ALL THAT’S NEW IN ILLINOIS

12th Annual Taxpayers’ Federation of Illinois

State and Local Tax Conference

September 20, 2011

Fred O. Marcus

Horwood Marcus & Berk, Chtd.

(312) 606-3210

fmarcus@hmblaw.com

Michael A. Lovett

PricewaterhouseCoopers LLP

(312) 298-5612

michael.a.lovett@us.pwc.com

Agenda

• Legislation

• Enacted

• Proposed

• Judicial

• Income / Franchise

• Other

• Regulations

• Adopted

• Projects on the Agenda

• Current Developments

2

Enacted Legislation (96th General Assembly)

S.B. 3655 Research and Development Credit

(P.A. 96-0937)(Signed 6/23/2010)

• Provides that the research and development credit applies

for taxable years ending on or after December 31, 2004

and ending prior to January 1, 2011

• Credit was to sunset on December 31, 2009 under Act’s

automatic sunset provisions

• Research and development credit may not be carried

forward to any taxable year ending on or after January 1,

2011

3

Enacted Legislation (96th General Assembly)

S.B. 1578 Small Business Jobs Creation Tax Credit

(P.A. 96-0888)(Signed 4/13/2010)

• Provides tax credit to small business by Department of

Commerce and Economic Opportunity (DCEO)

• Applies to taxpayers with fewer than 50 employees that

have hired a new employee during the State’s fiscal year

2011

• Credit not to exceed $2,500 ($50,000,000 total)

• Dept. Press Release “Illinois Small Business Jobs Creation

Tax Credit/Certificates from DCEO” (June 29, 2011)

• Reminder that the credit is only available to businesses and nonprofits that registered with the DCEO on or before June 20, 2011

• Clarifies when and how the credit is to be claimed

4

Enacted Legislation (96th General Assembly)

S.B. 3089 EDGE Tax Credits Expansion

(P.A. 96-0905)(Signed 6/4/2010)

• Expands the provision allowing certain motor vehicle

manufacturer to elect to claim the EDGE credit against

their withholding tax obligations to apply to heavy duty

truck manufacturer that meet certain criteria

• Intended to allow certain taxpayer to take advantage of the

provisions of P.A. 96-834, which passed during veto

session

5

Enacted Legislation (96th General Assembly)

S.B. 2505 (P.A. 96-1496)(Signed 1/13/2011)

• Corporate income tax rate increased from 4.8% to 7% beginning on

January 1, 2011

• On January 1, 2015, the rate decreases to 5.25%

• Reduced again to 4.8% on January 1, 2025

• Note that Illinois also imposes a 2.5% replacement tax on

corporations

• Special rules apply to fiscal-year taxpayers

• Taxpayers with tax years that overlap date on which a rate change

occurs can use a weighted average of the two rates or can elect to

specifically account for income and expenses earned during each

part of the tax year

6

Enacted Legislation (96th General Assembly)

S.B. 2505 (P.A. 96-1496)(Signed 1/13/2011)

• For all corporations (excluding S corporations), NOL

carryovers are suspended for tax years ending after

December 31, 2010 and prior to December 31, 2014

• No taxable year for which a deduction is suspended

will be counted

• Fiscal year taxpayers have a four-year suspension

• The rule suspending carryovers does not contain an

exception for corporations whose final taxable year

falls within the period of suspension. IT 11-0013-GIL

(July 8, 2011)

7

Enacted Legislation (97th General Assembly)

Income Tax

• SB 4 – Amends EDGE Act (P.A. 97-0002)(Signed

5/6/2011)

• Provides election to claim EDGE Credit against

withholding tax obligations for certain narrowly

defined industries

• Contains recapture provisions for not meeting

investment or job creation and retention requirements

• Provides that taxpayers may not take credits awarded

pursuant to Film Production Services Tax Credit Act

for tax years beginning on or after 5 years after

effective date of SB 4

8

Enacted Legislation (97th General Assembly)

