Slide 1 - Dairy Crest

advertisement

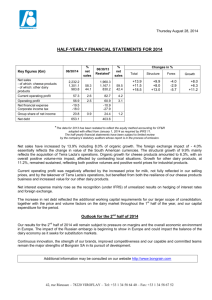

DAIRY CREST GROUP PLC PRELIMINARY RESULTS For the year ended 31 March 2006 1 Highlights Building value through brand development • Group Revenue (including share of jvs) £1.42bn (2005: £1.35bn) • Adjusted profit before tax* £67.7m (2005: £75.7m) • Adjusted earnings per share* 40.3 pence (2005: 43.9 pence) • Full year dividend up 6.4% to 21.5 pence (2005: 20.2 pence) • Net debt £280.2m (2005: £227.5m) * Including share of joint ventures and before exceptional items and amortisation of acquired intangibles 2 Highlights Building value through brand development • We continue to make good progress with our brand portfolio: - strong performances from Cathedral City, Clover, Country Life Spreadable and the Yoplait brands - active programme of new product launches with emphasis on functional foods - recent launch of Cathedral City Mild • We have strengthened the Dairies division: - integration of Midlands Co-op Dairies and Foston completed on time and to plan - successful implementation of additional Morrisons fresh milk - better balance of industry supply and demand in fresh milk - good performance by household business 3 Financial Review Alastair Murray 4 Income Statement £’m Year March 06 Year March 05 82.0 91.9 (14.3) (16.2) 67.7 75.7 Exceptional items (22.2) (4.4) Intangible amortisation (1.0) - Profit before tax 44.5 71.3 Taxation (9.7) (19.7) Profit after tax 34.8 51.6 Profit on operations** Net finance costs Profit after interest** * All items include share of joint ventures ** Before exceptional items and amortisation of acquired intangibles 5 Exceptional Items £’m Year March 06 Cash Non Cash Total Midlands Co-op Dairies (11.7) (1.0) (12.7) Arla London Foodservice (2.6) - (2.6) 1.4 - 1.4 - (9.3) (9.3) (12.9) (10.3) (23.2) 1.0 - 1.0 (11.9) (10.3) (22.2) Sale of Newport IOW Dairy Impairment of assets Share of JV sale of Enfield* Total * Profit on sale before tax 6 Earnings and Dividends Pence per share Year March 06 Year March 05 Change % Adjusted EPS 40.3 43.9 - 8.2 Basic EPS 27.1 41.4 - 34.5 Dividend declared 21.5 20.2 + 6.4 Shares in issue: m 124.8 123.4 7 Segmental Analysis £’m Year March 06 Year March 05 Foods excl jvs 539 518 Joint ventures 69 88 Foods 608 606 Dairies 816 743 1,424 1,349 Foods excl jvs 54.9 49.2 Joint ventures 9.3 7.5 Foods 64.2 56.7 Dairies 16.8 35.2 Total 81.0 91.9 Revenue Total Profit on operations * * Including pre tax and interest share of jvs and before exceptional items 8 Operating Margin* % Year March 06 Year March 05 Foods excl jvs 10.2 9.5 Joint ventures 13.5 8.5 Foods 10.6 9.4 Dairies 2.1 4.7 Total 5.7 6.8 * Including share of joint ventures and before exceptional items 9 Balance Sheet £’m Year March 06 Year March 05 Net operating assets 558.6 466.4 Tax (20.4) (18.3) 538.2 448.1 (280.2) (227.5) Net assets employed 258.0 220.6 Gearing 109% 103% Net debt 10 Operating Cash Flow £’m Year March 06 Year March 05 Adjusted profit on operations* 81.0 91.9 Depreciation and amortisation** 38.6 33.1 Exceptional items (14.3) (1.3) Pensions (1.3) 7.4 Joint ventures and other (14.3) (10.5) Working capital (16.3) 22.4 73.4 143.0 Operating cash flow * Including share of joint ventures and before exceptional items ** Net of grants 11 Cash Flow £’m Year March 06 Year March 05 73.4 143.0 Capital expenditure (net of grants) (44.0) (37.7) Interest, tax and dividends (57.5) (54.2) Dividends received from jvs 9.0 - (43.7) (9.9) Disposals 9.4 8.4 Other 0.7 2.6 Movement in net debt (52.7) 52.2 Net debt at 31 March 2005 227.5 Net debt at 31 March 2006 280.2 Operating cash flow Acquisitions 12 Pensions Summary • IAS19 gross deficit at 31 March 2006 of £62.0m (2005:£102.7m) - highly volatile measure - increased asset valuations and discount rate • Scheme to close to new entrants from July 2006 • Additional cash contribution of £6.0m in 2005/06 • Employer contributions to increase by £11.0m to c.