Grading Summary

advertisement

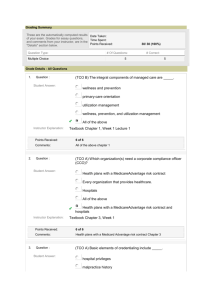

Grading Summary These are the automatically computed results of your exam. Grades for essay questions, and comments from your instructor, are in the "Details" section below. Date Taken: Time Spent: Points Received: Question Type: Multiple Choice 30 / 30 (100%) # Of Questions: 10 # Correct: 10 Grade Details 1. Question : Student Answer: (TCO 2) Operating budgets and financial budgets have nothing to do with the master budget. are prepared after the master budget. combined, form the master budget. Instructor Explanation: Points Received: are prepared before the master budget. Chapter 6, Page 182 3 of 3 Comments: 2. Question : Student Answer: (TCO 2) To gain the benefits of budgeting, ________ must understand and support the budget. customers management at all levels suppliers Instructor Explanation: Points Received: All of the above Chapter 6, Page 184 3 of 3 Comments: 3. Question : Student Answer: (TCO 2) Which budget is not necessary to prepare the budgeted balance sheet? Revenues budget Budgeted income statement Cash budget Instructor Explanation: Budgeted statement of cash flows Chapter 6, Page 187 Points Received: 3 of 3 Comments: 4. Question : Student Answer: (TCO 2) A feature of a standard-costing system is that the costs of every product or service planned to be worked on during the period can be computed at the start of that period. This feature of standard costing makes it possible to maintain actual costs as an integral part of the costing system. use a simple recording system. eliminate routine reports. Instructor Explanation: Points Received: justify eliminating the budgeting process. Chapter 7, Page 232 3 of 3 Comments: 5. Question : Student Answer: (TCO 2) An unfavorable variance indicates that actual costs are less than budgeted costs. actual revenues exceed budgeted revenues. the actual amount decreased operating income relative to the budgeted amount. Instructor Explanation: Points Received: All of the above Chapter 7, Page 227 3 of 3 Comments: 6. Question : Student Answer: (TCO 2) Which of the following statements is true about overhead cost variance analysis using activity-based costing? Overhead cost variances are calculated for output-unit level costs only. Overhead cost variances are calculated for variable manufacturing overhead costs only. A four-variance analysis can be conducted. Instructor Explanation: Points Received: Activity-based costing uses input measures for all activities, resulting in the inability to do flexible budgets needed for variance analysis. Chapter 8, Page 275 3 of 3 Comments: 7. Question : Student Answer: (TCO 2) Overhead costs have been increasing due to all of the following except product proliferation. tracing more costs as direct costs with the help of technology. more complexity in distribution processes. Instructor Explanation: Points Received: increased automation. Chapter 8, Pages 261-262 3 of 3 Comments: 8. Question : Student Answer: (TCO 2) Katie Enterprises reports the year-end information from 20X8 as follows: Sales (70,000 units) $560,000; Cost of goods sold 210,000; Gross margin 350,000; Operating expenses 200,000; Operating income $150,000. Katie is developing the 20X9 budget. In 20X9, the company would like to increase selling prices by 4%, and as a result expects a decrease in sales volume of 10%. All other operating expenses are expected to remain constant. Assume that COGS is a variable cost and that operating expenses are a fixed cost. What is budgeted sales for 20X9? $582,400 $524,160 $504,000 Instructor Explanation: $560,000 Sale price ($560,000 / 70,000) X 1.04 = $8.32 new price per unit 70,000 x (1- .10) = 63,000 units to be sold Sales $8.32 x 63,000 = $524,160 Points Received: 3 of 3 Comments: 9. Question : (TCO 2) Hester Company budgets on an annual basis for its fiscal year. The following beginning and ending inventory levels (in units) are planned for the fiscal year of July 1, 2008, through June 30, 2009. July 1, 2008 2009 Raw material (note) 40,000 June 30, 10,000 Work in process 8,000 8,000 Finished goods 30,000 5,000 (note) Three units of raw material are needed to produce each unit of finished product. If Hester Company plans to sell 600,000 units during the 20082009 fiscal year, the number of units it would have to manufacture during the year would be Student Answer: 625,000. 575,000. 540,000. 640,000. 600,000 + 5,000 finished goods ending inventory - 30,000 finished goods beginning inventory = 575,000 Instructor Explanation: Points Received: 3 of 3 Comments: 10. Question : (TCO 2) Information pertaining to Brenton Corporation's sales revenue is presented in the following table: February March April Cash Sales $120,000 Credit Sales 280,000 Total Sales $400,000 $160,000 $150,000 300,000 400,000 $460,000 $550,000 Management estimates that 5% of credit sales are not collectible. Of the credit sales that are collectible, 60% are collected in the month of sale and the remainder in the month following the sale. Cost of purchases of inventory each month are 70% of the next month's projected total sales. ll purchases of inventory are on account; 25% are paid in the month of purchase, and the remainder is paid in the month following the purchase. Brenton's budgeted total cash payments in March for inventory purchases are Student Answer: $385,000. $358,750. $306,250. Instructor $280,000. ($400,000 X 70% X 25%) + ($550,000 X 70% X 75%) = $358,750 Explanation: Points Received: Comments: 3 of 3