Income Tax

• SB 398 (P.A. 97-0003)(Signed 5/6/2011) – Film

Production Services Tax Credit Act

• Amends Film Production Services Tax Credit Act of

2008

• Provides that taxpayers not entitled to take credit for

tax years beginning on or after 10 years (instead of 5

years) after the effective date of SB 4

• Provides that General Assembly may extend sunset

date by 5 year intervals

9

Enacted Legislation (97th General Assembly)

Income Tax

• SB 2168 (P.A. 97-0203)(Signed 7/28/2011)

• River Edge Historic Rehabilitation Tax Credit

• Creates credit equal to 25% of qualified expenditures incurred

by eligible taxpayer for restoration and preservation of

qualified historic structure located in River Edge

Redevelopment Zone

• The qualifying expenditure must equal at least $5,000 or more

and must exceed 50% of the purchase price of the property

• Applicable to tax years beginning on or after January 1, 2012

and ending prior to January 1, 2017

10

Enacted Legislation (97th General Assembly)

Income Tax

• HB 2955 (P.A. 97-0507)(Signed 8/23/2011)

• Technical Corrections Bill

• Broad technical correction bill that amends the Income Tax Act

to achieve consistency with the IRS Code and clarifies the State’s

approach to taxation linked to insurance premiums, net losses,

life insurance income, and income from a real estate mortgage

investment conduit

• Various administrative and technical changes

• Provides that deduction for partnership personal service income

and income distributable to entities subject to Replacement Tax

are not subject to sunset provisions

• Many of the provisions have different effective dates

11

Enacted Legislation (97th General Assembly)

Income Tax

HB 2955 (P.A. 97-0507)(Signed 8/23/2011)

• Technical Corrections Bill

• Broadly permits full and partial combination of holding companies by

amending IITA Section 1501(a)(27)’s exception to allow combination of

a “holding company that would otherwise be a member of a unitary

business group with taxpayers that apportion business income under any

of subsections (b), (c), or (d) of Section 304”

• Defines what a holding company is and how the income and

apportionment factors should be allocated to the unitary groups

• The holding company provisions are intended to clarify existing law

12

Enacted Legislation (97th General Assembly)

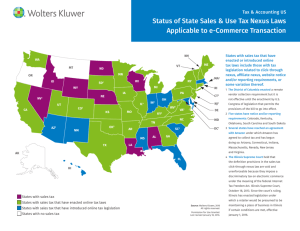

Sales/Use Tax

• HB 3659 (P.A. 96-1544)(Signed 3/10/2011)

• Amends Illinois use tax and service use tax laws, beginning

7/1/2011, by adopting click-through nexus provisions applicable

to certain retailers

• $10,000 threshold of total sales from in-state relationships

during the preceding 4 quarterly periods

• Unlike in other states adopting similar “click-through” nexus

provisions, there is no “presumption” that nexus exists that

can be rebutted by the out-of-state retailers

• Also adopts expanded affiliate nexus provisions for certain

retailers that use the same marks/trade names as in-state

businesses

13

Enacted Legislation (97th General Assembly)

Sales/ Use Tax

• SB 0145 (P.A. 97-0038)(Signed 6/28/2011)

• Nursing Home Care Act; Exemptions for certain food and medicine

• Provides that the exemption applicable to goods purchased for use

by a person receiving medical assistance under Art. 5 of the Public

Aid Code also applies to a person who resides in a licensed facility

as defined in the Specialized Mental Health Rehabilitation Act

(SMHRA)

• Provides a reduced 1% service occupation tax and service use tax

rate applies to food prepared for immediate consumption and

transferred incident to a sale of service by an entity licensed under

the SMHRA

14

Enacted Legislation (97th General Assembly)

Sales/ Use Tax

• SB 401 (P.A. 97-0073)(Signed 6/30/2011)

• Use Tax-Centralized Purchasing (Temporary Storage Exemption)

