PHS Power Point template

advertisement

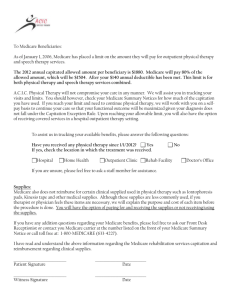

Optimizing Reimbursement Through the Medicare Cost Report Presented by: Susan Ruchin, Senior Manager Glenn Bunting, Director 1 The material appearing in this presentation is for informational purposes only and is not legal or accounting advice. Communication of this information is not intended to create, and receipt does not constitute, a legal relationship, including, but not limited to, an accountant-client relationship. Although these materials may have been prepared by professionals, they should not be used as a substitute for professional services. If legal, accounting, or other professional advice is required, the services of a professional should be sought. 2 PRESENTERS Susan Ruchin, Senior Manager │ Moss Adams LLP Susan has been in the health care industry for over 25 years, including 10 years working for a Medicare fiscal intermediary in the supervision and audit of large health care chain organizations. She also has six years of experience in hospital settings, where she was responsible for all phases of reimbursement, including Medicare cost report preparation and appeals with the Provider Reimbursement Review Board. Susan assists clients with wage index reviews, geographic reclassifications, and provider-based requirements such as signage, state licensure, and attestations. She also prepares and reviews Medicare cost reports and provides audit support to hospitals, skilled nursing facilities, and federally qualified health clinics during Medicare and Medicaid audits. Glenn Bunting, Director │ Moss Adams LLP Glenn has over 20 years of experience in the health care finance industry. With an emphasis on serving health care organizations with Medicare and Medicaid reimbursement and related billing and coding issues, he assists in overseeing the Health Care Consulting Group's Third-Party Reimbursement Practice including charge capture services, cost reporting, appeal services, and medical education programs. Glenn focuses on core reimbursement services, optimization and compliance, Medicare wage index and occupational mix reporting, reimbursement department outsourcing, and Medicare and Medicaid cost report appeals. MOSS ADAMS LLP | 3 PRESENTATION OVERVIEW • Why is the Cost Report Important? • Wage Index Information • Disproportionate Share Hospital (DSH) Payments / Uncompensated Care • Medicare Bad Debt • Medicare Managed Care Days for GME and HIT Payments • Charity Care for HIT and DSH Reimbursement • Importance of a Robust Protested Amount List • Best Cost Report Practices 4 THE IMPORTANCE OF YOUR COST REPORT “Why should I be concerned, there is no settlement impact?” • You may not see any settlement impact year-to-year, but we are entering a new era in prospective rate setting • Imperative for providers nationwide to work in unison through: o Homogenous completion of the Medicare cost report o Aligning costs and charges in the prescribed CMS cost centers o Utilizing “best-practices” with UB-04 revenue and CPT/HCPCS codes • Main focus of today is PPS rate setting, but CAH facilities are even more aware of the issue of proper cost center coding 5 THE CAVEAT - WHY WE ARE HERE TODAY • Medicare cost report in its original form not designed to support estimate of costs at DRG and APC level • To increase integrity of changing & designing new DRG and APC weights, a workgroup of hospital experts was convened by the AHA • Workgroup’s recommendations were: o To achieve more accurate DRG cost-based weights All hospitals should prepare their Medicare cost reports so Medicare charges, total charges and overall costs are aligned with each other and with the categories currently utilized in MedPAR file o The workgroup considered changes to Uniform Bill (UB) formats, revenue codes Cost Report, and MedPAR 6 THE MEDICARE COST