microconomics3_std - Rose

advertisement

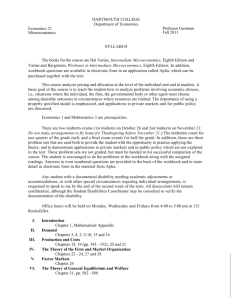

SL354, Intermediate Microeconomics

Monday

Week 1 :

March 3 – 7

Week 2 :

March 10 – 14

Week 3 :

March 17 – 21

Week 4 :

March 24 – 28

Week 5 :

April 7 – 11

Week 6 :

April 14 – 18

Week 7 :

April 21 – 25

Week 8 :

April 28 – May 2

Week 9 :

May 5 – 9

Week 10 :

May 12 – 16

Tuesday

Thursday

Friday

Introduction

Varian, 1

Budget Constraints

Varian, 2

Preferences

Varian, 3

Utility

Varian, 4

Choice

Varian, 5

Consumer Demand

Varian, 6 [7]

S. & I. Effects

Varian, 8

Problem Set 1

Thaler, 1 – 3

Buying & Selling

Varian, 9

Buying & Selling

Varian, 9

Intertemporal Choice

Varian, 10; Thaler, 8 – 9

Market Demand

Varian, 15

Equilibrium

Varian, 16

Problem Set 2

Asset Markets

Varian, 11

Uncertainty (Risk)

Varian, 12

Risky Assets

Varian, 13

Portfolio Theory

TBD

Loss Aversion, etc.

Thaler, 6 – 7

Capital Markets I

Thaler, 10 – 11

Capital Markets II

Thaler, 12 and 14

Problem Set 3

Technology

Varian, 18

Profit Maximization

Varian, 19

Exchange

Varian, 31

Welfare

Varian, 33

General Equilibrium

TBD

Problem Set 4

Auctions

Varian, 17

Auctions

Thaler, 5

Externalities

Varian, 34

Exam 1

Exam 3

Production

Varian, 32

Exam 4

Information

Varian, 35

Asymmetric Information Problem Set 5

Varian, 37

Thaler, 15

Exam 2

Exam 5

Intertemporal Trades

C2

(1 + r )m1 + m2

m2

•E

0

= {m1 , m2 }

A c1 , c2

•

c2

I0

1 r

m1

c1

Borrowing

in period 1

m2

m1 +

(1 + r )

C1

Intertemporal Trades

C2

C2

C1 = C2

C1 = C2

C1

C1

Patient preferences

Impatient preferences

(Negative time preference)

(Positive time preference)

Asset Markets: Debt

Asset Markets: Debt

Dow Jones Industrial Index

16,000

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

Jan-08

$0

Jan-07

$0

Jan-06

$100

Jan-05

$10

Jan-04

$20

Jan-03

$400

Jan-02

General Electric

Jan-01

$30

Jan-00

$500

Jan-99

$40

Jan-98

$50

Jan-97

Jan-08

Jan-07

Jan-06

Jan-05

Jan-04

Jan-03

Jan-02

Jan-01

Jan-00

Jan-99

Jan-98

Jan-97

Jan-96

$60

Jan-96

Jan-08

Jan-07

Jan-06

Jan-05

Jan-04

Jan-03

Jan-02

Jan-01

Jan-00

Jan-99

Jan-98

Jan-97

Jan-96

Asset Markets: Equity

Google

$800

$700

$600

$300

$200

S&P 500 Index

1,800

1,600

1,400

1,200

1,000

800

600

400

200

0

Asset Markets: Equity

Average Annual Returns*

GE Average

1982-2005

24%

100%

SP500 Average

1982-2005

12.3%

80%

60%

40%

20%

-40%

S&P 500 Index

*Calculated from a value-weighted index of all publicly traded stocks using CRSP data.

*Calculated as compounded annual return on average monthly returns from preceding 12 months.

General Electric

Jan-04

Jan-02

Jan-00

Jan-98

Jan-96

Jan-94

Jan-92

Jan-90

Jan-88

Jan-86

Jan-84

-20%

Jan-82

0%

Present Valuation Techniques and Asset Valuation

The present value (PV) of an amount to be received at time t (FV) when the perperiod discount rate is r:

PV

FV

1 r t

The present value (PV) of a stream of future values, when the per-period discount

rate is r:

n

FV0

FVn

FVt

FV1

PV

1 r 0 1 r 1

1 r n t 0 1 r t

Bond pricing. The price of a bond will be the net present value of interest

payments and the maturity date and value.

Stock valuation. The current value of a firm (PVFirm) is the present value of the

stream of future profits that the firm will generate -- and shareholders are

“residual claimants” of those profits:

PVFirm

t

1 r

t 0

t

Optimal Holding Period for an Asset

$350

24%

22%

$300

20%

FV t

$250

18%

16%

$200

14%

12%

$150

10%

8%

$100

PV t

$50

0

1

2

Time

3

4

5

6

7

8

t*

9

10

11

12

13

14

15

16

17

18

19

4%

2%

Rate of return from holding asset

$0

6%

0%

20

Risk and Uncertainty: “Contingent Consumption Plans”

Case 2:

A person with an endowment of

$35,000 faces a 1% probability of

losing $10,000. He is considering

the purchase of full insurance

against the loss for $100.