• Extends exemption to June 30, 2016 for use of tangible personal

property purchased from an Illinois retailer by a taxpayer engaged

in centralized purchasing activities in Illinois who will, upon

receipt of the property in the state, temporarily store the property

in Illinois (i) for the purpose of subsequently transporting it

outside the state for use or consumption solely outside Illinois or

(ii) for purpose of being processed, fabricated, or manufactured

into, attached to, or incorporated into other tangible personal

property to be transported outside Illinois and used or consumed

solely outside Illinois

15

Enacted Legislation (97th General Assembly)

Property Tax

• HB 212 (P.A. 97-0577)(Signed 8/26/2011)

• Business Corridor Abatement

• HB 1218(P.A. 97-0577)(Signed 8/25/2011)

• Tax Purchaser/Sale Transparency

• HB 1926 (P.A. 97-0451)(Signed 8/19/2011)

• Housing Authority Exemption

• HB 234(P.A. 97-0296)(Signed 8/11/2011)

• Open Space Valuation Changes

• SB 1804 (P.A. 97-0533)(Signed 8/23/2011)

• Special Service Area Property Tax Covenants

16

Enacted Legislation (97th General Assembly)

Property Tax

• SB 1386 (P.A. 97-0521)(Signed 8/23/2011)

• Property Tax Overpayments

• HB 1518(P.A. 97-0481(Signed 8/22/2011)

• Senior Citizen Real Estate Tax Deferral/High Speed Rail Property

Valuation

17

Enacted Legislation (97th General Assembly)

Unclaimed Property

• HB 1560 (P.A. 97-0270)(Signed 8/8/2011)

• Unclaimed Wages - Limitation

• Amends 765 ILCS 1025/2 and 2a

• Provides that unclaimed wages, payroll and salary held or

owing by a banking or financial institution will be presumed

abandoned if outstanding for more than one year from the

date of issuance

• Additionally, business associations shall report unclaimed

wages, payroll and salary, in any form, after remaining

unclaimed for more than one year

• Effective August 8, 2011

18

Enacted Legislation (97th General Assembly)

Miscellaneous Taxes

• SB 43 (P.A. 97-0353)(Signed 8/12/2011)

• Taxation Disclosure Act

• Provides that the Department of Revenue shall make tax rate

information available on its website, including:

Municipal rate information for use and occupation tax;

Corporate income tax rates; and

State and local excise tax rates

• Provides that the information required to be provided must be

made available in a viewable and downloadable format, and

must be updated regularly

• Effective July 1, 2012

19

Enacted Legislation (97th General Assembly)

Miscellaneous Taxes

• SB 2063 (P.A. 97-0463)(Signed 8/19/2011)

• Prepaid Wireless Surcharge

• Creates a prepaid wireless 911 surcharge of 1.5% on retail

transactions of “prepaid wireless telecommunications services”

• “Prepaid wireless telecommunications service” means a wireless

telecommunications service that allows a caller to dial 9-1-1 to

access the 911 system, when the service is paid for in advance and is

sold in predetermined units which decline with use in a known

amount

• Home rule municipalities having a population in excess of 500,000

may impose a prepaid wireless 911 surcharge not to exceed 7% per

retail transaction sourced to that jurisdiction.

• Effective January 1, 2012

20

Proposed 2011 Business Tax Law Changes

Income Tax

• SB 1741 Income Tax-Estimated Taxes (referred to

Assignments 7/23/2011)

• Provides if taxpayer is entitled to refund after payment

of fourth installment, may apply amount of refund to

first installment due in next taxable year

• SB 1900 Brownfield Credit (Re-referred to Rules

Committee 5/31/2011)

• Provides credit against income tax for eligible projects

related to remodeling, rehabilitation, modernization, or

remediation of contaminated property in Illinois

21

Proposed 2011 Business Tax Law Changes

Income Tax

• HB 1084 Business Mandate Note (Referred to

Assignments 7/23/2011)

• Provides that every bill that directly increases cost of

doing business in State shall have brief explanatory

statement or note with reliable estimate of anticipated

impact before second reading

22

Proposed 2011 Business Tax Law Changes

Income Tax

• SB 163 and SB 1842– Extends R&D Credit to 1/1/2016

and increases amount from 6.5% to 8% (Referred to

Assignments 3/18/2011)

