How to use this template #1 - present.knowledgevision.com

Interim results presentation

2013 Financial Year

Emery Severin – Chief Executive Officer

Ian Davis – Chief Financial Officer

21 February 2013

Disclaimer

This presentation has been prepared by Nuplex Industries Limited. The material that follows contains general background information about Nuplex’s activities as at the date of the presentation 21 February 2013.

The information in this presentation is not an offer or recommendation to purchase or subscribe for securities in Nuplex or to retain any securities currently held. It does not take into account the potential and current individual investment objectives or the financial situation of investors.

Actual results may vary materially either positively or negatively from any forecasts in this presentation. Before making or disposing of any investment in Nuplex securities, investors should consider the appropriateness of that investment in light of their individual investment objectives and financial situation, and seek their own professional advice.

All currencies are in NZD unless stated otherwise.

1

Safety

Making progress towards our goal of zero harm

Lost time injury frequency rate per million employee hours worked

15

10

5

0

0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 1H13

Total reportable injury frequency rate per million employee hours worked

30

20

10.2

10

0

FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 1H13

2

1H13 financial overview

Sales revenue

$828.7m

EBITDA 1

$57.6m

up 11.0% steady

NPAT 2 after significant items

$11.5m

down 52.3%

NPAT before significant items

$24.5m

down 9.6%

Earnings per share

5.8 cents down from 12.3 cents

Dividend per share

10 cents unchanged

Return of funds employed 3

9.8% down from 12.1%

Working capital to sales ratio

14.8% down from 16.5%

1 Earnings before interest, tax, depreciation and amortisation

2 Net profit after tax attributable to equity holders of the parent company

3 As defined by earnings before interest, tax and unusual items divided by average funds

All figures are in NZD unless otherwise stated

3

1H13 in review

Taking action to improve returns on funds employed

Existing operations steady despite significant weakness in Australia and volatility in Europe in November/ December

• Resins segment excluding acquisitions

– Volume growth due to Asia and Americas offsetting ANZ and Europe

– Unit margins up 3.4% 1

Strengthening Nuplex by reducing costs

• Restructuring Australia and New Zealand to adapt to changing markets

• Executing NuLEAP I - delivered $6m during 1H13, on track to deliver program target of

$30m net benefits by the end of the FY13

• Investing in NuLEAP II - procurement initiative to deliver $5.3m in 2H13, $12m in FY14

Acquisitions successfully integrated – delivering in line with forecast in FY13 and acquisition criteria

• Viverso on track to deliver EBITDA of €12m

• Nuplex Masterbatch on track to deliver EBITDA of A$5m

1. Defined as a unit margin as a percentage of sales = sales revenue minus raw material costs divided by tonnage

All figures in NZD unless otherwise stated

4

1H13 key financial outcomes

EBITDA

• Supported by Viverso and Masterbatch contributions

• Impacted by

‒ ANZ restructure and procurement costs

‒ Ongoing strength of the New Zealand dollar

1H13 vs 1H12 1

Geographic diversity supported existing operations

• Weakness in Australia and end-of-year slow down in

EMEA largely mitigated by growth in Asia and

Americas

Sales revenue

EBITDA

EBITDA before restructure and procurement costs

NPAT impacted by write downs

• $13m in significant items including

‒ $5.8m write down of obsolete equipment in ANZ

‒ $5.5m write down of Fibrelogic investment

NPAT after significant items

Interim dividend maintained at 10 cents per share

• Strong cash flows reflecting margin management and tight cost control

• Declared in context of the outlook for the full year

1 See slide 25 for underlying data, 2. Excluding acquisitions

All figures in NZD unless otherwise stated

NPAT before significant items and restructure and procurement costs

% growth constant FX

Group

14.8%

4.2%

14.8%

(50.3)%

8.9%

Existing operations 2

(2.7)%

(14.5)%

(5.3)%

(53.1)%

2.6%

5

1H13 earnings drivers

Solid EBITDA despite continued challenging market conditions particularly in

Australian coating resins business

$57.3m

3.2

(2.1)