REPORT • Currently, the Medicare cost report is CMS’ only standardized cost finding tool for Hospitals, SNFs, HHAs, etc. • In lieu of “standard federal general ledger format,” CMS believes cost report is reasonable / effective alternative Food For Thought • B-1 step down allocation has not been revised since inception • But... calculations within the cost report contain information beneficial to both Medicare and You 7 HOW DOES CMS USE COST REPORT DATA? Three primary areas: • Revise DRG & APC weights • Market basket relative weights to update payment rates for the CMS Prospective Payment System • Analyze payment adequacy (is Medicare paying fair and efficient rates for different classes of providers for different types of services) 8 MARKET BASKET ADJUSTMENT (AVG WEIGHT) Major expenditure categories used for update: 1) 2) 3) 4) 5) 6) 7) Wages and salaries Employee benefits Contract labor Pharmaceuticals Malpractice insurance Blood and blood products Residual (all other) Total 45.819 12.713 1.806 1.330 5.402 1.069 31.861 100.000 9 WHAT DATA DOES CMS USE FROM THE REPORT? • Wage index information • Total salary & non-salary costs before allocation & adjustments from WKS A to the various cost components • Total costs before and after allocation from WKS B • Capital Market Basket (capital costs directly assigned and capital cost data from WKS A-7) 10 REPORT DATA FIELDS NOT COMPLETED • Fields on the report not completed can be problematic (i.e. bias in the cost weight) o Example: Blood not separated for the majority of hospitals. • Could be acceptable if the provider’s costs for that field are representative of all other providers • Although problematic if the blood costs are not representative. 11 MALPRACTICE COSTS • WS S-2 reporting of malpractice costs • 1,200 hospitals reported no costs for malpractice, paid losses and/or self insurance information • How does this impact the market basket? 12 CONSEQUENCES OF FLAWED REPORTING • To the extent that providers do not fill in cost report fields, CMS is compelled to make assumptions about costs • Resort to judgment based methods (instead of strict computational methods) for deriving representative market basket cost weights. • Example of blood cost weight in the PPS market basket. Over 1,500 hospitals did not report blood costs separately on the cost report. 13 CMS RECEIVES SPECIAL REQUESTS • Payment and Cost Analyses Examples: o Simulate margins assuming the implementation of payment policy changes o Determine the percentage of hospitals in each margin range by critical access status, ownership type, and bed size to determine if the hospitals could afford to implement measures for influenza or Ebola outbreaks 14 PROVIDER REIMBURSEMENT MANUAL • Provides guidelines and policies to implement Medicare regulations which set forth principles for determining the reasonable cost of provider services furnished under the Health Insurance for the Aged Act of 1965, as amended. • Procedures and methods have been devised to accommodate program needs and the administrative needs of providers and their intermediaries and will assure that the reasonable cost regulations are uniformly applied nationally without regard to where covered services are furnished. • CMS’ interpretation of Federal Regulations/Laws which dictate what and how providers report their operating outcomes to CMS. 15 COST CENTER DEFINITION PRM 15-1 § 2302.8 Cost Center • An organizational unit, generally a department or its subunit, having a common functional purpose for which direct and indirect costs are accumulated, allocated and apportioned. • Natural expense classifications (e.g., depreciation) and non-allowable cost centers (e.g., research) specifically required by the instructions fall under this definition. 