• SB 1215 –Extends R&D Credit until 12/31/2016 (Referred

to Assignments 3/18/2011

• HB 2948—Extends R&D Credit until 12/31/2011 plus 5year Carryforward (Referred to House Rules 3/17/2011)

23

Proposed 2011 Business Tax Law Changes

Sales Tax

• SB 2194 Sales Tax Sourcing (Re-referred to Rules Committee 5/31/

2011)

• Attempts to codify history of regulations and letter rulings issued

by the Department concerning location of where order acceptance

occurs for Illinois Retailers’ Occupation Tax

• Amended to provide that if order is first received by the retailer or

placed by purchaser at a retailer’s retail sales location and

immediate payment and delivery or shipment of property occurs

at that location, retail sales location deemed the sales location for

the sale

• SB 397 w/HA#1—RTA/IDOR Local Sales Tax Sourcing Proposal

(Re-referred to Rules Committee 5/31/2011)

24

Proposed 2011 Business Tax Law Changes

Property Tax

• HB 363 (Re-referred to Rules Committee 7/23/ 2011)

• PTELL Referendum Transparency

• HB 503 (Senate Assignments 4/22/2011)

• Municipal Lease of Exempt Property

• HB 1883 (Senate Assignments 7/23/2011)

• Stipulated Assessments

• SB 19 (Re-referred to Rules Committee 5/31/2011)

• Annual Reapplication for Senior Citizens Homestead Exemption

in Cook County

• SB 1648 (Re-referred to Rules Committee 5/31/2011)

• Homestead Assessment Freeze Expansion of Disabled

25

Judicial Developments

Income Tax

AT&T Teleholdings Inc. v. Department of Revenue, 09COEL-008 (Cir. Ct. Cook County 1/20/2011)

In a Memorandum Opinion and Judgment Order, the

Circuit Court affirmed the decision of an Administrative

Law Judge that held a capital loss should be allocated

among members reporting a capital loss on Schedule D in

proportion to the sum of all separate capital losses so as

not to result in a windfall by carrying back the loss using a

combined apportionment method.

26

Judicial Developments

Non-Income Tax

Cwik v. Giannoulias, Ill., No. 108313, 5/20/2010

Issue: Whether the state’s retention of interest accrued on unclaimed

property pursuant to § 15 of the Act is an unconstitutional taking of

private property without compensation.

Holding: The Illinois Supreme Court held that the state’s unclaimed

property statute divests the owner of abandoned property of certain

incidents of ownership while that state provides safekeeping of the

property along with reclamation services. This limited lapse or

divestment is not an illegal taking for which compensation is due.

27

Judicial Developments

Non-Income Tax

Hartney Fuel Oil Co. v. Department of Revenue, Tenth

Circuit Court of Illinois, No. 08-MR-11, 08-MR-13, 08MR15, 1/26/2011

Issue: Whether fuel company provided sufficient evidence to support

its position that its fuel sales transactions were sitused at its sales office

in the Village of Mark.

Holding: Illinois Circuit Court held that the evidence was sufficient

and therefore the local sales tax imposed in Forest View should not

have been collected by the Illinois Department of Revenue.

28

Judicial Developments

Non-Income Tax

Empress Casino Joliet Corp. v. Blagojevich, No. 09-3975,

638 F. 3d 519 (3/2/2011)

Issue: Whether casino surcharge imposed by the Illinois legislature

and used by the state to assist the horse racing industry is a “tax” to

which the federal Tax Injunction Act applies.

Holding: The U.S. Court of Appeals for the Seventh Circuit held the

casino surcharge was not a “tax,” but rather more like a regulatory

penalty or fee.

29

Judicial Developments

Non-Income Tax

Performance Marketing Association v. Brian Hamer,

Director, Illinois Department of Revenue, Cir. Ct. Cook

County, 7/27/2011

Complaint originally field in Federal Court, dropped and refiled in Cir.