$57.6m

0.5

(3.1)* 1.5*

(7.3)

(6.1) 8.6

(4.5)* 9.7

*

1H12

EBITDA

Resins volume *

Unit margin *

Specialties

Cost inflation

- wages, utilities etc

Other fixed costs

NuLEAP

- benefit increase from

1H12 to

1H13

Restructure and procurement costs at

1H12 FX rates

Viverso at 1H12

FX rates

Masterbatch at

1H12 FX rates

FX

Excluding the impact of NuLEAP initiatives and acquisitions

1H13

EBITDA

6

Meeting challenging market conditions in ANZ with action

Restructuring to improve returns

7 sites

Pre-restructure

Reducing capacity to meet future demand

• Closing 1 site in New Zealand,

2 in Australia

• Expected restructure costs $9.6m

1

• Closures to occur 1 st half FY14

Investing to improve efficiency and further reduce costs

• Investing $13m to improve customer responsiveness and efficiency 4 sites

Benefits to flow from 2H13

• 2H13: $0.5m in cost savings

• FY14: $3.7m cost savings, 0.5 cents EPS uplift

• FY15: fully realised $5.6m cost savings,

2 cents EPS uplift

1 Timing of expected restructure costs 1H13 $2.8m, 2H13 $4.0m, FY14 $2.8

All figures in NZD unless otherwise stated

Post-restructure

7

Meeting challenging market conditions with action

Improving procurement and delivering significant cost savings

NuLEAP I on track to deliver $30m net benefits by end FY13

• 1H13 $6m realised

‒ 40% procurement, 40% sales, 20% operating costs

‒ Resins segment unit margins up 3.4%

NuLEAP II transformative procurement initiative

• Adopting a center-led approach supported by regional hubs

• Invested $3.2m in 1H13

• Benefits from this initiative to flow from

2H13

‒ $5.3m in 2H13

‒ $12m in FY14

All figures in NZD unless otherwise stated

Decentralised

Country procurement managers

Site buyer

Center-led

Global category managers

Regional procurement managers

Implementing

• Strategic sourcing processes

• Category management disciplines

8

Global resins segment

Specialties

Resins

EBITDA including Viverso $45.2m down 3.6% (up 0.6% constant FX)

• Includes $6m in costs to restructure ANZ ($2.8m) and upfront costs of procurement initiative ($3.2m)

EBITDA excluding Viverso, restructure and procurement costs $42.4m down 8.5%

(down 6.4% constant FX)

Europe, Middle East & Africa (EMEA)

• 2.5% volume growth ex Viverso

– Growth in powder resins

– Decorative, Marine & Protective and Auto OEM resins segments weaker

• EBITDA ex Viverso €9.2m down 3.2%

– Earlier than usual end-of-year slowdown

– Increased R&D costs, contribution to employee fund

Viverso

• Integration complete with successful transition of complex IT systems

• 1H13 performance in line with management expectations

• On track to deliver €12m in FY13

• Focus now on operational improvement and leveraging product portfolio

Americas

• 3.7% volume growth

– Growth in higher margin

High End Metal coatings

• EBITDA US$7.3m up 40.4%

• Tight cost control

• Contribution from sale of

Viverso products

All figures in NZD unless otherwise stated

Asia

• 10.3% volume growth

– Growth in China (Auto OEM, Vehicle Refinish),

Indonesia (Decorative) & Malaysia (Regional exports)

• EBITDA US$12.1m up 16.3%

• Contribution from sale of Viverso products

• Vietnam impacted by slowdown in housing market. New capacity still expected to be filled in 4 years

Australia & New Zealand

• Volumes down 11.4%

• EBITDA A$3.8m down 56.8% after A$1.6m restructure costs

• Cyclical low construction activity impacted demand

• Importation of finished goods continued to impact manufacturing customers

• Margin management and cost control mitigated some of volume impact

9

ANZ specialties segment

EBITDA $12.4m up 19.2% (up 20.2% constant FX)

