Market Economics

advertisement

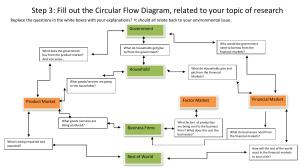

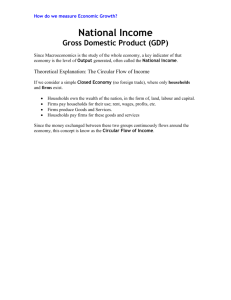

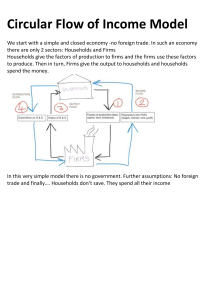

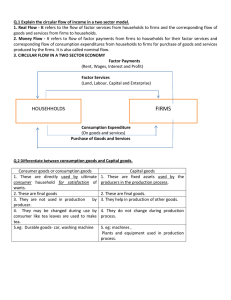

Current Issues - LHS • Supply – Reflects the amount of a product available to be purchased at a particular price – UPWARD slope • Higher the price, the more quantity of a product is available • Lower the price, the less quantity of a product is available – Suppliers produce more when prices are high b/c they make more money selling products at the higher price Supply Curve • Demand – Reflects the desire for a product at a particular price – DOWNWARD slope • The higher the price the less demand for a product • The lower the price, the more demand for a product – The higher the price, the lower the quantity someone buys Demand Curve • Finding “equilibrium” between supply and demand – Equilibrium = where supply, demand curves intersect – Means that the amount of goods being supplied is exactly the same as the amount of goods being demanded – When this happens, everyone is happy! (unfortunately, it’s only theoretical) • What happens to demand if price goes UP? • What happens to supply if price goes UP? • What happens to demand if price goes DOWN? • What happens to supply if price goes DOWN? • OC is the cost of any activity in terms of the value of the next best alternative that is not chosen • The “cost” is the lost opportunity that results from making your choice – Ex 1: Choosing between 2 TV shows (w/ no chance to record the one not watched) – Ex 2: College vs. working – Ex 3: Going to Disneyland vs. remodeling bathroom • Refers to shifts in the economy over time • Measured by the growth rate of the Gross Domestic Product – GDP = total market value of goods and services produced in a year – GDP per Capita = GDP per person – Used as a common comparison point between countries • Expansion (increase in production and prices) • Crisis (stock exchange crash, b/k) • Recession (drops in price, output) • Recovery (stocks recover b/c price, incomes fall) • Since WWII, business cycle has not been as extreme (gov’t use of fiscal, monetary policy to avoid worst effects) • Model showing the circulation of income between producers (businesses or “Firms”) and consumers (“Households”) • Firms use Factors of Production (Land, Labor, Capital) to produce goods and services • Shows how money circulates between businesses and households – If one part of model stops spending, what happens to economy? – Where does government fit in this model? • Where consumers are “households”, businesses are “firms”, and “factors” refer to factors of production (Land, Labor, Capital) • Two categories – Economic regulations seek to control prices • Prevent monopolies from gouging consumers • Stabilize agricultural prices – Anti-trust law strengthens market forces to avoid direct regulation • Prohibit practices that lessen competition • Prevent mergers that would limit competition • Other bases of government regulation – Protecting public’s health and safety – Maintain clean and healthy environment – Preventing businesses from failing • Bailouts, direct purchase of business by government • Nationalization of businesses: appropriate or not? • Conservatives usually support fewer regulations on business • They argue that regulations: – Interfere with free enterprise – Increase costs of doing business – Contribute to inflation • Is deregulation appropriate or not? Public utility deregulation