16 COST CENTERS VS. GL DEPARTMENTS Cost Centers: • May include more than one GL department • Non-Allowable Costs vs. NRCCs (e.g. Hospital Based Phys.) GL Departments: • Specific to the entity • Expenses and Revenues may need to be reclassified o Examples: Blood Products Medical Supplies Pharmaceuticals 17 18 Volume Performance Medicare to Become Majority of Volume by 2022 Projected Number of Medicare Beneficiaries Average Inpatient Case Mix By Volume Millions of Beneficiaries n = 785 Hospitals 6% 2% 25% 60.7 33% 59.0 15% 57.3 19% 55.6 58% 54.0 42% 2014 2016 2018 ©2014 The Advisory Board Company • advisory.com 2020 2022 2012 2022 Self-Pay Medicaid Commercial Medicare Source: CMS, “2013 Annual Report of the Boards of Trustees of the Federal Hospital Insurance and Federal Supplementary Medical Insurance Trust Funds,” May 31, 2013, available at: http://downloads.cms.gov/files/TR2013.pdf; Health Care Advisory Board interviews and analysis. WHY IS WAGE INDEX INFORMATION IMPORTANT? • Medicare Inpatient DRG Reimbursement • Medicare Outpatient APC Reimbursement • Medicare Inpatient Psych Facility (IPF) Reimbursement • Medicare Inpatient Rehabilitation Facility (IRF) Reimbursement • Medicare Inpatient Skilled Nursing Facility (SNF) Reimbursement • Other Health Plans Use Medicare Data Elements for Payment MOSS ADAMS LLP | 19 DRG PAYMENT RATES: WAGE INDEX > 1.0000 FFY 2014 Final (8/19/13 FR) FFY 2015 Final (10/3/14 FR Corrected) Labor-Related $3,737.71 $3,784.75 Non-Labor 1,632.57 1,653.10 Capital 429.31 434.97 Total Payment Rate $5,799.59 $5,872.82 Increase of $73.23 or 1.26% from prior year The data above assumes hospital is submitting quality data and is a meaningful EHR user. MOSS ADAMS LLP | 20 DRG PAYMENT RATES: WAGE INDEX <=1.0000 FFY 2014 Final (8/19/13 FR) FFY 2015 Final (10/3/14 FR Corrected) Labor-Related $3,329.57 $3,371.47 Non-Labor 2,040.71 2,066.38 Capital 429.31 434.97 Total Payment Rate $5,799.59 $5,872.82 MOSS ADAMS LLP | 21 WAGE INDEX DATA USED BY CMS • Step 1: CMS Obtains Hospital Average Hourly Wage From WS S-3, Part III, Line 6 • Step 2: CMS Applies Adjustments to Average Hourly Wage o o o o Overhead Allocation Applied Occupational Mix Adjustment Midpoint Adjustment to Normalize the Data Inflation Adjustment MOSS ADAMS LLP | 22 STATE OF HAWAII FINAL AVERAGE HOURLY WAGE FOR FFY 2015 60.00 50.00 40.00 30.00 20.00 10.00 0.00 54.66 50.55 47.48 45.07 45.07 44.66 42.60 42.17 41.75 41.25 41.05 40.82 Average Hourly Wage Kaiser Hospital Hawaii (U) The Queens Medical Center (U) Pali Momi Medical Center (U) Castle Medical Center (U) Straub Clinic and Hospital (U) Wilcox Memorial Hospital (R) Maui Memorial Medical Center (U) Kuakini Medical Center (U) Wahiawa General Hospital (U) North Hawaii Comm. Hospital (R) Hilo Medical Center (R) Kona Community Hospital (R) MOSS ADAMS LLP | 23 WAGE INDEX DATA USED BY CMS • Step 3: Adjusted Hourly Wage Data Grouped by County or Counties and Averaged With a Core Based Statistical Area (CBSA) o CBSA determined by OMB o CBSA designations can change every 10 years o CBSAs can change through legislative means! 24 WAGE INDEX DATA USED BY CMS • Step 4: CBSA Average Hourly Wage Compared to National Average Hourly Wage o If CBSA is equal to National, Wage Index Factor is 1.0000 o If CBSA is less than National, Wage Index Factor is less than 1.000 o If CBSA is greater than National, Wage Index Factor is greater than 1.000 25 HI WAGE INDEX FACTOR TRENDS Federal Fiscal Year 1.25 WI Factor 1.2 1.15 1.1 1.05 1 0.95 HI URBAN HI RURAL MAUI COUNTY FFY 2012 1.1428 1.1295 1.1295 FFY 2013 1.2016 1.0718 1.0718 FFY 2014 1.2164 1.0709 1.0709 FFY 2015 1.2300 1.0572 1.0737 26 WESTERN REGION WAGE INDEX FACTOR FOR FFY 2015 2.0000 1.724 1.8000 1.6000 1.307 1.4000 1.230 1.207 1.155 1.074 1.2000 1.0000 0.8000 0.6000 0.4000 0.2000 1.057 1.288 0.998 1.086 1.307 0.0000 HIGHEST URBAN AREA STATEWIDE RURAL MOSS ADAMS LLP | 27 WAGE INDEX DATA ELEMENTS • What are the data elements reported in the Medicare cost report that comprise the wage index information and set my Medicare payment? o o o o o Salary Paid Hours Contract Labor and Hours Physician Part A Compensation and Hours Wage Related Cost - Benefits 28 SALARY REPORTED ON WS A, COL. 1 • Direct salaries and wages, including amounts for related paid vacation, holiday, sick leave, other paid-time-off (PTO), severance pay, and bonus pay for personnel associated with the line item. • Bonus pay includes award pay and vacation, holiday, and sick pay conversion (pay in lieu of time off). 