Specialties

Agency and distribution

Defensive sectors growing

• Food and nutrition growing due to chocolate

• Pharmaceutical and healthcare

• Ongoing weakness in plastics, foam, paints and coatings

Nuplex Masterbatch

Integration/restructure complete

• 2 sites closed

• Improved margins

• Enhanced customer offering: expanded colour range, black and performance additives

Delivering in line with acquisition base case

• On track to deliver A$5m

EBITDA in FY13

Resins

All figures in NZD unless otherwise stated

10

2. Financial results

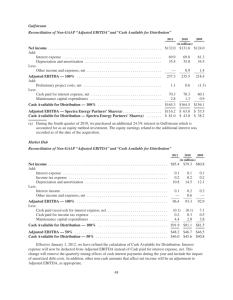

Financial results

NZ$ million

Sales

EBITDA

Depreciation and amortisation

EBIT

Net financing costs

Share of associates

Minority interests (non controlling interests)

Tax on operating profits

Underlying NPAT

Write downs

Legal provisions

Loss on sale of Plaster Systems NZ

Acquisition related costs

Income tax credit on non-operating items

NPAT attributable to equity holders of parent company

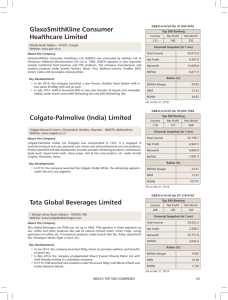

(7.7)

24.5

(13.6)

(0.3)

(0.7)

(0.8)

2.4

11.5

1H13

828.7

57.6

(16.0)

41.6

(9.1)

0.9

(1.2)

(9.2)

27.1

-

(0.4)

-

(2.6)

-

24.1

1H12

746.4

57.3

(12.2)

45.1

(6.5)

(1.3)

(1.0)

% change

11.0%

0.5%

30.7%

(7.7)%

38.6%

-

21.8%

(16.5)%

(9.6)%

(17.8)%

-

-

(71.5)%

-

(52.3)%

12

Reconciliation: EBITDA to cash flow

NZ$ million

EBITDA

Financing costs

Provisions/other

Loss on business disposal

Movement in working capital

Tax paid

Dividends from associates

Cash-flow from operations before significant items

Cash flow from significant items

Cash-flow from operations

Capital expenditure less proceeds of disposal

Cash flow

Dividends paid

Free cash flow

1H13

57.6

(9.1)

1.8

0.6

11.2

(14.3)

1.3

49.2

(1.7)

47.5

(18.8)

28.6

(18.7)

9.9

1H12

57.3

(6.5)

(2.0)

-

(9.9)

(15.9)

1.3

24.3

(3.0)

21.3

(13.0)

8.3

(22.3)

(14.1)

$ change

0.3

(2.6)

3.8

0.6

21.1

1.6

24.9

-

1.3

26.2

(5.8)

20.3

3.6

24

13

Working capital and capital expenditure

Working capital to sales ratio 14.8%

Stay in business capex

• 1H13: $12.2m, equivalent to 95.4% of depreciation

‒ $2.9m global ERP project

‒ $2.3m new reactors at Botany, Wacol, and East St.Louis

‒ $1.2m Suzhou Technical Centre

• FY13: expected to be 120% of depreciation

Working capital as a percentage of 12-month rolling sales

20%

18%

16%

Target range 15-17%

16.5

15.8

14.8

14%

12%

10%

Organic growth capex

• 1H13: $6.7m

‒ China new site $4.8m

• FY13 forecast approximately $20m

• FY14 forecast $25 to $30m

8%

6%

4%

2%

All figures in NZD unless otherwise stated

0%

Dec 08 Jun 09 Dec 09 Jun 10 Dec 10 Jun 11 Dec 11 June 12 Dec 12

14

Funding and gearing

$209m net debt as at 31 December 2012

• Largely unchanged from $220m as at

30 June 2012

Average cost of debt 6.6%

Completed US$105m US private placement funding

• 7 year term, mature 2019

• Coupon rate 6.125%

• Settled 31 July 2012

NZ$52.6m of Capital Notes redeemed

September 2012

Note: All figures are in NZD unless otherwise stated

Net debt to net debt plus equity ratio

60%

50%

40%

30%

Target range

20-35%

27.4%

20%

10%

0%

Dec 07 Dec 08 Dec 09 Dec 10 Dec 11 Dec 12

15

3. Strategy and outlook

We’re strengthening and growing Nuplex

Our ambition

Our strategy

FY2013

Execution

To be the leading, trusted independent polymer resins manufacturer globally, and leading agency and distribution business in ANZ