Ct. Cook County challenging the constitutionality of HB 3659 (P.A.

96-1544)(click-through nexus provisions)

• Count 1 alleges improper and unduly burdensome regulation of

interstate commerce in violation of the Commerce Clause of the

US Constitution

• Count 2 alleges improper regulation of commerce occurring

outside of Illinois’ borders in violation of the Commerce Clause

• Count 3 alleges violation of the Federal Internet Tax Freedom Act

30

Judicial Developments

Non-Income Tax

Interstate Trucks, LLC v. State of Illinois, Ill. App. Ct., 4th

Dist. No. 4-10-0603 (6/14/2011)

Motor Fuel Tax Law

Issue: Whether out-of-state dealership that purchased trucks in Illinois and

then attempted to transport the trucks to the dealership in Tennessee was

subject to the motor fuel use tax when fuel for the trucks was purchased in

Illinois.

Holding: Court held that motor fuel use tax license was not required because,

at the time the Department stopped the trucks, they had been operated

exclusively within Illinois, and fuel sufficient to get the trucks out of the state

had been purchased in Illinois. The court further found that requiring the

taxpayer to purchase single-trip permits would not further the purpose behind

the motor fuel use tax.

31

Judicial Developments

Non-Income Tax

Wirtz v. Quinn, Ill. S. Ct., 2011 IL 111903 (7/11/2011),

reversing Wirtz v. Quinn, Ill. App. Ct., No 1-09-3163 and 1-10-0344

(1/26/2011)

Issue: Whether four laws enacted in 2009 that created a $31 billion capital

program were enacted in violation of the single subject rule of the Illinois state

constitution.

Holding: On appeal, the Illinois Supreme Court reversed the Court of

Appeals, finding that the substantive provisions of the Act were clearly

connected to the single subject of the Act (capital projects) because they

established increased revenue sources to be deposited into the Capital Projects

fund. Even the provisions that did not directly raise revenue were still related

in that they helped implement the other provisions. The Court rejected all

other constitutional challenges to the enactment of the Act.

32

Judicial Developments

Non-Income Tax

Kansas City Southern Railway Co. et al. v. Koeller et al.,

7th Cir., No. 10-2333 (7/27/2011)

Federal Railroad Revitalization and Regulatory Reform Act (“4-R

Act”)

Issue: Whether Sny Island Levee Drainage District assessments were

discriminatory under the federal 4-R Act.

Holding: 7th Circuit decision found that the assessment did violate the 4-R

Act’s prohibition against imposition of discriminatory taxes when it changed

its method for calculating assessments due under the Illinois Drainage Code.

While the basis for calculating the assessments (a “benefit basis”) might have

been fair in theory, as applied to the railroad companies, it was discriminatory

in practice. Case remanded to district court with instructions to enjoin the

assessments.

33

Judicial Developments

Non-Income Tax

Demos v. Pappas et al., Ill. App. Ct., 1st Dist. No. 1-100829 (8/15/2011)

Issue: Whether County Treasurer, as judgment debtor under the Property

Tax Code Indemnity Fund, is a “governmental entity” for purposes of

calculating postjudgment rates.

Holding: The Property Tax Code Indemnity Fund is maintained to satisfy

judgments against the County Treasurer, as trustee of the fund. The interest

rate applicable to such judgments depends on whether the “judgment debtor”

is a “governmental entity.” As trustee of the Fund, the Cook County Treasurer

is the relevant “judgment debtor,” and the Court of Appeals determined that

the county treasurer is a “governmental entity,” because the treasurer is a

constitutional officer carrying out her public duties for the benefit of the public.

Therefore, the proper postjudgment rate on indemnity fund judgments is 6%.

