Theory of the Firm

advertisement

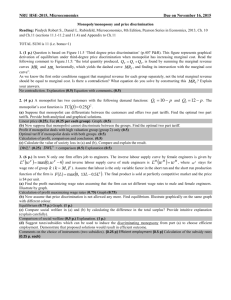

6th Quiz - Econ 202 - key 1. From the above graph, total revenue at the profit-maximizing quantity of output is area outlined by points 0Q0FP3. 2. From the graph above, the amount of positive economic profits earned by this monopolist is illustrated by the area outlined by points P2CFP3. 3. Which of the following is an assumption of the theory of oligopoly? Firms produce and sell either homogeneous or differentiated products. 4. In what industry structure is the mutual interdependence of the firms an important feature? oligopoly 5. A monopolistically competitive firm maximizes profits by producing at the point where marginal revenue equals marginal cost. 6. Which of the following conditions would prevent price discrimination? the inability to identify those customers willing to pay more 7. The economic inefficiency of a monopolist can be measured by the deadweight loss. 8. Competition is legally prohibited when barriers to entry are artificial barriers. 9. From the above table, the profit-maximizing single-price monopolist should produce (this question requires some calculations) 5 units. 10. The monopolistic competitor faces a downward-sloping demand curve and therefore is a price searcher. 11. The perfectly competitive firm charges a price ____ while the monopolistically competitive firm charges a price ____. equal to marginal cost, greater than marginal cost 12. The monopolist's marginal revenue curve is downward sloping and twice as steep as demand. 13. A monopolistically competitive firm is producing at an output level in the short run where average total cost is $3.50, price is $3.00, marginal revenue is $1.50, and marginal cost is $1.50. This firm is operating with an economic loss in the short run. 14. When oligopolists collude the results are generally smaller output and higher price 15. In maximizing profits, a monopolist will charge a price that is greater than marginal cost. 16. What area represents consumer surplus if an oligopoly exercises market power in this market? a 17. What area represents consumer surplus if oligopolists engage in a “price war”? a+b+c 18. A perfectly competitive industry is in long-run equilibrium. If demand for the product decreases, we can expect the price of the good to: falls at first and then rises. 19. In a perfectly competitive industry, in the long run: firms earn zero economic profit.