Case 1:

A person with an endowment of

$100 is considering the purchase

of a lottery ticket that costs $5.

The winning ticket in the lottery

gets $200.

$100

Lucky

day

Do not

purchase

Purchase

Do not

purchase

Lucky

day

$295

If

Pr(Lucky) = 0.025):

Purchase

$35,000

Outcome A:

E x $34 ,900

x $995

Unlucky

day

$25,000

Lucky

day

$34,900

Outcome B:

E x $100

x $31

Unlucky

day

$95

E x $34 ,900

x 0

Unlucky

day

$34,900

Risk and Uncertainty: “Contingent Consumption Plans”

CGood

$35,000

Lucky

day

Do not

purchase

• E

C g0 , Cb0

C g0 $35,000

Purchase

Unlucky

day

Lucky

day

Unlucky

day

C 1g $34 ,900

C

1

b

C g0 K

A C 1g , Cb1

•

$25,000

$34,900

$34,900

I0

1

Cb0 $25,000

C

0

b

C g0 K

C

Cb1 $34,900

1

b

Cb0 K K

K = the “expected loss” ($10,000), and K is the insurance premium.

C Bad

Economic Treatment of Risk

The Meaning of Risk Aversion

1. Risk aversion is defined through peoples’ choices:

Given a choice between two options with equal expected values and

different standard deviations, a risk averse person will choose the option

with the lower standard deviation:

If EX1 EX 2 , and 1

2

, then1 2

Given a choice between two options with equal standard deviations and

different expected values, a risk-averse person will choose the option

with the higher expected value:

If 1

2

, and EX1 EX 2 , then1 2

2. Non-linearity in the utility of wealth.

Dealing With Risk: Insurance

$100,000

Pr(xA) = .990

E[X] = $99,500

= $4,975

cv = 0.0500

Pr(xB) = .010

$50,000

Dealing With Risk: Insurance

Pr(xA) = .990

$100,000

$500

$99,500

E[X] = $99,500

= $0

cv = 0

$100,000

Pr(xB) = .010

$100,000

$500

- $50,000

+ $50,000

$99,500

Dealing With Risk: Insurance

For a risk-averse person . . .

E[X] = $99,500

= $0

cv = 0

Is

Preferable

to

E[X] = $99,500

= $4,975

cv = 0.0500

Can we find another option, keeping = $0, but with a lower

E[X], that will be considered equal to the original? For example,

suppose that for this risk-averse person . . .

E[X] = $99,415

= $0

cv = 0

Is

Equivalent

to

E[X] = $99,500

= $4,975

cv = 0.0500

Dealing With Risk: Insurance

If, for a risk-averse person . . .

$99,415

Is

Equivalent

to

E[X] = $99,500

= $4,975

cv = 0.0500

Then $99,415 is called a certainty equivalent.

Furthermore, we will be able to sell an insurance policy to this

person for $585.

The $85 difference between the amount the person will pay and

the expected loss is called a risk premium.

Economic Treatment of Risk

Utility

The Meaning of Risk Aversion

A

l

U3

l

U2

U1

l

B

U($)

D

l

C

Risk Premium

$0

$99,415

$99,500

$100,000

$

$50,000

U 1 U $50,000

U 2 U $99,415 EU 99,500

U 3 U $100,000

Economic Treatment of Risk

Utility

Risk Aversion and Risk Neutrality

U($)

U($)

U($)

$

Economic Treatment of Risk

Utility

Risk Tolerance

U1($)

U2($)

Risk Premium 1

Risk Premium 2

$

Risk Premium 1 > Risk Premium 2 :

Agent 1 is more risk averse than Agent 2

Agent 2 is more risk tolerant than Agent 1

Modeling Risk and Expected Utility in Insurance Problems

Expected Utility:

E Utility

pr( x ) * x

n

n

n

If n 2, E U pr x1 *U x1 pr x2 *U x2

Certainty Equivalent:

U CE EU

Risk Premium:

RP Ex CE

Dealing With Risk: Diversification (Portfolio Theory)

Expected Return of a Portfolio (2 investments):

E r1,2

E r1,2 Expected return of a portfolio comprised of investments 1 and 2

w1E r1 w2 E r2 , where

wi Weight of investment i in the portfolio

E ri Expected return of investment i

Expected Variance of a Portfolio (2 investments):

12,2

12,2 Variance of the portfolio

w Weight of investment i in the porfolio

w1212 w22 22 2w1w21,2 , where i

i2 Variance of investment i

Covariance of investments 1 and 2

1,2

Dealing With Risk: Diversification (Portfolio Theory)

Portfolio Example

Weight:

Pr(•)

0.200

0.200

0.200

0.200

0.200

State

1

2

3

4

5

0.5

x

11.00%

9.00%

25.00%

7.00%

-2.00%

0.5

y

-3.00%

15.00%

2.00%

20.00%

6.00%

10.00%

0.76%

8.72%

0.87

8.00%

0.71%

8.41%

1.05

x,y

4.00%

12.00%

13.50%

13.50%

2.00%

.