34

Judicial Developments

Non-Income Tax

Regional Transportation Authority v. City of Kankakee et.

al., Cir. Ct. Cook County (8/23/2011)

Complaint filed August 23, 2011 alleging that Kankakee and

Channahon have been distributing local sales tax revenue to companies

sourcing sales to “sham” offices purportedly located in those

municipalities. The RTA claims that these “sham” offices are set up to

avoid paying locally imposed taxes, including the share of the

Retailers’ Occupation Tax that is allocated 0.25% to the RTA in Cook

County. As a result, the RTA “loses sales tax monies that should have

been rightfully paid to it.” The complaint alleges a violation of 65

ILCS 5/8-11-21, and seeks damages to compensate for the tax revenue

it was denied as a result of the municipalities unlawful conduct.

35

Judicial Developments

Non-Income Tax

City of Chicago v. City of Kankakee et. al., Cir. Ct. Cook

County (8/23/2011)

Similar to the RTA action, but limited to periods since 1/1/2004

forward. In addition to damages, City of Chicago is seeking injunctive

relief.

36

Income Tax

Adopted Regulations

Income Tax

• Estimated Income Tax Payment

• 86 Ill. Adm. Code 100.8000 and 100.8010, added 8/19/10

• Taxability in Other State

• 86 Ill. Adm. Code 100.3200, amended 8/19/10

• Filing Extension Pass-through Entities

• 86 Ill. Adm. Code 100.5020, amended 8/19/10

• Income Tax Treatment of Separate Entities

• 86 Ill. Adm. Code 100.9750, amended 8/19/10

37

Income Tax

Adopted Regulations

Income Tax (con’t)

• Electronic Filing Returns and Other Documents

• 86 Ill. Adm. Code 760.100, amended 12/21/10 (see slide re:

proposed regs for Notice of further amendments)

• Refund Claims for Overpayment

• 86 Ill. Adm. Code 100.9400 and 100.9410, amended 2/25/11.

• Angel Investor Tax Credit

• 14 Ill Adm. Code 531.10-.90, adopted 6/1/11

38

Sales/Other Tax

Adopted Regulations

Sales Tax

• Retailers’ Occupation Tax/Graphic Arts Machinery

• 86 Ill. Adm. Code 130.325, amended 1/24/11

• Retailers’ Occupation Tax Candy, Soft Drinks, Drugs, Medicines,

Medical Appliances and Grooming and Hygiene Products as the result

of P.A. 96-0034 and 96-0038

• 86 Ill. Adm. Code 130.310, amended 8/19/10, and 130.311, added

8/19/10

All Taxes Administered by the DOR

• Tax Amnesty

• 86 Ill. Adm. Code 520.101 and 105

39

Department of Revenue

Proposed Income Tax Regulations

• Electronic Filing of Returns and Other Documents;

Proposal to amend 86 Ill. Adm. Code 760.100

• Would mandate filing of Illinois corporate income tax

return electronically for those corporations required to

file their federal income tax returns, beginning with

returns for taxable years ending December 31, 2011

• Formal JCAR meeting 9 /13/2011; 2d Notice ends

10/5/2011

40

Department of Revenue

Proposed Income Tax Regulations

• Income Tax; Notice of Proposal to amend 86 Ill. Adm. Code 100.7325

(5/27/2011)

• Would amend regulation to require semi-weekly withholding payments to

be made by electronic funds transfer beginning calendar year 2011

• Income Tax; Notice of Proposal to amend 86 Ill. Adm. Code 100.2101

(6/3/2011)

• Would update regulation to reflect changes to the definition of “retailing”

and “tangible personal property” under PA 96-115, and extend the

replacement tax investment credit through 2013

• Income Tax; Notice of Proposal to add 86 Ill. Adm. Code 100.2193,

.2435, and .2510 (6/10/2011)

• Proposes new rules regarding: subtraction modification for contributions

to an Il qualified tuition plan; income tax credit for contributing

employers; and addition modification for employers claiming the credit

41

Department of Revenue

2011 Regulatory Agenda/ Projects

Income Tax (no hearings scheduled as of 8/29/2011)

• 86 Ill Adm. Code 100 (multiple sections)

