Understanding In-Service Withdrawals

advertisement

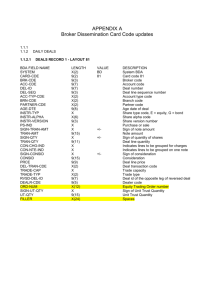

Understanding In-Service Withdrawals No bank guarantee • Not a deposit • May lose value • Not FDIC/NCUA insured • Not insured by any federal government agency 2/15 E24095-15A For broker/dealer use only. Not for use with the public. [Name of Financial Professional, Company Name] [Name of Pacific Life Wholesaler, Pacific Life] Please note that this presentation has been designed to provide general, introductory information. Neither Pacific Life nor its representatives offer legal or tax advice. Clients should consult their attorneys and tax advisors as to the applicability of this information to their specific circumstances. Pacific Life and its affiliates do not provide any employer-sponsored qualified plan administrative services or impartial investment advice and do not act in a fiduciary capacity for any plan. Please contact your plan administrator for any questions relating to your 401(k) plan. [Name of Financial Professional] and [Company] are not affiliated with Pacific Life or its affiliated companies. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. For broker/dealer use only. Not for use with the public. Agenda In-service withdrawals defined IRA rollover drawbacks vs. benefits Requesting a rollover Case study Summary For broker/dealer use only. Not for use with the public. In-Service Withdrawals Many participants are unaware that they may be able to access plan assets prior to retirement An in-service withdrawal provision allows participants of an employer-sponsored plan to take a distribution from the plan while still employed Withdrawals are often eligible for rollover For broker/dealer use only. Not for use with the public. In-Service Withdrawals Rules vary depending on the type of employersponsored plan: – Defined contribution (DC) plan – Defined benefit (DB) plan Employers may allow an in-service withdrawal feature, but they are not required to do so The law lays out allowable withdrawals, and plans may be more restrictive than the law allows For broker/dealer use only. Not for use with the public. What DC Plan Assets Can Be Withdrawn? Pretax elective deferrals – If age 59½ or a result of hardship Employer contributions – Profit-sharing or matching contributions – Fully vested and “two-year bake” rule satisfied After-tax contributions Rollovers from other retirement plans For broker/dealer use only. Not for use with the public. What DC Plan Assets Cannot Be Withdrawn? Elective employee salary deferrals – Unless triggering event is met Non-vested employer contributions “Two-year bake” rule – Fewer than five years of participation – Employer contributions must be held for at least two years – Not applicable with five years or more of participation For broker/dealer use only. Not for use with the public. Possible DC Plan Restrictions Plan may impose – Restrictions on class of assets – Restrictions on frequency and amount of withdrawals – Possible suspension of plan participation and employer match May have specific paperwork Contact employer for details and request copy of summary plan description For broker/dealer use only. Not for use with the public. In-Service Distribution from DB Plans Historically permitted in-service distributions at normal retirement age (NRA) only (e.g., age 65) Beginning in 2007, employers may amend plan allowing in-service feature at age 62 even if NRA is greater than 62 Hardship withdrawals prior to age 62 are not permitted For broker/dealer use only. Not for use with the public. Hardship and Nonhardship Hardship distributions are not eligible for rollover – Plan has option to permit “hardship distribution” – If granted, participant will have to suspend elective contributions for at least six months after hardship distribution is received Nonhardship distributions are generally eligible for rollover into: – Eligible retirement plan and avoid income tax and additional 10% early distribution tax – Roth IRA and avoid additional 10% early distribution tax but not income tax For broker/dealer use only. Not for use with the public. Advantages of In-Service Rollovers Wider array of investment options Greater distribution options Not subject to 20% mandatory withholding on distributions IRAs and qualified plans—such as 401(k)s and 403(b)s—are already tax-deferred. Therefore, a deferred annuity should only be used to fund an IRA or qualified plan to benefit from the annuity’s features other than tax deferral. These include lifetime income, death benefit options, and the ability to transfer among investment options without sales or withdrawal charges. For broker/dealer use only. Not for use with the public. Disadvantages of In-Service Rollovers Potential loss of: Exception to additional 10% early distribution tax if separated from service after attainment of age 55 and older Amounts available for loans Ability to delay required minimum distributions (RMDs) beyond age 70½ Tax advantages using net unrealized appreciation (NUA) strategy Inherited Roth IRA to beneficiaries Lifetime income provided through plan annuity options For broker/dealer use only. Not for use with the public. Some Reasons Not to Roll to an IRA Current qualified plan may offer: Lower cost funds Lower administrative expenses Greater level of service Loan features For broker/dealer use only. Not for use with the public. How to Do an In-Service Rollover Step one: Contact Human Resources – Does plan allow for in-service rollovers? – Obtain clarification of specific plan requirements AND restrictions on frequency/amounts/types of contributions – Obtain proper forms and instructions – Consult tax advisor For broker/dealer use only. Not for use with the public. How to Do an In-service Rollover Step two: Establish an IRA (traditional or Roth) rollover account – Determine investment product For broker/dealer use only. Not for use with the public. Hypothetical Case Study: Defined Contribution John, age 58, 20 years of service, XYZ Company 401(k) balance totals $850,000 – $400,000 in salary deferrals – $350,000 in matching contributions (XYZ stock) – $100,000 in rollover contributions John is not happy with plan investment options – Considering diversification of his retirement assets For broker/dealer use only. Not for use with the public. Hypothetical Case Study: Defined Contribution John verifies that his plan allows in-service distributions of: – Rollover contributions at any time – Nonhardship withdrawals of employer stock contributions – Salary deferrals beginning at age 59½ Diversify stock position and rollover contributions now directly to IRA Plans to roll salary deferral contributions at age 59½ For broker/dealer use only. Not for use with the public. Why Employers Might Adopt an In-Service Option for Employees Appealing to employees Mitigate employer liability Lower participant balance might be less likely to take legal action against the employer For broker/dealer use only. Not for use with the public. Act Today Check your book for clients who are: Employed and active participants in 401(k), profit-sharing, stock bonus, or defined benefit plans Concerned that a large portion of their retirement assets are allocated to employer company stock Looking for investment options not offered at the plan level For broker/dealer use only. Not for use with the public. Retirement Strategies Group Available to do CE and client seminars Insurance CPA, CFP®, PACE E-mail: RetirementStrategiesGroup@PacificLife.com For broker/dealer use only. Not for use with the public. More Information Contact our Advanced Marketing Group (800) 722-2333, ext. 3939 AdvMkt@PacificLife.com For broker/dealer use only. Not for use with the public. This material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding U.S. federal, state, or local tax penalties. This material is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by this material. Pacific Life, its affiliates, their distributors, and respective representatives do not provide tax, accounting, or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney. For broker/dealer use only. Not for use with the public. Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues. Variable insurance products are distributed by Pacific Select Distributors, LLC (member FINRA & SIPC), a subsidiary of Pacific Life Insurance Company and affiliate of Pacific Life & Annuity Company. Variable and fixed annuity products are available through licensed third-party broker/dealers. (Newport Beach, CA) For broker/dealer use only. Not for use with the public.