Accounts Payable

advertisement

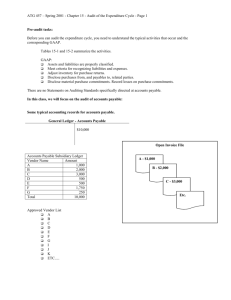

Acquisitions and Payments Accounts Payable Accounts Payable – Substantive Testing • What are accounts payable? • Acquisition and payments are • Both the ending liability and the transactions often involve Accounts Payable-2 Designing Tests of Details of Balances of Accounts Payable Set materiality. Assess Audit Risk and Inherent Risk for A/P Assess Control Risk for Accounts Payable Identify assertions where substantive testing is insufficient, and/or there is risk of material misstatement Design and perform test of control. Assess control risk The type of audit procedures? What is the sample size? Items to be selected? Timing – when to do the procedures? Design and perform substantive tests. Includes test of details and analytical procedures Accounts Payable-3 Tests of Detail of Balance of Accounts Payables Existence Recorded acquisitions are for items that were acquired 1. Trace from the accounts payable listing 2. Confirm accounts payable 3. Scan voucher register 4. Examine underlying documents for authenticity and reasonableness Accounts Payable-4 Best Company 522 Spring Hope Drive Somewhere, Ontario L2T-7Y6 January 7, 201Y Hunter Company 322 Vernon Road Elsewhere, Ontario L2R-3W4 Our auditors, Sell &Ross LLP, are conducting an audit of out financial statements. For this purpose, please furnish directly to them, at their address noted below, the following information as of December 31, 201X. (1) Itemized statements of our accounts payable to you showing all unpaid items; (2) A complete list of any notes and acceptances payable to you (including any which have been discounted) showing the original date, dates due, original amount, unpaid balances, collateral and endorsers; and (3) An itemized list of your merchandise consigned to us. Your prompt attention to this request will be appreciated. A stamped, addressed envelope is enclosed for your reply. Yours truly George Winters Sell & Ross LLP Chartered Accountants 841 Main Street Our Town, Ontario L2S-9J1 Best Company per George Winters Accounts Payable-5 • Completeness • To ensure that existing accounts payable • Search for unrecorded liabilities 1. Examine documents underlying vouchers subsequent to the B/S date 2. Examine the documents underlying invoices not yet recorded 3. Using the last receiving report number at the time of the inventory observation Accounts Payable-6 • Cutoff • To determine if the transactions are recorded in the correct period 1. Testing cutoff Accounts Payable-7 • Obligations • The client has an obligation to pay 1. Vendors’ statements 2. Confirmations Accounts Payable-8 • Accuracy • Acquisitions are recorded for the proper amounts 1. Can use the same procedures as those for existence Accounts Payable-9 • Detail tie-in • Accounts payable listing agrees with 1. Footing 2. Tracing the total Accounts Payable-10 • Classification • Accounts payable in the listing are properly classified 1. Scanning Accounts Payable-11 • Presentation and disclosure • Acquisitions are recorded to result in presentation according to GAAP 1. Review the financial statements Accounts Payable-12 Analytical Procedures for Accounts Payable • Compare acquisition-related expense account balances with prior years. • Review list of accounts payable for unusual, non-vendor, and interest bearing payables. • Compare individual accounts payable with previous years. • Calculate ratios such as purchase divided by accounts payable, and accounts payable divided by current liabilities. Accounts Payable-13 OKRA DEVELOPMENT CORP. 867 8924 Bailey Road, Salem, OR 92117 Sept. 4, 201X Pay to the order of Faragut Sales, Inc. $474.40 Four hundred and seventy 40/100----------------- Dollars Dewey Lee THE BANK of OREGON Treasurer CHEQUE REGISTER Page 292 Voucher Payee Faragut Sales, Inc Vouchers Purchase Cash Cheque No. No. Date Payable Dr. Discounts Cr Cr 867 9-00018 Sept. 4, 201X 480.00 9.60 470.40 Accounts Payable-14 Tests of Details for Cash Payments Examining documents underlying cash payments 1. • What documents? • Existence of the documents provides evidence • Approvals of the documents • A paid cheque • Recalculation of the discount • Accuracy of posting to the accounts Accounts Payable-15 2. Reconciling cash payments per book to cash payments per bank • Proof of cash • Usually performed when controls over recording cash are weak • Excellent evidence of completeness 3. Bank reconciliation • Bank reconciliations • Receiving bank statements directly from the bank • Bank cutoff statements • Bank confirmation