Read full five year economic forecast

advertisement

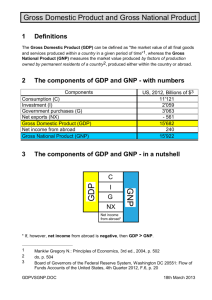

Irelands Economic outlook David Duffy The Outlook Dependent on world trade growth Household spending likely to remain weak, but some improvement due to employment growth If forecast recovery materialises then Irish growth will improve in 2014 Savings rate to remain around current levels Investment to increase (FDI and a number of big projects) Export growth continues to increase, mainly due to services Although unemployment will fall it remains high Public finances to improve again GDP to increase by 1.8 per cent in 2013 and 2.7 per cent in 2014 The International Economy Euro Area United States United Kingdom 4 4 4 3 3 2 2 1 1 0 0 -1 -1 -2 -2 -3 -3 -4 -4 -4 -5 -5 -5 3 2 1 0 -1 -2 -3 Actual outturn Forecast range Actual outturn and median of forecasts Sources: Eurostat, FocusEconomics, IMF, OECD, HM Treasury and Federal Reserve International forecasts, GDP growth 4.5 4 Annual % change 3.5 3 World 2013 2.5 World 2014 2 US 2013 1.5 US 2014 Eurozone 2013 1 Eurozone 2014 0.5 UK 2013 0 UK 2014 -0.5 -1 Jan 2012 Apr 2012 July 2012 Oct 2012 Jan 2013 Apr 2013 Economic Outlook 2011 2012 2013(f) 2014(f) Consumption -2.4 -0.9 -0.4 0.4 Government -4.3 -3.7 -1.0 -2.0 Investment -12.6 1.2 1.6 5.5 Exports 5.1 2.9 3.0 5.3 Imports -0.3 0.3 2.3 4.3 Economic Outlook 2012 2013(f) 2014(f) 0.9 1.8 2.7 14.7 14.2 13.9 1.7 1.5 1.7 Budget Deficit (GGB) (% GDP) -7.6 -7.2 -4.6 GNP (% change) 3.4 1.0 1.5 Domestic demand (% change) -1.5 0.7 0.7 GDP (% change) Unemployment (%) CPI (% change) GDP, % Change, Volume 14 Celtic Tiger period 12 Domestic Driven Growth +11.5% Recession.......and recovery 10 Per cent change 8 6 ESRI Forecasts 2013-2014 4 2 0 -2 1989 1994 1999 2004 2009 -4 -6 -8 -5.5% 2014 Emigration reducing unemployment Level of employment and unemployment falling Long-term unemployment fell 19,700 in Q4 2012 Employment still falling in 2012 000s 80 60 40 20 0 -20 -40 Excluding agriculture, annual decrease of 10,600 in Q4 2012 Long-term Unemployment, Annual Change Total Males Females Contribution to GDP Growth 8 6 4 2 0 -2 2008 2009 2010 2011 2012 2013 -4 -6 -8 -10 -12 Total Domestic Demand (incl. stocks) Net Exports 2014 Contribution to GDP Growth 8 6 4 2 0 -2 -4 -6 -8 -10 -12 2009 2010 Consumption 2011 Government 2012 Investment 2013 2014 Net exports Redomiciled plcs, Irish output and the balance of payments A number of companies have relocated HQ to Ireland without generating real activity (redomiciled plcs) Inflow of profits, only some of which is paid out in dividends Recorded inflows are much higher than recorded outflows Impact on measured BoP current account surplus and nominal GNP Redomiciled plcs, Irish output and the balance of payments GNP, € millions 150000 Current Account, % of GNP 8.0 6.0 140000 4.0 130000 120000 2.0 110000 0.0 100000 90000 -2.0 80000 -4.0 70000 60000 -6.0 GNP - Adjusted 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 GNP -Published -8.0 Unadjusted Adjusted Redomiciled plcs and output 6 4 2 0 -2 -4 -6 -8 -10 2009 2010 2011 2012 GNP GNP adjusted Medium Term Outlook Backdrop of high debt levels Two different paths Recovery scenario – virtuous circle Failure to fix banks? Realising state’s financial assets Failure to provide credit to fund recovery Low growth scenario – vicious circle? Cause is external to Ireland What can policy do? Recovery Stronger growth from 2015 Unemployment rate declines Government surplus 2018 Neutral fiscal policy 2016-20 Further benefits – realise financial assets Reduce net debt GDP ratio below 60%? Issues: Banks, labour market Low Growth Unemployment rate remains high Government Deficit Banks may well cost more money Net Debt GDP ratio 2020 same as today Any shock or additional problems More austerity 2016-20? Possible downward spiral Policy response? Assessment When account taken of redomiciled plc profit flows economic performance weaker than estimated Balance of payments surplus smaller – less potential impact on growth Domestic issues Availability of credit Business and Consumer Confidence Unemployment (especially LTU) Assessment External sector, particularly services exports, main driver of growth in 2012 and over forecast period Forecasts of upturn in international economy important Domestic economy remains weak but should start to make contribution to growth from 2013 and 2014 Investment growth, small upturn in PCE in 2014 Unemployment rate will only fall gradually Initially due to net emigration Public finances set to meet targets Continue with planned consolidation measures