To achieve superior shareholder returns by delivering high quality products to our customers through pursuing operational excellence, innovation and building market leading positions

Strengthening through operational excellence Growing through building market leading positions

Safety

• Build a culture of

‘zero harm’

• Implementing global common standards relating to processes and policies

• Health &

Wellbeing program in ANZ

People

• Engage and leverage One

Global Team

• Introduce global

Overlay Teams to leverage products, R&D and procurement across the group

• Global Senior

Management

Conference

• Employee survey

• Nuplex

Leadership

Academy: online development program

NuLEAP

• Improve the way we work through rigorous improvement programs

• NuLEAP I

− Final phase of execution

• NuLEAP II

− Planning

− Procurement initiative

• Restructure of

Australia and

New Zealand

Emerging markets

• Profitably expand capacity and presence in emerging markets

• China: 3 rd site progressing

US$35m

• Indonesia: capacity expansion

US$5.4m

• Russia: finalising JV

• Thailand: capacity expansion

R&D

• Grow market share through innovative products

• Pursue market development opportunities

• Leverage technologies across global platform

• Preparing for launch of new products at

European

Coatings Show in March 2013

• Succession planning for

R&D personnel

Strategic acquisitions

• Consider acquisitions that

− Strengthen leading market

& technology positions

− Leverage capabilities

− Meet disciplined criteria

• Consolidation of recent acquisitions

− Integration

− Improving operational performance

− Leveraging benefits of product portfolio

17

Building leading positions where our markets are developing and growing

Sales by region 1

%

100%

China, Changshu

• Investing US$35m

• Double capacity in China

• Delayed 6 months

• Commissioning now expected end FY14

Americas

Asia

EMEA

100%

9

12

21

100%

9

16

31

9

20

34

Indonesia, Surabaya

• Investing US$5.4m

• Expanding capacity and adding new technology

• Commissioning expected end FY14

Thailand, Bangkok

• Joint venture

• Investing US$1.5m

• Expanding powder capacity 40%

• Funded from cash within JV

ANZ

58

FY09

44

FY12

37

FY15

Russia, Belgorod

• Joint venture negotiations nearing completion

• Expect to be operating 4 th quarter FY13

• Initial investment of €8m in existing plant

& equipment and working capital

– Nuplex equity investment €2.5m

• Working towards starting construction of new site in 2014

– estimated investment €20 million,

Nuplex share 50% expected

1. FY09 sales retranslated at FY12 exchange rates (base case 2 )

2. Forecast subject to unforeseen circumstances and economic uncertainty

18

FY13 guidance

2013 so far

ANZ

• New Zealand: in recovery mode

• Australia: bouncing along the bottom?

Asia

• China: signs of an upturn in China

• SE Asia: growing steadily

Europe

• While activity is volatile, demand steady

Americas

• Steady growth

FY13 earnings guidance

EBITDA now expected to be between $135m and $140m

• Assumes similar market conditions in 2H13

• Is based on 1H13 average exchange rates

• Acquisitions on track to deliver EBITDA targets; Viverso €12m, Nuplex Masterbatch $5m

• NuLEAP on track to deliver at least $13m

• Procurement initiative to deliver benefits of $5.3m in the second half

• ANZ restructure costs of $6.8m

Note: All figures are in NZD unless otherwise stated

19

FOR FURTHER DETAILS:

Emery Severin

Chief Executive Officer

+61 2 8036 0902

emery.severin@nuplex.com

Josie Ashton

Investor Relations

+61 2 8036 0906 or

+61 416 205 234

josie.ashton@nuplex.com