E[i]

Var(i)

(i)

c.v.

Cov(x,y)

Var(x,y)

(x,y)

c.v.

9.00%

E rx, y wx Erx wy E ry

-0.24%

2

0.25% x, y

4.97%

0.55

wx2 x2 w2y y2 2wx wy cov rx , ry

where : cov rx , ry x, y x y

Capital Asset Pricing Model

Capital Market Line

Security Market Line

r = E[return of a portfolio ]

r = E[return of a security ]

rx = rf +

rm - rf

m

rm

X

(

)

ri = rf + ri - rf i

rm

rx

rm - rf

rf

rm - r f

m

rf

x

m

cov(rx , rm )

Beta, ≡

var (rm )

1

i

Capital Asset Pricing Model

25

Returns

20

15

10

5

0

0.0

0.2

0.4

Mutual Fund Name

American Century Heritage A

Fidelity Advisor Equity Growth T

Fidelity Magellan

Putnam International Growth & Income

Fidelity Diversified International

Templeton Growth A

Vanguard 500 Index

Vanguard Total Stock Market Index

Vanguard PRIMECAP

Janis Growth & Income

Dreyfus Premier Balanced B

Dreyfus Founders Balanced A

0.6

Symbol

ATHAX

FAEGX

FMAGX

PNGAX

FDIVX

TEPLX

VFINX

VTSMX

VPMCX

JAGIX

PRBBX

FRIDX

0.8

Beta

1.0

1.2

1.4

1.6

3-Year

5-Year

10-Year

Beta

Returns Beta

Returns Beta

Returns

1.44

20.50

1.17

19.26

0.96

8.42

1.18

8.31

1.16

11.20

1.16

3.34

1.33

6.88

1.03

10.42

1.04

3.53

1.07

12.55

1.03

20.56

0.96

6.90

1.08

14.57

1.02

22.18

0.96

10.85

0.77

5.78

0.85

14.81

0.80

7.01

1.00

5.72

1.00

11.18

1.00

3.43

1.04

6.19

1.04

12.27

1.01

3.89

1.01

9.63

1.06

15.78

1.08

8.50

1.13

6.69

1.05

11.22

0.98

5.84

0.98

4.05

0.90

6.59

0.87

1.43

0.98

3.71

0.88

7.21

Capital Asset Pricing Model

cov(rx , rm )

Beta, ≡

var (rm )

Name

Symbol

Beta

Aetna

AET

1.08

Anheuser Busch

BUD

0.60

Bank of America

BAC

0.32

Boeing

BA

0.88

Cummins Inc.

CMI

1.35

Deere & Co.

DELL

1.23

Dell

DELL

1.81

Eli Lilly Co.

LLY

0.43

Family Dollar Stores

FDO

0.82

General Electric

GE

0.70

General Motors

GM

1.27

GOOG

2.01

Intel

INTC

1.72

J.P. Morgan Chase

JPM

0.68

Microsoft

MSFT

1.61

Nordstrom Inc.

JWN

1.51

PF

0.75

Wal-Mart Stores

WMT

-0.18

Wellpoint Inc.

WLP

0.61

Wells Fargo

WFC

0.32

Google

Pfizer

Economic Analysis of Market Opportunities

Efficient Markets and Economic Profits –

Total Market Returns, Selected Time Periods

Monthly:

Value-Weighted Equal-Weighted

Index

Index

Annual:

Value-Weighted Equal-Weighted

Index

Index

1/80 to 12/02:

AVG

STDEV

0.0108

0.0464

0.0202

0.0548

0.1370

0.7234

0.2708

0.8974

1/97 to 12/99:

AVG

STDEV

0.0208

0.0501

0.0250

0.0579

0.2805

0.7981

0.3450

0.9643

1/00 to 12/02:

AVG

STDEV

-0.0115

0.0564

0.0109

0.0778

-0.1298

0.9319

0.1385

1.4576

1/97 to 12/01:

AVG

STDEV

0.0046

0.0554

0.0179

0.0685

0.0572

0.9103

0.2378

1.2135

1980s:

AVG

STDEV

0.0139

0.0482

0.0152

0.0530

0.1798

0.7591

0.1986

0.8585

1990s:

AVG

STDEV

0.0143

0.0393

0.0279

0.0474

0.1859

0.5883

0.3916

0.7428

Loss Aversion

You are offered the following bet:

A coin will be tossed. If it is heads you

win x; if it is tails, you lose y.

“Most respondents in a sample of undergraduates refused to stake $10 on

the toss of a coin if they stood to win less than $30.”

Value = V($)

+v

- $10

+ (Loss)

+ $30

-v

+ (Gain)