Chapter 11

advertisement

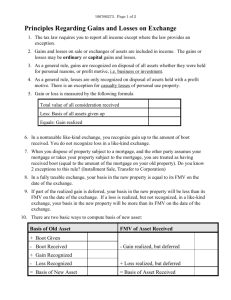

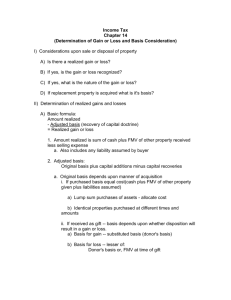

Chapter 11 Tax Consequence of Property Disposal Computation of Realized Gain or Loss Everything of economic value received in exchange for a property comprises the consideration If seller receives other property or services as part of the transaction, these must be included at their fair market value Difference between consideration received and the adjusted tax basis at the time of the transaction is the realized gain or loss on disposal Tax Treatment of Realized Gain or Loss Gains are ordinary income when they result from recapture of depreciation allowances. Gains are also ordinary income when they result from selling real estate that has been held for resale in the normal course of business (dealer property). Gains on the sale or exchange of real estate held for business or investment purposes are capital gains. If the holding period exceeds one year, the gain is a long-term capital gain. Tax Treatment of Realized Losses Real estate used in a trade or business (includes actively managed rental property) and held for more than one year are called Section 1231 assets. Gains on their disposal are treated as capital gains, losses are treated as offsets against ordinary income. Losses on real estate held for investment purposes are capital losses. If the real estate is held for more than one year, the loss is a long-term capital loss Computing Net Gain or Loss on Sale of Assets Held for Use in Trade or Business Offset Section 1231 gains and losses against each other. Offset long-term capital gains against long-term capital losses Offset short-term capital against against short-term capital losses If there are net losses in one category and gains in the other, offset the two Tax Consequences Depends Upon Outcome of Offsetting Gains and Losses If outcome is net short-term gains, lump them with ordinary income If outcome is net long-term gains, they are taxed at the maximum rate of 15%, regardless of taxpayer’s marginal tax bracket. Recaptured depreciation is taxed at 25% If outcome is net losses, they are offset against ordinary income on a dollar-for-dollar basis, but only to the extent of $3,000 per year When Realized Gains or Losses Are Recognized Gains are realized when a transaction is completed They may be recognized (and tax consequences experienced) in that year or at another time Use of the Installment Method If seller takes back a promissory note in part payment for property, it may be possible to defer recognition of part of the taxable gain until principal amount of the note is collected Gain that may be deferred is the installment method gain –total gain minus any portion that represents recapture of accelerated depreciation allowances Use of the Installment Method Contract price is total selling price, less balance of any mortgage note payable by the purchaser to a third party Each year, recognized gain is determined by multiplying the amount of the sales price actually collected by the seller, multiplied by the ratio of the installment method gain to the contract price Use of the Installment Method Installment note must include a provision for reasonable rate of interest—otherwise, IRS imputes a reasonable rate and recalculates the tax consequences of the transaction Complex tax rules limit the extent to which a taxpayer can defer a gain by using the installment method when they themselves own substantial amount of mortgage indebtedness Like-Kind Exchanges (1031 Exchanges) An otherwise taxable gain realized on an exchange of like-kind assets need not be recognized in the year of the transaction. Tax liability is postponed until a future, taxable transaction occurs with respect to the newly acquired property. Like-Kind Exchanges (1031 Exchanges) Enabling legislation for likekind exchanges (called taxfree exchanges) is contained in Section 1031 of the Internal Revenue Code. Like-Kind Exchanges (1031 Exchanges) To qualify under Section 1031: Must have been bona fide exchange of assets involved Property conveyed must have been held for productive use in a trade or business or an investment and must be exchanged for like-kind property that is also to be used in a trade or business or held as an investment Property must be of like-kind Like-Kind Exchanges (1031 Exchanges) Certain types of property are specifically excluded form Section 1031 Foreign real estate is never considered like-kind with domestic real estate Tax Consequences of Like-Kind Exchanges If all property involved in an exchange qualifies as like-kind and all parties qualify, then no party to the exchange may recognize any gain or loss on the transaction. Should some of the property involved in an exchange fail the like-kind test, then some portion of a gain must be recognized in the year of the transaction. Receipt of property that does not meet the like-kind definition has the effect of partially disqualifying a gain from deferral under Section 1031. Gifts of Property Gifts and legacies are subjected to a unified, graduated gift and estate tax that is imposed on the person who makes a gift or to the estate of a decedent Gifts of Property Exemptions and exclusions from the gift and estate tax: One may give as much as $11,000 each to as man persons as one wishes each year with no gift tax implications ($22,000 for spouses) Unlimited exemption for gifts or legacies to a spouse who is a United States citizen Unlimited exemption for payment of tuition and medical expenses for others Gifts of Property Gifts are cumulative over the giver’s lifetime for purposes of determining the graduated tax rate, but gift taxes are due in the year the gift is made Each taxpayer has a lifetime credit against the unified gift and estate tax. The amount of the credit will shelter $1,000,000 Gifts of Property Gift of property that is subject to a mortgage will have sale as well as gift elements The tax basis of a recipient’s interest in property received as a gift is the same as the basis of the giver’s, unless the giver incurred a gift tax liability. Letting title pass as a legacy rather than a gift works better for highly appreciated property