Managerial Accounting Concepts

and Principles

Chapter 14

PowerPoint Editor:

Beth Kane, MBA, CPA

Wild, Shaw, and Chiappetta

Financial & Managerial Accounting

6th Edition

Copyright © 2016 McGraw-Hill Education. All rights reserved. No

reproduction or distribution without the prior written consent of

McGraw-Hill Education.

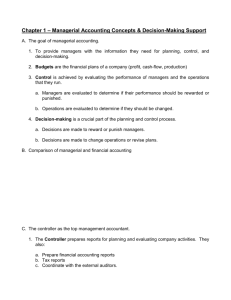

14-C1: Purpose of Managerial

Accounting

2

18 - 3

Managerial Accounting Basics

Managerial accounting

provides financial and

nonfinancial information

for managers of an

organization and other

decision makers.

C1

3

18 - 4

Purpose of Managerial Accounting

C1

4

18 - 5

Nature of Managerial Accounting

C1

5

18 - 6

Fraud and Ethics in

Managerial Accounting

Fraud affects all business and it is costly: A 2014 Report to

the Nation from the Association of Certified Fraud

Examiners (ACFE) estimates the average U.S. business

loses 5% of its annual revenues to fraud.

The Institute of Management Accountants has issued a code of

ethics to help accountants involved in solving ethical dilemmas.

C1

6

14-C2: Cost Classifications

7

18 - 8

Types of Cost Classifications

Classification by Behavior

Cost

Cost behavior refers to how a

cost will react to changes in

the level of business activity.

• Total fixed costs do

not change when activity

changes.

Cost

Activity

Activity

C2

• Total variable costs change

in proportion

to activity changes.

8

18 - 9

Types of Cost Classifications

Classification by Traceability

Direct costs

Costs traceable to a

single cost object.

Examples: material

and labor cost for a

product.

C2

Indirect costs

Costs that cannot

be traced to a

single cost object.

Example: A

maintenance

expenditure

benefiting two or

more departments.

9

14-C3: Comparing Product

and Period Costs

10

18 - 11

Types of Cost Classifications

Classification by Function

Direct

Labor

Direct

Material

Manufacturing

Overhead

Product

Period costs are expenses not attached to the product.

Selling costs are incurred to

obtain orders and to deliver

finished goods to customers.

C3

Administrative costs are

non-manufacturing costs

of staff support and

administrative functions.

11

18 - 12

Period and Product Costs

in Financial Statements

C3

12

18 - 13

Identifications of

Cost Classifications

C3

13

18 - 14

Cost Concepts for

Service Companies

The cost concepts described are generally

applicable to service organizations.

For example, the cost of

beverages for

passengers of Southwest

Airlines is a variable cost

based on number of

passengers.

C3

14

NEED-TO-KNOW

Following are the costs of a company that manufactures computer chips. Classify each as either a product

cost or a period cost. Then classify each of the product costs as direct material, direct labor, or factory

overhead.

1. Plastic board used to mount the chip

2. Advertising costs

3. Factory maintenance workers’ salaries

4. Real estate taxes paid on the sales office

1. Plastic board used to mount the chip

2. Advertising costs

3. Factory maintenance workers’ salaries

4. Real estate taxes paid on the sales office

5. Real estate taxes paid on the factory

6. Factory supervisor salary

7. Depreciation on factory equipment

8. Assembly worker hourly pay to make chips

Product Costs

All Factory Costs

Assets on Balance Sheet

C2/C 3

5. Real estate taxes paid on the factory

6. Factory supervisor salary

7. Depreciation on factory equipment

8. Assembly worker hourly pay to make chips

Product Costs

Direct

Direct

Factory

Material Labor Overhead

X

Period

Cost

X

X

X

X

X

X

X

Period Costs

Non-Factory Costs

Expensed on Income Statement as

Selling, General and Administrative

15

18 - 16

Manufacturer’s Costs

C3

16

18 - 17

Direct Materials

Direct material costs are the expenditures for

direct materials that are separately and

readily traced through the manufacturing

process to finished goods.

Example:

Steel used in the

frame of a

mountain bike.

C3

17

18 - 18

Direct Labor

Direct labor costs are the wages and salaries for

direct labor that are separately and readily

traced through the manufacturing process to

finished goods.

Example:

Wages paid to a

mountain bike

assembly worker.

C3

18

18 - 19

Factory Overhead

Factory overhead consists of all manufacturing

costs that are not direct materials or direct labor

and the costs cannot be separately or readily

traced to finished goods.

Examples:

Indirect labor – maintenance.

Indirect material – cleaning supplies.

Factory utility costs.

Supervisory costs.

C3

19

18 - 20

Prime and Conversion Costs

Manufacturing costs are often

combined as follows:

Direct

Material

Direct

Labor

Prime

Cost

C3

Manufacturing

Overhead

Conversion

Cost

20

14-C4: Balance Sheet

21

18 - 22

Reporting Manufacturing Activities

Merchandisers . . .

Manufacturers . . .

Buy

finished goods.

Buy

raw materials.

Sell

finished goods.

Produce

and sell

finished goods.

SaleMart

C4

22

18 - 23

Manufacturer’s Balance Sheet

MERCHANDISER

Current Assets

Cash

Receivables

Merchandise

Inventory

MANUFACTURER

Current Assets

Cash

Receivables

Inventories

Raw Materials

Goods in Process

Finished Goods

The primary difference is inventory.

C4

23

18 - 24

Manufacturer’s Balance Sheet

Raw

Materials

Goods in

Process

Finished

Goods

Materials

waiting to be

processed.

Partially complete

products.

Completed

products

for sale.

Can be direct

or indirect.

