Simple interest - Haaga

advertisement

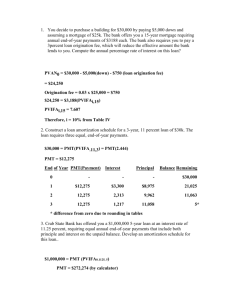

Business Mathematics Periodic payments Haaga-Helia / KeiKa Page 1 Periodic payments FV = Future Value of all periodic payments PV = Present Value of all periodic payments pmt = Payment (= constant amount of money paid regularly). Also called an Annuity p% i = interest rate for the payment period in a decimal format [ i = ] 100 n = number of payments 1. Future value FV 2. Present value (1 i ) n 1 pmt i PV 3. Payment (from the future value) pmt i FV (1 i ) n 1 (1 i ) n 1 pmt (1 i ) n i 4. Payment (from the present value) pmt (1 i ) n i PV (1 i) n 1 Example 1. 250 € is paid monthly for 10 years. The annual net interest rate is 2,1%. pmt = 250 € 0,021 i= = 0,00175 12 n = 10 × 12 = 120 1,00175120 1 FV 250 € 33 350 € 0,00175 Example 2. The loan can be paid back with 400 € monthly payments. Loan time is 5 years and the interest is 4,2%. How big the loan can be? (Note! Loan = Present value) pmt = 400 € 0,042 i= = 0,0035 12 n = 5 × 12 = 60 1,003560 1 400 € 21 613 € Loan = PV 1,003560 0,0035 Business Mathematics Periodic payments Haaga-Helia / KeiKa Page 2 Example 3. How much must a person save monthly if he wants to have 25 000 € after 7 years? The annual interest rate is 1,8% and source tax is 28%. FV = 25 000 € 0,018 0,72 = 0,00108 i= 12 (note: source tax is removed by multiplying with 0,72) pmt n = 7 × 12 = 84 0,00108 25 000 € 284,48 € 1,0010884 1 Example 4. What is the equal monthly payment for a 120 000 € loan, if the loan time is 20 years and the interest is 4,44% ? PV = 120 000 € 0,0444 i= = 0,0037 12 n = 20 × 12 = 240 pmt 1,0037 240 0,0037 120 000 € 755,30 € 1,0037 240 1