Take Aways - NavigatingAccounting.com

advertisement

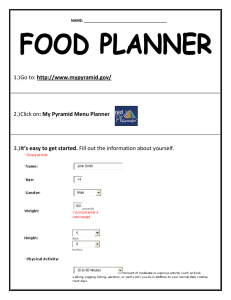

Making Informed Judgments Part 6 Factors Driving the Dispersion of Measures ® Navigating Accounting, G. Peter & Carolyn R. Wilson, © 1991-2009 NavAcc LLC. Modified by [Your Name]. Menu Ideal measurement distributions Everyone is an objective expert No need for authoritative guidance Actual measurement distributions Not everyone is perfect; Some preparers are dishonest or stretch the truth; Others lack the requisite expertise Users can not perfectly determine preparers’ expertise and/or objectivity There is a need for authoritative guidance and other mechanisms that aim to discipline reporting How the factors can inform accounting judgments Closing thoughts 2 View in Slide Show Mode > click hyperlink. Ideal Measurement Distributions Things You Need to Know Measurement objectives specify qualitative features or dimensions of an asset. Fair value The price a company would receive for an asset in an orderly transaction between market participants on the reporting date. Depends on the future benefits an unrelated party would expect to realize as of the reporting date by using the asset. Value in use The benefits the company expects to realize as of the reporting date by using the asset. Historical cost An asset’s cost to the entity when acquired, possibly adjusted for Return to menu 3 benefits used up by the reporting date. Ideal Measurement Distributions Question Answer the following question from the perspective of a representative student in your group: Compare the availability and reliability of information objective experts would seek to measure the fair value of your car to the information they would seek to measure its historical cost adjusted for usage? Assume you have owned the car for three years. Return to menu 4 Ideal Measurement Distributions Take Aways To estimate the historical cost of your car adjusted for usage, objective experts would mostly rely on information they would get from you to: Determine or estimate its historical cost Estimate, at the acquisition date, the expected pattern of the future benefits you expect to realize through usage and disposal of the car. Possibly modify this pattern over time for changes in expectations regarding future usage and disposal. To estimate the car’s fair value, the objective experts would need information from you regarding the car’s past usage and current condition and recent sales prices for comparable cars from other sources. Return to menu 5 Ideal Measurement Distributions Question Answer the following question from the perspective of a representative student in your group: How, if at all, would you expect the dispersion of objective experts’ estimates of the historical cost of your human capital to differ from the dispersion of their estimates of its value in use? Return to menu 6 Ideal Measurement Distributions Take Aways The dispersion of objective experts’ estimates of the historical cost of your human capital would likely be considerably narrower than the dispersion of their estimates of its value in use. To estimate its historical cost they would need to know what it cost to support you up to this point in your life and, more specifically, the portion of these costs that helped you develop your human capital. This would not be easy but the uncertainty regarding the inputs to this estimation would probably be considerably less than the uncertainty associated with predicting the way you will use this human capital to generate income in the future. Return to menu 7 Ideal Measurement Distributions Things You Need to Know Once experts know a measurement objective, they must select a measurement technique from acceptable alternatives and locate the inputs needed to apply the technique, including related assumptions. The average value of recent comparable sales would be a technique for estimating the fair value of your car on a reporting date: the price you would receive in an orderly transaction with market participants (car buyers). The closing stock price on the reporting date for a share of common stock you own would be a measurement technique for estimating the stock’s fair value. The present value of the future net cash flows a factory is expected to generate would be a technique for measuring its value in use. Return to menu 8 Ideal Measurement Distributions Things You Need to Know Benchmark data consists of inputs providing a basis for comparison. Companies derive estimates by applying a formula or technique to benchmark data. Three types of benchmarks are widely used: Market prices for recent trades Comparable company (cross-sectional) data Historical (time series) data Return to menu 9 Ideal Measurement Distributions Things You Need to Know The risks and uncertainties associated with the measurement context tend to be: Directly related to the dispersion of objective experts’ estimates. Inversely related to the availability and reliability of benchmark data: The number of benchmark observations and … The extent to which the business context associated with these observations is comparable to the measurement context. Return to menu 10 Ideal Measurement Distributions Question Answer the following questions from the perspective of a representative student in your group: If it exists, identify readily available and relatively reliable benchmark data that could be used to estimate the following measurement