Material to which

some labor and/or

overhead have

been added.

C4

24

14-P1: Income Statement

25

18 - 26

Manufacturer’s Income Statement

P1

26

18 - 27

Cost of Goods Sold for a

Merchandiser and Manufacturer

Cost of goods sold for

manufacturers differs

only slightly from cost of

goods sold for

merchandisers.

P1

27

NEED-TO-KNOW

Indicate whether the following financial statement items apply to a manufacturer, a merchandiser, or a

service provider. Some items apply to more than one type of organization.

1. Merchandise inventory

2. Finished goods inventory

3. Cost of goods sold

Manufacturer

4. Operating expenses

5. Cost of goods manufactured

6. Supplies inventory

Merchandiser

Produces units for sale

Purchases units for resale

Balance Sheet includes:

Raw Materials Inventory

Work in Process Inventory

Finished Goods Inventory

Balance Sheet includes:

Merchandise Inventory

Manufacturer

1. Merchandise inventory

2. Finished goods inventory

3. Cost of goods sold

4. Operating expenses

5. Cost of goods manufactured

6. Supplies inventory

P1

X

X

X

X

X

Service Provider

Does not provide a product to its

customers; no inventories.

Merchandiser

X

Service Provider

X

X

X

X

X

28

14-C5: Flow of Manufacturing

Activities

29

18 - 30

Activities and Cost Flows

in Manufacturing

C5

30

14-P2: Schedule of Cost of

Goods Manufactured

31

18 - 32

Schedule of Cost of Good

Manufactured

Summarizes the types and amounts of costs

incurred in a company’s manufacturing process.

P2

+

+

=

+

–

=

Direct Materials Used

Direct Labor

Factory Overhead

Total Manufacturing Costs

Beginning Work in Process

Ending Work in Process

Cost of Goods Manufactured

32

18 - 33

Manufacturing Statement

P2

33

18 - 34

Manufacturing Statement

P2

34

18 - 35

Manufacturing Statement

Include all direct labor costs

incurred during the current period.

P2

35

18 - 36

Manufacturing Statement

P2

36

18 - 37

Manufacturing Statement

P2

37

18 - 38

Overhead Cost Flows Across

Accounting Reports

P2

38

NEED-TO-KNOW

Compute the following three measures using the information below.

1. Cost of materials used

$70,900 Cost of Direct Materials transferred from Raw Materials Inventory to Work in

Process Inventory.

2. Cost of goods manufactured

$173,900 Cost of goods completed in the current period and transferred from Work in

Process Inventory to Finished Goods Inventory.

3. Cost of goods sold

$160,500 Cost of goods leaving Finished Goods Inventory and going to the customer.

Expensed on the income statement.

Beginning raw materials inventory

Beginning work in process inventory

Beginning finished goods inventory

Raw materials purchased

Total factory overhead used

Raw Materials Inventory

Beg. Inv.

Purchases

15,500

66,000

Avail for Use

81,500

P1/P 2

10,600

Ending raw materials inventory

$10,600

Ending work in process inventory 44,000

Ending finished goods inventory

37,400

Direct labor used

38,000

Work in Process Inventory

Beg. Inv.

Matls. Used

Direct Labor

Fact. OH

Avail for Mfg.

Matls. Used

End. Inv.

$15,500

29,000

24,000

66,000

80,000

29,000

70,900

38,000

80,000

217,900

70,900

44,000

24,000

173,900

Avail for Sale 197,900

Cost of GM

End. Inv.

Finished Goods Inventory

Beg. Inv.

Cost of GM

173,900

Cost of GS

End. Inv.

160,500

37,400

39

NEED-TO-KNOW

Raw Materials Inventory

Beg. Inv.

Purchases

15,500

66,000

Avail for Use

81,500

Matls. Used

End. Inv.

10,600

Work in Process Inventory

Beg. Inv.

Matls. Used

Direct Labor

Fact. OH

Avail for Mfg.

70,900

44,000

Balance Sheet

Current assets:

Raw Materials Inventory

Work in Process Inventory

Finished Goods Inventory

Income Statement

Sales

Cost of Goods Sold

P1/P 2

Beg. Inv.

Cost of GM

24,000

173,900

Avail for Sale 197,900

Cost of GM

End. Inv.

Finished Goods Inventory

29,000

70,900

38,000

80,000

217,900

173,900

Cost of GS

End. Inv.

160,500

37,400

$10,600

44,000

37,400

$XXXXX

(160,500)

40

14-C6: Trends in Managerial

Accounting

41

18 - 42

Trends in Managerial Accounting

Customer

Orientation

E-Commerce

Lean Practices

C6

Global

Economy

Service

Economy

Value Chain

42

18 - 43

Customer Orientation

C6

43

18 - 44

Total Quality Management

Quality improvement

applied to all aspects of

business activities.

Seek and uncover

waste.

Constant Focus on

Higher Standards

Employees encouraged

to try new methods

to improve quality.

C6

Company emphasizes

value of quality through

quality awards.

44

18 - 45

Just-In-Time (JIT) Manufacturing

Receive

customer

orders

Complete products

just-in-time to

ship to customers

Schedule

Production

Receive materials

just-in-time for

production

C6

Complete parts

just-in-time for

assembly into products

45

18 - 46

Value Chain

The value chain refers to the series of activities that

add value to a company’s products or services.

Companies can use lean practices to increase

efficiency and profits.

C6

46

Global View

47

14-A1: Raw Materials

Inventory Turnover and Days’

Sales

48

18 - 49

Raw Materials Inventory Turnover

Raw materials

Inventory turnover =

A1

Raw materials used

Average materials

inventory

49

18 - 50

End of Chapter 14

50