29 SALARY REPORTED ON WS A, COL. 1 • Source for WS A Salaries: General Ledger • General Ledger Includes: o Cost paid during the year o Cost accrued during the year • Salary and PTO Includes Both Paid and Accrued Expense • WS A, Col. 1 Salary Flows to WS S-3, Part II, Col. 2 30 PAID HOURS REPORTED ON WS S-3, PART II • Source for Hours: Payroll Report • Paid hours include regular hours (including paid lunch hours), overtime hours, paid holiday, vacation and sick leave hours, paid time-off hours, and hours associated with severance pay. • On call hours are not to be included in the total paid hours 31 PAID HOURS REPORTED ON WS S-3, PART II • Overtime hours are calculated as one hour when an employee is paid time and a half • No hours are required for bonus pay • Full Time Intern and Residents – 2,080 Hrs. • Full Time Salaried Employees Paid Fixed Rate – 2,080 Hrs (based upon 40 hrs. / week). MOSS ADAMS LLP | 32 CONTRACT LABOR REPORTED ON WS S3, PART II Note: All contract labor expense should be reported on WS A, Col. 2 • Line 11: Direct patient care services include nursing, diagnostic, therapeutic, and rehabilitative services. o Report only personnel costs – no supplies or nonsalary cost. o Do not include costs applicable to excluded areas reported on line 9 and 10 MOSS ADAMS LLP | 33 CONTRACT LABOR REPORTED ON WS S3, PART II • Line 12: Contracted top level management services (routine and ancillary patient care cost centers) • Line 13: Physician Part A administration paid under contract o Per time study data reported on WS A-8-2 o Medical directors 34 CONTRACT LABOR REPORTED ON WS S3, PART II • Line 14: Salary and hours associated with the home office and/or regional office cost statement o Apply same hospital related salary and hours procedures to home office / regional office o Include a directly assigned or allocated share of employee benefit expense • Line 15: Salary, hours and wage related cost associated with home office Physician Part A Administration 35 OTHER CONTRACT LABOR WS S-3, PART II • Line 28: A&G Under Contract o o o o o Contract information / data processing services Legal fees Tax preparation fees Cost report preparation fees Purchasing services Do not include the same costs on this line and lines 11 or 12 36 OTHER CONTRACT LABOR WS S-3, PART II • Line 33: Housekeeping Under Contract • Line 35: Dietary Under Contract Hours may need to be obtained from contract with vendor or from the vendor directly 37 WAGE RELATED COST WS S-3, PART II • Allowable wage related costs (i.e. employee benefits) are listed and reported on WS S-3, Part IV. o o o o o o o o o Retirement Cost (4 types) Plan Administrative Expense (Legal, Accounting, Admin) Employee Health Insurance (Prescription Drug, Dental, Vision) Life, Accident and Disability Insurance Long Term Care Insurance Workers Compensation Retirement Health Insurance Taxes (FICA, Medicare, SUI, FUI) Other (Tuition, Day Care, Executive Deferred Comp) 38 WAGE RELATED COST WS S-3, PART II • Unless wage related costs are directly assigned to specific cost centers, expenses are allocated between the following areas using salary as a proxy: o o o o o o o o Core (general service, routine, ancillary, outpatient) Excluded (Rehab, Psych, SNF, NRCC) Non-Physician Anesthetist (Part A and Part B) Physician Part A Administrative