objectives: The fair value of your car The fair value of a patent you hold on an invention The portion of year-end accounts receivable owed to a company that are not expected to be collected in the future When might you be most concerned about the reliability of benchmark data that is readily available? Why did banks find it difficult to reliably predict bad debts associated with loans and other “toxic” assets in 2008? Return to menu 11 Ideal Measurement Distributions Take Aways The dispersion of the ideal estimates depends on: the measurement objective the business risks and uncertainties associated with the measurement objective the availability and reliability of benchmark data the availability and validity of measurement techniques the extent to which the business context associated with the benchmark data is comparable to the measurement context. The relative importance of these factors depends on the measurement context. Return to menu 12 Ideal Measurement Distributions Take Aways GAAP often restricts the measurement process when there are too many opportunities for dishonest reporting or unintentional errors. This tends to occur when the dispersion of objective experts’ estimates becomes large. GAAP restrictions are a net benefit to society to the extent: The benefits of restricting preparers who would otherwise act dishonestly or inadvertently make errors outweighs. The costs of preventing preparers who are objective experts from reporting their best estimates when the related measurement procedures do not conform with GAAP. Return to menu 13 Ideal Measurement Distributions Take Aways Understanding the factors that drive the dispersion of objective experts’ estimates can help you qualitatively gauge the dispersion. This, in turn, can help you: 1. Understand the reasons GAAP restrictions exist and how they evolve over time as the factors that affect the dispersions change. For example, as reliable benchmark data has become more readily available. 2. Gauge how close reported numbers are to the ideal measures that would have been reported if there were no GAAP restrictions and all preparers were objective experts. 3. Gauge the confidence you should have in reported numbers when making decisions based on them. Return to menu 14 Actual Measurement Distributions Things you need to know Generally, the factors that affect the ideal distributions of objective experts’ estimates also affect the actual distributions that occur under GAAP. However, several other factors affect the actual distributions. These tend to have one or more of the following effects on measurements; Help honest preparers avoid unintentional errors. Give preparers incentives to report dishonestly or otherwise commit frauds. The mere presence of these incentives does not mean preparers will necessarily act on them. Discipline preparers not to act on incentives to report dishonestly when given opportunities to do so. Return to menu 15 Actual Measurement Distributions Question Answer the following questions from the perspective of a representative student in your group: What are some honest errors you could make when estimating the following: The historical cost of your car adjusted for usage? The fair value of your car? The value in use of you human capital? What are some things you could do to reduce these errors? GAAP requires companies to estimate accounts receivable at the end of reporting periods that will probably not be collected in the future. What are some related honest errors that could occur and how can companies try to control them? Return to menu 16 Actual Measurement Distributions Take Aways Honest errors generally occur when: Preparers do not know what they should do: they lack the requisite knowledge. They know what they should do but they do not know how to do it: they lack the requisite skill. They know what they should do and how to do it, but they inadvertently fail to do it: they lack the requisite focus. Here are some ways to control these errors: Training is the best way to ensure preparers have the requisite knowledge and skills. Accountability, performance rewards and penalties, and otherwise promoting goal congruence can motivate focus. Return to menu 17 Actual Measurement Distributions Question Answer the following questions from the perspective of a representative student in your group: What are some rewards you can receive for reporting the values of your assets dishonestly or otherwise taking actions that serve your self interests at society’s expense? For example, what are some rewards you can receive by misrepresenting your qualifications during a job interview or cheating on exams to misrepresent your grades? Return to menu 18 Actual Measurement Distributions Question Answer the following questions from the perspective of a representative student in your group: What are some situations where you have particularly strong incentives (reasons) to report dishonestly or otherwise behave inappropriately to secure these rewards? What are some situations where these same rewards can motivate honest individuals to take actions that serve their self interests and society’s interests? Return to menu 19 Actual Measurement Distributions Take Aways Conflicts of interest exist when individuals have opportunities to take actions that serve their own interests at others’ expense. Conflicts of interest and opportunities to act on them inappropriately are pervasive and they