Lecture

advertisement

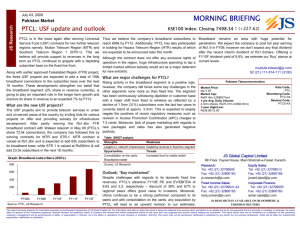

ROLE OF PTA IN THE DEVELOPMENT OF TELECOM SECTOR VISION Fair Regulatory Regime to Promote Investment , Encourage Competition, Protect Consumer Interest and Ensure High Quality ICT Services SEQUENCE PTA ORGANIZATION AND FUNCTIONS INDUSTRY SCENARIO INCETIVES TO THE INDUSTRY SECTOR LIBERALIZATION INDUSTRY PERFORMANCE TARIFF CHALLENGES Perspective PTA was established under the Telecom (ReOrganization) Act 1996 To regulate telecom system and services in Pakistan Headquarters in Islamabad. Regional Offices are in Karachi, Quetta, Lahore, Rawalpindi and Peshawar Autonomous Body Organization CHAIRMAN MEMBER (TECHNICAL) COORDINATION FINANCE LAW MEMBER (FINANCE) LICENSING WIRELESS LICENSING WIRE LINE INDUSTRY DEVELOPMENT ENFORCEMENT FAB COMMERCIAL AFFAIRS Functions Regulate telecom systems and services through fair, transparent and judicious regulatory framework • • • • Issuance of licenses for various telecom services Enforcement Protect the interests of users and service providers Investigate and adjudicate on complaints and other claims Process applications for radio frequency spectrum Promote modernization of telecommunication systems and services Make recommendations to the Federal Government on policy matters Telecom Scenario 2002 PTCL Monopoly on Fixed Line Telephony Cellular Mobile Sector –Stagnant Competition in Value Added Services (Small Operators) Pay phones ISPs Cable TV Low Tele Density Fixed 2.5 Total 3.5 Mobile 1.0 Incentives to the Industry 2001 (Reduction in Fee / Royalty) Mobile phone ISPs Royalty on Equipment Sale License Fee ISPs in Balochistan Satellite Service - From 4% to 1.5% - From 4% to 0.66% - From 5% to 0% - 50% - Fee & License Abolished (Registration Only) Type Approval Fee Locally Manufactured Equipment - 50% Foreign Manufactured Equipment - 33% Continue Incentives to the Industry 2001 (Reduction in Fee / Royalty) PTCL Leased Line Charges - 30% Reduction in 2002 For Mobile Operators - 17% Reduction in 2005 PTCL Leased Line Charges - up to 39% Reduction in 2005 For LL & LDI Operators Activation Charges For Mobile Phones - Rs. 2000 to Rs. 500 Advance Tax on Prepaid Cards - Rs. 125 to 45* *on card value of Rs. 500 SECTOR LIBERALIZATION Cellular Mobile New Licensing Open Auction for Award of Licenses -14 April 2004 ( US $ 10 MILLION Earnest money) Companies Participated in the Auction Highest Bid - 9 - US$ 291 Million (Existing Licensees to pay the same fee) WARID & TELENOR WARID & TELENOR Serviceability OPERATIONS Service Started WARID TELENOR May 2005 March 2005 Cities/ Towns Covered 28 (70 Jan 06) 3 (Now 160) No of BTs 536 (Now 617) 350 ( Now 1000) Deregulation Policy Open and Technology Neutral License Term – 20 Years (Review after 5 Years) License Categories • Local Loop (LL) • Long Distance & International (LDI) Issuance of LL & LDI Licenses Licenses Issued • LL – 79 • LDI - 13 License Fee • LL - US$ 10000 • LDI - US$ 500000 • (Performance Bond- US $10 MILLION) Spectrum Auction for WLL Spectrum auctioned through open bidding – Aug 2004 Spectrum allocated on regional basis Licenses Issued – 92 Fee Collected – RS 14 Billion NEW LICENSES CMT LDI LL (Fixed) WLL 2 13 79 92 Salient Regulatory Initiatives Determination on Interconnect Determination on Co-Location Determination on Limited Mobility SMP Status of PTCL and Mobilink Simplified VAS Licensing Regime Many licenses condensed into only two Some licenses replaced by registration Enabling environment for broadband penetration INDUSTRY PERFORMANCE Teledensity Growth (fixed telephony) Fixed Line Connections - 5,318,480 WLL Connections - 4,17,349 4.00% 3.70% 3.17% 3.50% 3.00% 2.27% 2.18% 2.10% 1.99% 2.00% 1.85% 1.91% 2.50% 2.70% 2.50% 1.50% 1.00% 0.50% 0.00% 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 Major WLL Companies • • • • • • PTCL TELECARD WORLD CALL GREAT BEAR DV COM BURAQ 238,202 132,500 43,114 3,511 starting the service soon starting the service soon Cellular Mobile Growth Penetration 12.7% 20,000,000 19598013 18,000,000 16,000,000 12,489,000 14,000,000 12,000,000 