chapter ten banker's acceptance

advertisement

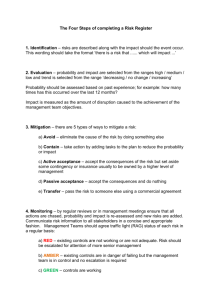

CHAPTER TEN BANKER’S ACCEPTANCE • It is a means of providing financing for international trade and creating a unique financial instrument that is attractive to money market investors. It facilitates and expands the sources of credits beyond a commercial bank. • A bankers acceptance is a time draft drawn by one party (the drawer) on a bank (the drawee) and accepted by the bank as the bank’s commitment to pay a third party (the payee) a stated sum on a specified future date. The bank promises to pay the draft at maturity. The bank creating an acceptance becomes primarily liable for the payment on the maturity date. • Through the bankers acceptance banks can provide credit to their customers without using the bank’s own funds. This is done by creating a negotiable instrument with a specified maturity date which can be sold at a discount to investors. • Figure 10.1 Banker’s Acceptance • The bank stamps “accepted” across the draft as shown in figure 10.1 with authorized signatures. Parties involved are: • The borrower. The importer (sight or time draft) • The seller. The exporter (sight or time draft) • The bank (own funds or lending) • The broker. Establishes contact between the people who wants to sell and buy bankers acceptances. • The investor. The person who buys the bankers acceptance in order to gain higher rate of return than time accounts or bank’s certificate of deposits. ELIGBLE BANKER’S ACCEPTANCE • In the USA banker’s acceptance drawn in accordance with the Federal Reserve Act are eligible for discount or purchase by a Federal Reserve Member bank at any of the Federal Reserve Banks. Usually they are discounting in private trading market. The conditions which are mentioned in the Fed Reserve Act are: • • • • • Importation or exportation of goods Domestic shipment of goods Storage of readily marketable staples Banker’s acceptance may be created for maximum term of six months. Eligible banker’s acceptance is exempt from reserve requirements and deposits insurance. A national bank may have banker’s acceptances outstanding up to 150% of the banks capital.