• Add new rules concerning: tax credit for Tech Prep Youth Vocational

Programs; reallocation of items under Section 404; pass-through of

investment credits from partnerships and Sub S corps; filing of refund

claims, statutes of limitations and interest computations

• Add and amend rules concerning: computation of base income under Art 2

and the allocation and apportionment of base income under Art 3;

definition of unitary business group and computation of combined tax

liability of unitary group; addition and subtraction modifications for

residential property tax credit; definitions in Section 1501(a);

implementation of legislation introduced beginning in 2004; and guidance

on nexus and Illinois tax consequences of Federal tax law changes

42

Department of Revenue

2011 Regulatory Agenda/ Projects

Sales/Use Taxes (no hearings scheduled as of 8/29/2011)

•

ROT, 86 Ill. Adm. Code 130: Project relates to multiple sections, including:

•

•

•

•

•

•

•

130.415 transportation and delivery charges

130.2050 sales and gifts by employers to employees

130.450 installation, alteration, and special service charges re: real estate

130.340 rolling stock exemption

SOT, 86 Ill. Adm. Code 140: Project relates to general updates designed to

clarify application of the SOT and to reflect recent decisional law, statutory

changes and Dept. policies

Use Tax, 86 Ill. Adm. Code 150: Project relates to updates designed to reflect

new statutory developments, decisional law, and Dept. policies regarding, for

example, the types of activities and relationships that establish nexus for Use

Tax purposes

Service Use Tax, 86 Ill. Adm. Code 160: Project designed to reflect new

statutory developments, decisional law and Dept. policies

43

Illinois Department of Revenue Developments

New Tax Computer System

• Department in process of completing project to consolidate

more than 200 tax and fee programs into one integrated

computer system (four year project begun in 2007)

• Department will have ability to view taxpayer accounts on

consolidated basis

• Enhancements to notices and bills (include Account ID for

each tax type; Taxpayer Statement to replace Statement of

Account)

• Illinois Business Tax (IBT) numbers to be replaced by

Account IDs

44

Illinois Department of Revenue Developments

Denial of Property Tax Exemption

• On August 16, 2011, based on the 2010 Illinois Supreme

Court decision in Provena Covenant, the Department

denied the exempt status of three more Illinois hospitals.

The reported charity care at the hospitals ranged from

1.85% of patient revenue to .96%, all in excess of the .07%

determined by the court in Provena to be “de minimis.”

The hospitals can seek review of the Department’s

decision by filing a petition with the Office of

Administrative Hearing within 60 days of the

Department’s decision.

45

Other Income Tax Developments

Electronic Filing

• Effective January 1, 2011, paid preparers who file more than 100

Illinois Individual Income Tax returns must file electronically

Electronic Payments

• Effective October 1, 2010, the mandated threshold for electronic

payments reduced from $200,000 to $20,000 except for Individual

Income Tax, Telecom Tax, Environmental Impact Fee, and Motor Fuel

Tax

• Effective January 1, 2011, the mandated threshold for making

electronic payments for Withholding Income Tax reduced to $12,000

Bonus Depreciation

• Department issued revised Form IL-4562

• Provides clarification that Illinois conforms with 100 percent bonus

depreciation allowed under Tax Relief, Unemployment Insurance

Reauthorization, and Job Creation Act of 2010

46

Franchise Tax—Illinois Secretary of State

Recent Activity

• BCA 1.35 Allocation Factor Interrogatories—Proposed Apportionment

Factor changes

• Business Services Section amended instructions to Interrogatories

related to the sourcing of “investment property” and service

income

• Significant impact on Illinois Headquarters Companies

• Secretary of State withdrew revised Form BCA 1.35 and reinstated old

Form (revised as of Jan. 2003)

47

Q&A

•

•

•

This document is for general information purposes only, and should not be used as

a substitute for consultation with professional advisors .

This document was not intended or written to be used, and it cannot be used, for the

purpose of avoiding U.S. federal, state or local tax penalties.

© 2011 PwC. All rights reserved. In this document, "PwC" refers to

PricewaterhouseCoopers LLP, a Delaware limited liability partnership, which is a

member firm of PricewaterhouseCoopers International Limited, each member firm of

which is a separate legal entity.