£28.3m from 2006/07 - additional cash contribution of £12.0m - basic contribution increased from £11.3m to c.£16.3m • Committed to maintain additional cash contribution of £12.0m in 2007/08 • Next full actuarial valuation as at 31 March 2007 13 Business Review Drummond Hall 14 Total Shareholder Return since IPO • TSR = Share price + dividends 600.0 500.0 400.0 300.0 200.0 100.0 0.0 Aug-96 Aug-97 Aug-98 Aug-99 Aug-00 Aug-01 Aug-02 Aug-03 Aug-04 Aug-05 Dairy Crest (TSR) Source: Datastream (May 2006) FTSE 250 (TSR) 15 Our brands are getting bigger + 248% 1996/97 Cathedral City 2005/06 1996/97 + 36% Clover 2005/06 0 100 200 300 400 1996/97 + 210% Petits Filous 2005/06 1996/97 Country Life 2005/06 0 100 200 300 + 317% 400 Source: Dairy Crest Annual Sales Volumes (Country Life 100% since Sept 2004) – 1996/97 indexed to 100 16 Our brands are getting bigger £106m bigger than £66m bigger than £52m bigger than £41m bigger than Source: TNS / AC Nielsen / IRI 52 week ended March 2006 17 We’ve been active with new product development 18 Spreads • Spreads business continues to be biggest profit contributor • Marketing continues to focus on four key brands - simplified portfolio with fewer brands and sku’s • Good performance from Clover - sales value growth of 5% - lower proportion of sales on promotion - price increases achieved in Sept 2005 and Jan 2006 • Utterly Butterly continues to make progress against competition - increased share of dairy spreads sector - sales up 7% by volume and down 2% by value 19 Clover and UB outperform ICBINB DC acquired UB MAT Value: £000’s 70,000 65,000 60,000 55,000 50,000 45,000 40,000 35,000 30,000 Clover Source: AC Nielsen (MAT) 26 March 2006 ICBINB 06 ar - 5 M ec -0 D Ju l-0 5 O ct -0 5 05 pr A Ju n03 Se p03 N ov -0 3 Fe b04 M ay -0 4 A ug -0 4 N ov -0 4 Ja n05 03 M ar - 2 ec -0 D Ju l-0 2 O ct -0 2 Ja n02 A pr -0 2 25,000 Utterly Butterly 20 Country Life • Good growth in Country Life - packet sales up 9% by value - spreadable sales up 23% by value • Successful marketing campaign launched in summer 2005 - first national TV advertising for 20 years • Lightly salted version of Country Life Spreadable launched in January 2006 • New packaging for Country Life range introduced • Opportunities to stretch the Country Life brand into new areas 21 St. Ivel Gold • St. Ivel Gold volume and share under pressure - sales down 17% by value - strong competitor performance • St. Ivel Gold relaunched in January 2006 - new packaging - new television advertising campaign - new Omega-3 variant launched • St. Ivel Gold will be the platform for functional spreads 22 Cathedral City • Strong performance from Cathedral City - sales up 17% by value and 11% by volume - lower proportion of sales on promotion • New packaging launched • Successful TV advertising campaign • Cathedral City Mild launched May 2006 • Final phase of Davidstow redevelopment completed 23 ay -0 Au 1 gN 01 ov -0 Ja 1 n0 Ap 2 r-0 Ju 2 lSe 02 pD 02 ec -0 Fe 2 bM 03 ay -0 Au 3 g0 O 3 ct -0 Ja 3 n0 Ap 4 r-0 Ju 4 nSe 04 pN 04 ov Fe 0 4 bM 05 ay -0 Ju 5 l-0 O 5 ct -0 Ja 5 n0 M 6 ar -0 6 M Cathedral City Growth £120m £100m £80m £60m £40m £20m £0m Cathedral City Source: TNS (MAT) 26 March 2006 Seriously Strong Pilgrims Choice 24 Cheese • Strong overall performance from our cheese business - Cathedral City growth - cost related price increases