Situational Influences on Management Control Systems

advertisement

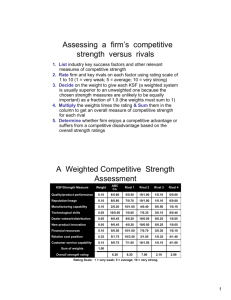

When is it Worth it? Chapter 5 Kent Thorén INDEK / KTH. Builds on Merchant and Van der Stede Recall that Controls benefit is a higher probability that people will both work hard and direct their energies to serve the organization’s interests. However, there are also costs of controls: Direct out-of-pocket costs Harmful side-effects 2 Effectiveness of Control Control system effectiveness depends on whether the direct and indirect costs of control are reasonable considering: 1. The (behavioral) benefits of the controls 2. The cost of not having control 3 Direct Costs The direct monetary costs related to operating control systems. For example: Investments in information systems. Managerial time spent on reporting and monitoring. Other administrative costs. Costs of rewards to make results controls and action accountability effective. 4 Direct Costs (cont.) Quantification of direct costs can be more or less straightforward: Easy to quantify: cost of cash bonuses, internal audit staffs, etc.; Difficult to quantify: time spend on planning and budgeting activities, on pre-action reviews, etc. 5 Indirect Costs Dysfunctional effects linked to different control systems Behavioral displacement Gamesmanship Operating delays Negative attitudes 6 Negative Attitudes Job tension, conflict, frustration, resistance, etc. Action controls often “annoy” professionals, but also lower-level personnel … Are often coincident with many harmful behaviors, such as, gaming, lack of effort, absenteeism, turnover, etc. Sometimes difficult to avoid: e.g., it is difficult for people to enjoy following a strict set of procedures for a long period of time ... Results controls ... Lack of employee commitment to the performance targets; targets are too difficult, not meaningful, not controllable. Performance evaluations are perceived as being unfair; The controls are implemented in a people-insensitive, nonsupportive way. 7 Design & Evaluation Chapter 6 A Framework for Making Control Systems Trade-offs 9 Control System Trade-offs II What is desired!? Key actions - i.e., actions that must be performed to provide the greatest probability of success. Key results – i.e. the few key areas where things must go right for the business to flourish. depend on strategy etc. What is likely!? Investigate potential for each control problem: Lack of direction, Motivational problems, Personal limitations. 10 Control System Trade-offs III Whenever “what is likely” differs form “what is desired”, two sets of design questions should be addressed: 1. Select types of controls 2. Choose how tightly to apply each type of control 11 A Simple Strategy Formulation Process 1. Identify KSFs of the industry 2. Review the firm in terms of how it meets the KSF 3. Compare with e.g. the largest rival (or several rivals) to make a more objective scoring 4. Project the future-state scoring to illustrate gaps 5. Use either the likely or the desired future state 6. Prioritize each KSF and draft high-level actions to maintain strong points, close critical gaps etc. This provides a starting point for strategy formulation 12 A Simple Strategy Formulation Process cont. Industry KSF Weakness Strength Raw material access Strategy Implications Secure raw material partnership Gap Manufactring yield R&D effectiveness Gap Improve R&D Gap Review and enhance sales network Time-to-market Sales network -2 -1 Equal +1 +2 Current position vs. main rival Desired future position vs. main rival Define Desired Behaviors 13 What is Desired? Customer buying process Awareness Appeal Prefer Purchase Direct influence Desired salesperson behavior Mention Advocate Compare Book 14 Start Outlining Control System Needs What is desired? Mention Advocate Compare Book What is likely? -Motivation -Direction -Limitations Mention of our products Poor promotion Not likely today On customer request Control system candidates? - (Tools and) (Tools and) (Tools and) Training Training Training Performance measurements Rewards PC + RC PC + RC Control system types PC 15 Then Set Performance Areas, Target Levels etc. Increase Activity Levles % of sales situations 100 Current 90 Target next FY 80 70 60 50 40 35-40% 30 20 10-12% 10 Mention Advocate Compare Book 16 Pros and Cons of Control Mechanisms Action controls Direct link between action and control Documentation and learning Efficient coordination (if technology is simple and stable) Proactive Stifling creativity and fast adaptation Foster sloppiness Negative attitudes Behavioral displacement risk Often costly (indirect costs) Results controls Feasibility due to monetary focus Can be used to enhance autonomy Relatively inexpensive Imperfect link to actions Shift risk to employees Risk of gamesmanship Motivation vs communication Costly (direct & indirect costs) Reactive Personnel Relatively inexpensive or cultural (except selection and training) controls Proactive Difficult to change quickly (particularly cultural controls) Requires significant trust 17 Pros and Cons of Control Mechanisms II The different types of controls (action, results and people controls) are not equally effective at addressing each of the control problems. Results accountability Action controls - Behavioral constraints - Preaction reviews - Action accountability Lack of direction Lack of motivation Personal limitations People controls - Selection / placement - Training - Provision of resources - Strong culture - Group-based rewards 18 Conclusions III Can people be avoided? (e.g., automation, centralization) Yes Control-problem avoidance No Yes Can you rely on people involved? No Yes Can you make people reliable? People controls No Have knowledge about what specific actions are desirable? Yes Able to assess whether specific action was taken? Yes No Action controls Have knowledge about what results are desirable? No Yes Able to measure results? Yes Results controls ? 19 Questions chapter 4 & 5 Consider how controls of gaming operations at Bellagio, if technology could be applied to monitor dealers work as proposed in the case; what control systems could be removed and why? What could the potential indirect costs be? 20 Questions chapter 6 AirTex does not really have a strategy. What if it was given a growth mission. What would the desired behavior be at each department? What potential control problems would be candidates for addressing with new control systems? 21 Strategic Missions The Four Missions: Build Hold Invest in MS even at the expense of ST-earnings / CFs Harvest Divest Maximize ST-earnings / CFs even at the expense of MS Protect MS and competitive position Outright sale Slow liquidation 22