were likely the root cause of the scandals that nearly collapsed stock markets in 2001-2002 and credit markets in 2007-2009. During these tumultuous events, far too many of the individuals who prepared financial reports, audited them, regulated them, based recommendations on them, and otherwise used them served their own interests, often excessively, at the expense of society’s interests. Return to menu 20 Actual Measurement Distributions Take Aways This excessive greed might lead you to conclude that conflicts of interest should be eliminated. Sometimes this is the best course of action, but not always: In a capitalist economy conflicts of interest are often the unintended side effects of financial incentives that create tremendous social benefits. Removing them by curbing or eliminating the incentives that cause them throws out the baby with the bath water, so this radical surgery should only be performed as a last resort. An alternative approach is to create or refine disciplining mechanisms that give individuals incentives (reasons) not to act in their own interests at society’s expense when they confront conflicts of interest. We will examine some of these mechanisms next. Return to menu 21 Actual Measurement Distributions Question Answer the following questions from the perspective of a representative student in your group: What are some things that would motivate you not to act inappropriately on the following conflicts of interest: Cheating on exams or graded assignments to boost your grades and ultimately misrepresent the value of your human capital? Lying to a car salesman when he asks you whether a car you are trading in for a new one has ever been in a serious accident and thus misrepresenting the value of your car? What are some things that would motivate a company not to report inflated asset measures? Return to menu 22 Actual Measurement Distributions Take Aways The figure below illustrates factors that affect accounting judgments, including financial incentives that can benefit or harm society’s interests and disciplining mechanisms that can curb or eliminate inappropriate behavior: Return to menu 23 Actual Measurement Distributions Take Aways These disciplining mechanisms all failed at Enron, WorldCom, Tyco, and other companies during the 20012002 scandals when there was a perfect storm of opportunities and incentives to commit fraud. Return to menu 24 Actual Measurement Distributions Take Aways For the most part, Sarbanes Oxley and other reforms passed in response to the scandals increased the restrictions associated with the disciplining mechanisms: Return to menu 25 How the Factors Can Inform Judgments Question How can understanding the factors below that influence measurement when everyone is not an objective expert and the additional factors that affect the dispersion of objective experts’ estimates help preparers increase the credibility of the measures they report? Return to menu 26 How the Factors Can Inform Judgments Question How can understanding these factors help users assess the credibility of the measures they are analyzing? Return to menu 27 How the Factors Can Inform Judgments Question How can understanding these factors help you better understand GAAP? For example, how can they help you better understand why research costs are expensed rather than capitalized? Return to menu 28 How the Factors Can Inform Judgments Take Aways When assessing the usefulness of reported numbers for their decisions, outsiders can gauge how reliably the numbers measure what they are intended to measure and how relevant this measurement objective is to their decisions. To assess reliability, they can assess the impact of the factors that affected the measures, including factors that affect the dispersion of objective experts’ estimates and the additional factors that must be considered because unfortunately some preparers are dishonest and others lack the requite expertise. Return to menu 29 How the Factors Can Inform Judgments Take Aways Recognizing that users make these assessments, preparers can increase the credibility of reported measures by disclosing accompanying information about the factors that affect their reliability. These factors can help you understand GAAP. For example: The reasons U.S. GAAP requires expensing research and development costs and IFRS permits capitalizing development costs when certain conditions are met. The reasons revenue recognition must be deferred when companies do not have benchmark data that allows them to reliably predict bad debts or product returns. Return to menu 30 Closing Thoughts The factors that affect measurement and other accounting judgments are intertwined and contextual, often differing significantly over time as globalization and technology evolves and across countries, industries, companies, and individuals: Return to menu 31 Closing Thoughts Considering the dramatic transformations that have occurred in these contexts and will likely continue to occur, the half life of facts you learn about current standards, regulations, and institutions will probably be quite short. Return to menu 32 Closing Thoughts For this reason, it is important that you understand how these factors evolve and relate to each other. The related concepts have proven to be very durable: They survived and, in fact, help explain the near collapse of stock markets in 2001-2002 and credit markets in 2007-2009. Return to menu 33