Physician Part A Teaching Physician Part B RHC / FQHC Intern and Resident 39 WAGE RELATED COST WS S-3, PART II • Retirement Costs Reported on a Cash Paid Basis: o 401K Employer Contributions o Tax Sheltered Annuity o Nonqualified Defined Benefit Plan • Retirement Costs Reported on a 3 Yr. Average Methodology (WS S-3, Part IV, Exhibit 3): o Qualified Defined Benefit Plan Need Cash Contribution to Plan Documents Actuary Report(s) and IRS Form 5500 40 WAGE RELATED COST WS S-3, PART II • Health Insurance o Purchased Health Insurance Premium costs, and costs paid to external organizations for plan administration o Self Funded Health Insurance Costs paid to external organizations for plan administration Cost hospital incurs in providing services under plan to its employees o Health-Related Services Health services not covered employee’s plan Provided by hospital at no cost or a discount MOSS ADAMS LLP | 41 OTHER WAGE RELATED COST WS S-3, PART II • Qualifying Criteria o Exception to the core list on WS S-3, Part IV o The wage-related cost has not been furnished for the convenience of the provider o The wage-related cost is a fringe benefit as defined by the IRS (e.g. unrecovered cost of employee meals, education costs, auto allowances) o The total cost of the particular wage-related cost for employees whose services are paid under IPPS exceeds 1 percent of total salaries MOSS ADAMS LLP | 42 DSH/UNCOMPENSATED CARE • • • • • Must meet DSH payment formula’s 15% qualifying threshold in order to receive uncompensated care payment No change to eligibility requirements for DSH or uncompensated care for FY 2015 FFY 2015 gross DSH payments estimated at $13.383B in the final rule compared to $14.205B in the proposed rule 25% of DSH = $3.346 billion Factor 1 – uncompensated care = $10.037 billion MOSS ADAMS LLP | 43 DSH/UNCOMPENSATED CARE IMPACT MOSS ADAMS LLP | 44 DSH/UNCOMPENSATED CARE • • • • Factor 3 is hospital-specific value Medicaid days taken from the 2011/2012 cost reports (March 2014 HCRIS) CMS used FFY 2011 in proposed rule CMS used FFY 2012 SSI published June 2014 for Factor 3 in FY 2015 Final Rule o SSI ratios based on FFY, not hospital fiscal year o May impact uncompensated care payments shown on following slides MOSS ADAMS LLP | 45 UNCOMPENSATED CARE INFO FY 2015 IPPS FINAL Rule: Implementation of Section 3133 of the Affordable Care Act - Medicare DSH - Supplemental Data State Alaska Arizona California Colorado Florida Hawaii Idaho Montana Nevada New Mexico New York Oregon Texas Utah Washington (excl Group Health) Group Health Total All States Total Uncompensated Care for All Hospitals - 10/1/2014 - 9/30/2015 Estimated Per Claim Amount $8,321,249 150,330,961 $ 778.39 0.10% 1505.26 1.76% 1,058,279,674 2,381.14 75,279,990 1,281.80 97,209,416 5,974.11 17,759,171 1,293.88 21,442,732 1,152.79 9,812,103 652.13 57,993,655 1,282.58 45,707,445 1,299.18 937,520,318 2,095.46 67,365,102 1,168.60 732,239,185 1,705.56 38,059,158 4,342.04 129,946,883 12,071.53 897,284 448,642 $8,561,050,684 Total $ Nationwide $1,588.61 Average per claim % Uncompensated Care $ to Total $ 12.36% 0.88% 1.14% 0.21% 0.25% 0.11% 0.68% 0.53% 10.95% 0.79% 8.55% 0.44% 1.52% 0.01% MOSS ADAMS LLP | 46 100.00% MEDICAID ENROLLMENT AS A PERCENT OF TOTAL POPULATION & RECENT CHANGES KAISER FAMILY FOUNDATION Ranking State Medicaid Enrollment as % of Total Pop (2010-11) Medicaid Beneficiaries As of 2010 (est) % change in Medicaid Enrollment (2011-12) Status of State Action on the Medicaid Expansion Decision as of December 2013 1. District of Columbia 35% 210,603 +5% Implementing Expansion in 2014 2. California 31% 11,548,726 +2% Implementing Expansion in 2014 3. Maine 31% 411,792 -1% Not Moving Forward at this Time 4. Vermont 31% 193,980 +3% Implementing Expansion in 2014 5. New York 29% 5,619,650 +3% Implementing Expansion in 2014 6. New Mexico 28% 