Common Sense Economics - 10 Key Elements of Economics

advertisement

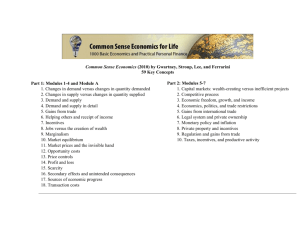

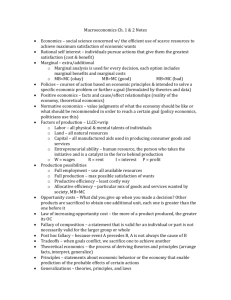

Common Sense Economics What Everyone Should Know About Wealth & Prosperity by James Gwartney, Richard Stroup, and Dwight Lee 10 Key Elements of Economics CommonSenseEconomics.com Ten Key Elements of Economics Provide an introductory flavor for the course Bridge between common sense & basic principles of economics Begin to help you “think like an economist” Provide some explanation as to why our economy and our world work the way they do 1. Incentives matter. What are Incentives? Incentives are the costs and benefits of making specific decisions. Changing incentives alters people’s behavior. Incentives operate on all levels- personal, familial, industry and societal level. Gasoline Prices… When the price of gas rises, do you change your behavior? Do you really? What’s the difference between short-run changes and long-run changes in behavior? Volunteerism… Incentives don’t matter only to the greedy and selfish. What incentives do volunteers have, if not monetary? Why do you volunteer? Seat belts save lives… Does wearing a seat belt create any incentives? Why do people get in more accidents now that cars are safer? 2. There is no such thing as a free lunch. The condition of scarcity Our resources are limited…but our desire for goods & services is NOT. When production costs are high, it is because the resource in question is desired for other purpose(s) as well. A resource is scarce if it has more than one valuable use. To Choose is to Refuse Because we are constantly faced with scarcity, we must make choices. Every time we choose one thing (material or not) we refuse something else. We constantly make tradeoffs in our decisions. But, but, but… What if someone else buys your lunch? Merely a shifting of cost, not an elimination And is it really free? 3. Decisions are made at the margin. Marginalism… Few, if any, decisions are “all-or-nothing”. Marginal means additional… Marginalism is seldom ignored in our personal decisions, but frequently in our conversations and in politics. To get the most out of our resources, we should only take an action when the marginal benefits are greater than the marginal costs. Marginal Decision Examples… How clean is your house? Do you clean to 100% cleanliness? How about when company is coming? How about when selling your house? You clean to the point where the marginal costs outweigh the expected marginal benefits! 4. Trade promotes economic progress. People gain when they trade… Trade moves goods from people who value them less to people who value them more. Trade makes larger outputs/consumption possible as we specialize. Voluntary exchange allows production costs to fall through mass production. Trade exists at many levels… Enrolling in this class Shopping at Safeway Having a garage sale Taking a vacation Buying imports from China & Mexico 5. Transaction costs are an obstacle to trade. Transaction Costs Spending resources on: Searching out trading partners Searching out product information Negotiating terms of trade Closing sales Why do we experience transaction costs? Physical objects Can’t get there from here! Lack of information Finding sellers/ best deals Political obstacles Taxes, tariffs, licensing requirements, regulations, etc. Role of middlemen? Increase or decrease TC? 6. Profits direct business toward activities that increase wealth. Why profits are not the enemy… People of a nation are better off if their resources produce valuable goods & services. Less productive use of resources should thus be discouraged. This is the function of profits and losses. Profit is a reward for transforming resources into something of greater value. Losses just as important! A T-shirt factory has total production costs of $20,000. 1,000 T-shirts sold at $22 each = $2,000 in profit. Wealth has been created for the producer and consumer. What if shirts can only be sold for $17 each? T-shirts are worth less to consumers than the resources required to produce them. What’s the trade-off if firms continue to operate at a loss? 7. People earn income by helping others. Earning Income People are different in many ways…This is our greatest asset! Differences in income arise because they affect the value of goods and services individuals are willing to provide. There is a direct link (ceteris paribus) between helping others & income. If you want a large income- figure out how to help others!!! Income Variation College students are rewarded for studying Star athletes and entertainers are rewarded for their special skills Entrepreneurs are rewarded for their innovations. 8. Economic progress comes primarily through trade, investment, better ways of doing things, and sound economic institutions. What is Economic Progress? Americans produce and earn THIRTY TIMES as much as they did in 1750. Why are Americans so much more productive today than they were 250 years ago? Why is economic progress important? Sources of Economic Growth Investments in productive assets Tools, machines, “human capital” Improvements in technology Internal combustion engine, electricity, computers, by-pass surgeries, etc. Improvements in economic organization Legal system, competitive markets, etc. 9. The “invisible hand” of market prices directs buyers and sellers toward activities that promote the general welfare. Invisible What? Adam Smith, The Wealth of Nations (1776) “It is his own advantage, indeed, and not that of society which he has in his view. But the study of his own advantage naturally, or rather necessarily, leads him to prefer that employment which is most advantageous to society…He intends only his own gain, and he is in this, as in many other cases, led by an invisible hand to promote an end which was not part of his intention.” Friedrich von Hayek Primary function of markets is to provide information (both to buyers and sellers) Consider the price of apples… Price indicative of what consumers are willing and able to pay, but also incorporates costs of production/bringing to market Things constantly happen to make both consumer value & production costs vary… 10. Too often long-term consequences, or the secondary effects, of an action are ignored. Unintended Consequences Perhaps the most common source of economic error. Actions often promote secondary effects. Tariffs & quotas to protect domestic industries Paying for pencils in the 2nd grade class