achieved in summer 2005 • Davidstow brand performed strongly with sales up 19% • Successful implementation of new own label supply arrangements with ASDA and Morrisons • Stilton business continues to be challenging - impairment charge on value of assets of £9.3m - launch of new speciality cheese brand ‘Over the Moon’ • Strong market for whey products • Industry cheese stocks have risen in second half - pressure on pricing in commodity cheese in 2006/07 25 De c01 M ar -0 Ju 2 n0 Se 2 p0 De 2 c02 M ar -0 3 Ju n0 Se 3 p0 De 3 c03 M ar -0 4 Ju n0 Se 4 p0 De 4 c04 M ar -0 Ju 5 n0 Se 5 p0 De 5 c05 M ar -0 6 Cheese Stocks K tonnes British Cheese Board cheddar stocks 12 month moving average 115.0 110.0 105.0 100.0 95.0 90.0 85.0 26 Yoplait Dairy Crest • Continued good growth in chilled yogurts and desserts market • Brands continue to perform strongly with overall sales value up 11% - Petits Filous up 25% - Frubes up 34% - Wildlife up 6% - YOP up 13% • Weight Watchers down 4% by value but held market share in ‘Light’ • New product development in functional foods - Petits Filous Plus: probiotic yogurt drink for kids • Closure of own label operations in June 2005 27 Liquid Products • Retail milk volumes down 17% year on year - Tesco volume ceased in April 2005 • Morrisons additional volume successfully implemented at end of October 2005 • Acquisitions of Midland Co-op Dairies and Foston dairy in May 2005 - integration completed on schedule and to plan - MCD Birmingham dairy closed February 2006 - Foston now fully operational • Better balance of supply and demand in fresh milk industry • Price increases achieved from March 2005 and further increases achieved in January 2006 to offset higher input costs 28 Other Liquid Products • Strong growth in organic milk - own label milk sales up 49% by value - Rachel’s brand sales up 47% by value • FRijj maintained market leading position - value down 5% due to lower promotional volumes - addressing capacity constraints for 2006/07 • Potted cream sales up 15% by value - M&S sole supply position from August 2006 • St. Ivel advance encouraging performance so far - good levels of trade distribution - annualised retail sales of approximately £13m 29 Household • Overall household volumes up 31% year on year - volume gained in middle ground - Midlands Co-op Dairies acquisition May 2005 - Arla’s London foodservice business October 2005 - ongoing infill acquisitions • Uplift in Midlands Co-op performance - Average milk per round: 322 to 450 gallons pw - Non-milk products per round: £55 to £206 pw • Underlying doorstep decline maintained at around 8% - investment in canvassing - first class service initiatives • Non-milk product sales up by 30% • Doorstep price increase from September 2005 of 2 pence per pint 30 Milk Procurement • Strong working relationship with Dairy Crest Direct - over 70% of raw milk sourced from Dairy Crest Direct • Dairy Crest continues to pay market leading prices - Waitrose and Marks & Spencer - Davidstow • Price reductions on cheese contracts following 0.8 ppl increase in summer 2005: - 0.5ppl from March 2006 (excluding Davidstow) - Announced 0.5ppl from June 2006 (0.25ppl for Davidstow) • Price reduction on liquids contracts of 0.5ppl from April 2006 reflecting lower commodity cream prices 31 Outlook • Our brand portfolio continues to make good progress - further new product launches • Markets for own label and commodity products continue to be challenging • Improved performance from Dairies division • Trading at the start of the new financial year is on track 32 DAIRY CREST GROUP PLC PRELIMINARY RESULTS For the year ended 31 March 2006 33