576,570 0% Implementing Expansion in 2014 27. Washington 20% 1,344,908 +5% Implementing Expansion in 2014 29. Hawaii 19% 258,457 +4% Implementing Expansion in 2014 30. Alaska 18% 127,842 +4% Not Moving Forward at this Time 39. Oregon 17% 651,283 +5% Implementing Expansion in 2014 46. Nevada 13% 351,072 +8% Implementing Expansion in 2014 United States 21% 65,711,913 +3% MOSS ADAMS LLP | 47 NEW HOSPITALS / NEWLY MERGED • • • Hospitals that merge after final rule issued to be treated similar to new hospitals Final uncompensated care determined at cost report settlement Once new hospital has established DSH eligibility, hospital eligible for uncompensated care payments o Calculated retroactively upon final settlement MOSS ADAMS LLP | 48 DSH – REALIGNMENT & REQUESTS REMINDER • 42 CFR 412.106(b)(3) allows a hospital to request to have the SSI ratio recomputed based on the hospital’s cost report yearend MOSS ADAMS LLP | 49 MEDICARE BAD DEBT • 42 CFR 413.89(e) Criteria for allowable bad debt. A bad debt must meet the following criteria to be allowable: • (1) The debt must be related to covered services and derived from deductible and coinsurance amounts. • (2) The provider must be able to establish that reasonable collection efforts were made. • (3) The debt was actually uncollectible when claimed as worthless. • (4) Sound business judgment established that there was no likelihood of recovery at any time in the future. 50 MEDICARE BAD DEBT Allowable Bad Debt Percentage for Cost Report Period Began 10/1/2012 Periods Began 10/1/2013 FFY 2015 (10/1/2014) and After Hospitals 65% 65% 65% SNFs, Non Dual Eligibles 65% 65% 65% Swing-Bed Hospitals, Non Dual Eligibles 65% 65% 65% SNFs & Swing-Bed Hospitals, Dual Eligibles 88% 76% 65% CAHs 88% 76% 65% ESRDs 88% 76% 65% CMHCs 88% 76% 65% FQHCs/RHCs 88% 76% 65% Cost Based HMOs 88% 76% 65% Health Care Pre-Payment Plans 88% 76% 65% Competitive Medical Health Plans 88% 76% 65% Provider Type MOSS ADAMS LLP | 51 MEDICARE BAD DEBT • Two Categories of Bad Debt: Indigent and NonIndigent (i.e. Regular) o No collection effort required for indigent but must bill to Medicaid to ensure there is no obligation by the State to pay o Regular bad debt must exhaust all collection efforts before it can be claimed for reimbursement on the Medicare cost report 52 MEDICARE MANAGED CARE DAYS • Used in the calculation of Graduate Medical Education (GME) payment reimbursement • Simulated DRG payment originating from Medicare managed care days is used in Indirect Medical Education (IME) payment reimbursement • Used in the calculation of HIT payment reimbursement • Used in the calculation of the SSI ratio of the DSH payment calculation 53 MEDICARE MANAGED CARE DAYS • Medicare managed care days must be billed to the Medicare Administrative Contractor (MAC) and a no-pay bill must be generated in order to ensure these days are counted for GME, IME, HIT and DSH payment purposes. • Providers are required to submit no-pay bills for all Medicare managed care activity. • PS&R Report 118 – Medicare managed care activity 54 CHARITY CARE • Reported on Worksheet S-10 • Instructions are vague and inconsistent • CMS to issue uniform instructions at some point in the future • Used as a component of the HIT payment • Could be used in the future as a proxy to distribute the DSH uncompensated care payment 55 PROTESTED AMOUNTS • What is a Protested Amount List and Why is it Important? o In simplistic terms it’s a list of disputed issues o Allows one to file a compliant Medicare cost report while preserving an avenue to benefit from court litigation on a disputed issue o Cannot file an appeal unless there is an audit adjustment – CMS requires audit adjustments of protested amounts in NPRs o Successful appeals provide future revenue streams • Appeals are Now Developed Prior to Cost Report Filing MOSS ADAMS LLP | 56 PROTESTED