10,000,000 8,000,000 5,022,908 6,000,000 4,000,000 2,000,000 2,404,400 1,698,536 265,612 306,493 742,606 0 Jun 99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Nov\ Dec 2005 Cellular Mobile Sites Growth 7000 6500 6000 5000 4000 3000 2000 1000 1459 212 248 283 360 2000 2001 2002 2003 0 Years 2004 2005 Market Share of CMT Operators Warid Telenor 9% Instaphone 2% 8% PTML 23% Paktel 5% Mobilink 53% Pay Phone Growth Revenue to PTCL (Approx. Rs.10 billion) 300000 281600 250000 200439 200000 127910 150000 97751 100000 66968 50000 10400 0 2000 2001 2002 2003 Years 2004 2005 Internet Subscriber 2500000 Users - Approx 10 million Broadband Subscribers - 30,000 2000000 2100000 2000000 1600000 1500000 1000000 1000000 800000 500000 500000 0 2000 2001 2002 2003 2004 2005 REVENUE / INVESTMENT License /Spectrum Fee 20 16,765 2004 2005 18 - RS 16,765 BILLION - RS 12,257 BILLION 16 14 12 9,267 10 8 397 6 2,593 4 2 0 2004 2005 CMT 2005 WLL 2005 LL & LDI Cellular Mobile Revenue 100 Rs. in billion 100 90 80 70 60 50 40 30 20 10 0 63.6 34.9 19.8 2002-03 2003-04 2004-05 2005-06 Estimated GST/CED of Telecom Sector 25 20.4 Rs. Billion 20 15 11.5 8.8 10 5 0 12.1 FDI in Telecom Sector (% of Total Contribution in Total FDI) Total FDI – US $328.7MIL (July – Sept. 05) FDI in Telecom - US $91.4 MIL(July – Sept. 05) 35.00% 32.40% 27.80% 30.00% 25.00% 21.80% 20.00% 15.00% 10.00% 5.00% 1.26% 1.69% 2002 2003 0.00% 2004 2005 July -Sept. 05 Investment Made by Major Companies COMPANY Telenor (CMT) Warid (CMT) PTCL World Call TeleCard DV Com DanCom Burraq Telecom Redtone Existing Mobile Operators Total EXPECTED INVESTMENT (US $ Million) 400 392 273.3 115 165 38 12 21.5 38.2 645.5 2,100.5 TARIFF Tariff Reduction of PTCL Charges (Rs.) Incl. of 15% GST 1996 2003 2004 2005 Connection Charges 2500 Urban 1553 Rural 575 Urban 863 Rural 575 No change Line Rent 50 300 200 No change NWD Charges 42 / min 10 / min 6.04 / min 4.6 / min 74 / min 39 / min 23 / min 10.35 / min* International Calls * (Prepaid Card) Long Distance Call Rates Prepaid Calling Cards Domestic Long Distance (Rs.) International (Rs.)* 1.73 – 3.45 10.35 3.45 3.44 2.88 5.74 3.86 – 4.54 6.36 1.75 3.00 Burraq 1.71 – 3.09 4.59 Circlenet 2.04 – 3.05 3.98 Charges inclusive of 15% GST Company PTCL World Call DV Com Callmate Dancom * International tariffs vary from country to country and for calls to Mobile networks in different countries Local Call Rates - WLL Company Line Rent Rs. Same Network Other Networks PTCL 174 2.01/ 5 min 2.01/ 5 min Tele Card 149 0.40 / min 2.01/ 5 min World Call 175 Free 0.85 / min No Installation Charges Tariff Reduction Cellular Mobile Charges (Rs) 2000 2002 2004 2005 4.75 / min - Mobilink Prepaid Air Time (On-net) 6.25 / min Postpaid Air Time (On-net) 1.99 5.75 / min 5.00 / min - Ufone 1.5– 3.00/ min 3.75 / min - Paktel 1.50 1.00 0.75 Rs. 2.12 / min Fixed line to Local Mobile 3.20 / min 2.80 / min 2.80 / min Rs. 1.77 / min (July 06) Roaming Charges 5.0/min 6.0/min Free since October Free Achievements Unprecedented Growth in Telecom Sector Tariff Significantly Reduced Substantial Investment Made Economic Growth Employment Opportunities Healthy Competition Successful Holding APT Meeting Significant Role in Earthquake Relief Efforts Heavy license fee collected for the Government CHALLENGES Mobile Number Portability MNP Allows Users to Retain the Same Number While Switching Over to Another Operator Enhances Fair Competition 60% task completed MNP regime will be implemented in first half of 2006 Rural Communication Many Options to Extend Telecom Facilities (Use of WLL, VSAT, IP Technologies and Cellular Mobile) Plan to establish Tele-Centers through Micro Financing Implementation in consultations with local Governments Broadband High Speed (128 kbps & More) “Always On” Internet Connection Broadband Access a Catalyst for Economic & Social Development Broadband Penetration very low - 30,000 Approx Efforts in Hand to Enhance Penetration International connectivity will be enhanced soon Cost of Domestic Private Lease Circuits (DPLC) being reviewed Creation of enabling environments THANKS