Managerial Accounting Chapter 38

advertisement

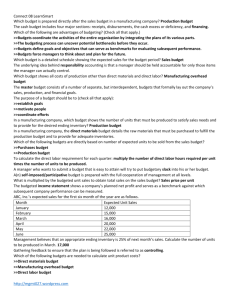

Chapter 38 Managerial Accounting Sales, Production, and Purchases Budgets Prepared by Diane Tanner University of North Florida Master Budget 2 A comprehensive planning document Incorporates a number of individual budgets Replaced by an ‘inventory purchases’ budget for merchandising companies, or by ‘cost of services’ budget for service companies Sales budget Production budget Materials purchases budget Direct labor budget Manufacturing overhead budget Selling and administrative budget Capital acquisitions budget Budgeted statement of cash flows Cash budget Budgeted income statement Budgeted balance sheet The Flow of Budgets in the Master Budget Sales Budget Materials Purchases Budget Production Budget Selling and Administrative Budget Direct Labor Budget Manufacturing Overhead Budget Cash Budget Budgeted Financial Statements 3 4 Sales Budget First step in the budget process Why? Subsequent budgets cannot be prepared without an estimate of sales Involves forecasting sales Based on various methods including Econometric models Previous sales trends Trade journals and magazines Sales force estimates Sales Budget Example DartCo’s selling price is $10 per bucket for April with a 5% increase per month thereafter. Budgeted sales for the next five months are: April 3,200 units May 4,000 units Then 10% increase per month thereafter Budgeted sales (units) Selling price per unit Total sales April May June 3,200 4,000 4,400 $10.00 $10.50 $11.03 $32,000 $42,000 $48,510 While this budget covers 3 months, management often prepares annual, quarterly, and monthly budgets 5 Production Budget The only budget in the master budget that is prepared in ‘units’ Budgeted sales of finished units + Desired ending inventory of finished units − Beginning inventory of finished units = Finished goods units to be produced Sales Budget Production Budget 6 7 Production Budget Example Trump Inc. produces trinkets. Each trinket requires 0.4 board feet of wood and 1.25 hours of direct labor. Wood costs $1.40 per board foot. Trump desires to have 20% of the materials needed for production during the next month on hand at the end of each month, and 15% of the number of trinkets to be sold the next month on hand at the end of each month. Scheduled sales of trinkets for April are 4,200, May is 4,500, and June is 5,200 units. Prepare a production budget for May. Begin with units to be sold Trinkets to be sold Add ending FG inventory desired: 15% x 5,200 Ending FG inventory desired Subtract beginning FG inventory desired: 15% x 4,500 Add the ending and subtract beginning inventories 4,500 780 Beginning FG inventory to be on hand (675) Budgeted trinkets to be produced 4,605 8 Direct Materials Purchases Budget Step 1: Begin with units to be sold Step 2: Convert to the RM denomination, i.e., in what quantities are materials purchased from suppliers Such as…pounds, yards, kilograms, linear feet Step 3: Multiply to determine the quantity needed for production Step 4: Add desired ending RM inventory Step 5: Subtract expected beginning RM inventory Step 6: Multiply the materials quantity to be purchased times the cost per unit of material 9 Materials Purchases Budget Format Budgeted finished units to be produced x Raw materials needed for each finished goods unit = Total raw materials units needed for production + Desired raw materials ending inventory − Beginning raw materials on hand = Raw materials needed to purchase x Cost per raw materials unit = Budgeted cost of purchases Denominated in ‘units’ in which the raw materials are inventoried. 10 Materials Purchases Budget Example Trump Inc. produces trinkets. Each trinket requires 0.4 board feet of wood, costing $1.40 per board foot. Trump desires to have 20% of the materials needed for production during the next month on hand at the end of each month, and 15% of the number of trinkets to be sold the next month on hand at the end of each month. Scheduled production of trinkets for May is 4,605 and June is 5,100 units. Prepare a materials purchases budget for May. Begin with FG units to be produced Trinkets to be produced 4,605 Convert to RM denomination Wood (board feet) required for each trinket Multiply to get total needed for production Board feet of wood needed for production Add ending RM inventory desired: 20% x 5,100 x 0.4 feet Ending RM inventory desired Subtract beginning RM inventory desired: 20% x 4,605 x 0.4 feet Beginning FG inventory to be on hand 0.40 1,842 408 Continued (368) Materials Purchases Budget Example Each trinket requires 0.4 board feet of wood, costing $1.40 per board foot. Trump desires to have 20% of the materials needed for production during the next month on hand at the end of each month, and 15% of the number of trinkets to be sold the next month on hand at the end of each month. Scheduled production of trinkets for May is 4,605 and June is 5,100 units. Prepare a materials purchases budget for May. Add the ending and subtract beginning inventories Budgeted board feet to purchase Indicate the cost per RM denomination Cost per board foot $ 1.40 Multiply to determine the cost of materials purchases Budgeted cost of materials purchases $9,082 6,487 11 Hints Must clearly distinguish between the two types of inventory in budgets Companies produce and sell finished goods So…. Sales budget uses only units to be sold The production budget determines finished units to be produced Materials purchases budget units are denominated in raw materials units; it ultimately determines the raw materials units to be purchased 12 The End 13