AMOUNTS • Key Elements of a Compliant Protested Amount List o Must fully describe your issue in dispute o Must provide an accurate protested amount calculation that fully identifies the disputed data element(s), DSH disputed patients etc. o Calculation is becoming as important as description of the issue in dispute. o Must ensure your calculated protested amount is input on the appropriate line of the cost report. MOSS ADAMS LLP | 57 PROTESTED AMOUNTS • Example of an Inadequate Protested Amount: o o o o o o DSH DSH SSI DSH Eligible Days FTEs HIT Payment Uncompensated Care Payment • Consequence: o Jurisdictional Challenge MOSS ADAMS LLP | 58 PROTESTED AMOUNTS • Example of a Compliant Protested Amount: o Understated DSH payments due to the fact the SSI Ratio, as published by CMS, is developed on a federal fiscal year basis in lieu of being developed on a cost report period basis MOSS ADAMS LLP | 59 PROTESTED AMOUNTS Protested Amounts to be Considered: 1. 2. 3. 4. 5. 6. 7. 8. 9. Accuracy of SSI Ratio SSI Ratio Realignment SSI Ratio Compliance with Section 951 of 2003 MMA CMS Ruling 1498R Non-Covered Part A Days in SSI Ratio CMS Ruling 1498R Non-Covered Part C Days in SSI Ratio Exclusion of DSH Non-Covered Dual Eligible Part A Days Exclusion of DSH Non-Covered Dual Eligible Part C Days Additional Medicaid Eligible Days DSH Uncompensated Care Payments MOSS ADAMS LLP | 60 PROTESTED AMOUNTS Protested Amounts to be Considered (cont.): 10. 11. 12. 13. 14. 15. 16. 17. 18. Understated HIT Payment due to Medicare Part C Days Understated HIT Payment due to Charity Care Charges 2 Midnight Rule 0.2 Payment Reduction Understated Nursing and Allied Health Payments Understated Medicare Bad Debt – Documentation Pending Understated Medicare Bad Debt – Share of Cost Claims Understated Medicare Bad Debt due to Write-Off Date Understated Medicare Settlement Data – Omitted Claims Understated Medicare Settlement Data – Incorrect Calc. MOSS ADAMS LLP | 61 PROTESTED AMOUNTS Protested Amounts to be Considered (cont.): 19. 20. 21. 22. 23. 24. 25. 26. 27. Omission of Low Volume Adjustment Add-On Payment LVA – Inclusion of Medicare Part C Discharges SCH – Errors in CMS 2007 Adjustment Factor SCH – Denial of Uncompensated Care Pool Payment I&R FTEs – Additional FTEs Not Claimed Understated GME / IME–Exclusion of Medicare Part C Days Understated GME / IME – Unaccredited Training Program Understated GME / IME – Time Spent in Elective Rotations Understated GME / IME – Initial Residency Programs MOSS ADAMS LLP | 62 PROTESTED AMOUNTS Protested Amounts to be Considered (cont.): 28. 29. 30. 31. 32. 33. 34. Understated GME / IME – FTE Cap & Affiliation Agreement Understated GME / IME – Prior Yr./Penultimate Yr. FTEs Understated IME – Prior Year Available Bed Count Understated IME – Licensed Bed v Available Bed Count Understated GME / IME – IRIS Program Software Errors Understated GME / IME – Understated Medicare Set Data Prior Year Audit Adjustments Incorporated in CY Cost Report MOSS ADAMS LLP | 63 BEST PRACTICES • Report Preparation o Documentation is first priority Maintaining accurate reports throughout year Staff turnover creates confusion & uncertainty Consistency and efficiency are key o Begin the process as early as possible o DILLY/SALY no longer are acceptable o Incorporating prior MAC adjustments 64 BEST PRACTICES • Reimbursement Optimization o Keeping up with regulations o Flexibility of mindsets and cost/benefit considerations • Department communication o Accounting and business office staff need to work in unison on cost report items 65 EXTRACTING USEFUL/OPTIMAL DATA • • • • Revenue Usage Reports Job Costing Detail (Labor Distribution Reports) Time-Study Logs Using PS&R for internal use 66 Questions? Thank you! Susan Ruchin (480) 366-8369 Susan.ruchin@mossadams.com Glenn Bunting (916) 503-8195 Glenn.bunting@mossadams.com 67