagram) $43,600.70

Annuity Due

Solution Opt 1: r periodic

= r nominal

/m = 9.42%/4 = 2.355%

Set to BGN mode, P/Y=1, N=22, I/Y=2.355, PMT=1500;

CPT,FV: FV = $43,600.70

Solution Opt 2: Set to BGN mode: P/Y=4, N=22, I/Y=9.42,

PMT=1500; CPT,FV:

FV = $43,600.70

m=4, T=5.5; n = m x T = 4 x 5.5 = 22

0 1 2 r simple

= 9.42%

20 21

FV = ?

5.5 yrs

22

PMT = $1500

17.

How many years will it take for your savings account to accumulate $1m if it pays 4% interest per year compounded semiannually and you deposit $10k every 6-months at the end of the 6-month period?

27.74 years a) Find number of periods r periodic

= r nominal

/ m = 4%/2 = 2%

P/Y=1, I/Y= 2, PMT=-10000, FV=1000000; CPT,N: N = 55.48 periods

OR

P/Y=2, I/Y= 4, PMT=-10000, FV=1000000; CPT,N: N = 55.48 periods b) Find number of years

Years = N/m = 55.48/2 = 27.74 years

3

18.

You are considering financing a new car which with an amortized loan. Your bank offers a nominal rate of 6.4500% for a 6 year loan with monthly payments. You cannot afford to pay more than $400 per month. What is the price of the most expensive car you can afford to finance? (Draw a cash flow diagram) $23,829.19

Solution Opt 1: r periodic

= r nominal

/ m = 6.45%/12 = 0.5375%

P/Y=1, N=72, I/Y=0. 5375, PMT=400; CPT,PV: PV =

$23,829.19

Solution Opt 2:

P/Y=12, N=72, I/Y=6.45, PMT=400; CPT,PV: PV =

$23,829.19

PV = ?

r nominal

1

= ?

2 m = 12, T = 6; n = m x T = 12 x 6 =72

70 71

6 yrs

72

PMT = 400

19. You are considering leasing a car that cost $34,000. The lease will be for 5 years and requires monthly payments.

Somewhere on the lease paperwork you notice a statement to the affect that you will be charged an APR of 5.4000%. Assume the car will be worth $16,000 at the end of the lease. How much will your payments be? $413.13

r periodic

= r nominal

/m = 5.4000%/12 = 0.45%

Set BGN, P/Y=1, N=60, I/Y=0.45, PV=34000, FV= -16000; CPT PMT:

PMT = $413.13

OR

Set BGN, P/Y=12, N=60, I/Y=5.4, PV=34000, FV= -16000; CPT PMT:

PMT = $413.13

0

PV = $34,000 m=12, T=5; n = m x T = 60

1 2

5 yrs

58 59 60

PMT = ?

Turn-in = $16,000

20.

Today you open a new investment account for your company. The account has had an average yield of 9.5600% p.a. over the last three years and compounds every quarter . You plan to deposit $6,000 into this account every month , at the end of the month . Your first deposit will be at the end of this month. How much will you have in this account 3 years from now?.

P/Y=12, C/Y=4, N=36, I/Y=9.56, PMT=6000; CPT,FV:

FV = $248,737.32

OR

Convert the quarterly rate into a monthly rate then solve for FV

2nd , ICONV, 9.56, ENTER,

, 4, ENTER,

, CPT: EFF% = 9.9082%

↓, 12, ENTER. ↓, CPT: NOM% = 9.4848%

P/Y=12, N=36, I/Y=9.4848, PMT=6000; CPT,FV: FV = $248,737.32

m=12, T=3; n = m x T = 12 x 3 = 36

Note: use the m of the payments to compute n

FV = ?

0 1 2 34 35 36

PMT = $6,000

4