Accounts Payable-16 The Nature of Capital Assets • Typically capital assets are used in manufacturing • Operational use and normal life of greater than one year Accounts Payable-17 Tracking Capital Assets • Large organizations • The source of information for • Small organizations may have a manual listing of such assets Accounts Payable-18 Audit Emphasis for Manufacturing Asset Additions • Emphasis is on auditing • For tax purposes • Amortization and accumulated amortization Accounts Payable-19 Categories of Audit Tests for Capital Assets • Audit emphasis is the verification of: – Current-year acquisitions – Current-year disposals – The ending balance in the asset account – Amortization expense – The ending balance in accumulated amortization • For tax purposes Accounts Payable-20 Analytical Procedures for Capital Assets • Compare amortization expense divided by gross manufacturing equipment cost with previous years • Compare accumulated amortization divided by gross manufacturing equipment cost with previous years • Compare monthly or annual repairs and maintenance, supplies expense, small tools expense, and similar accounts with previous years • Compare gross manufacturing cost divided by some measure of production with previous years Accounts Payable-21 Verification of Asset Balances • Relevant internal controls over existing assets • Audit tests • Agree last years ending balances • How about asset additions and disposals? Accounts Payable-22 Verification of Current Year Acquisitions • Important because • Starting point is normally a continuity schedule prepared by the client • An important technique is examination of Accounts Payable-23 Verification of Current Year Disposals • The most important internal control over disposals is the existence of a formal method to inform management • The most important audit procedures are • Vouch disposal to Accounts Payable-24 Verification of Amortization Expense and Accumulated Amortization • Amortization Expense • Primary audit objectives involve determining whether the client is: • Accumulated Amortization • Debits are normally tested as a part of • Credits are verified as part of Accounts Payable-25 Audit of Prepaid Expenses • Prepaid expenses arise from the concept of matching expenses with revenues • Prepaid insurance is a common expense • Look at the file of insurance policies in force Accounts Payable-26 Question 16-11, page 529 • Explain why it is common for auditors to send confirmation requests to vendors with “zero balances” on the client’s accounts payable listing but uncommon to follow the same approach in verifying accounts receivable. Accounts Payable-27 Problem 16-21, Page 530 Because of the small size of the company and the limited number of accounting personnel, Dry Goods Wholesale Company Ltd. initially records all acquisitions of goods and services at the time that cash disbursements are made. At the end of each quarter when financial statements for internal purposes are prepared, accounts payable are recorded by adjusting journal entries. The entries are reversed at the beginning of the subsequent period. Except for the lack of a purchasing system, the controls over acquisitions are excellent for a small company. (There are adequate prenumbered documents for all receipt of goods, proper approvals, and adequate internal verification wherever possible.) Before the auditor arrives for the year-end audit, the bookkeeper prepares adjusting entries to record the accounts payable as of the balance sheet date. The aged trial balance is listed as of the year end, and a manual schedule is prepared adding amounts that were entered in the following month. Thus, the accounts payable balance equals the aged trial balance plus the following month's journal entry for invoices received after year end. All vendors’ invoices supporting the journal entry are retained in a separate file for the auditor’s use. In the current year, the accounts payable balance has increased dramatically because of a severe cash shortage. (The cash shortage apparently arose from expansion of inventory and facilities rather than a lack of sales.) Many accounts have remain unpaid for several months, and the client is getting pressure from several vendors to pay the bills. Since the company had a relatively profitable year, management is anxious to complete the audit as early as possible so that the audited statements can be used to obtain a larger bank. loan. REQUIRED a. Explain how the lack of a complete aged accounts payable trial balance will affect the auditor’s tests of controls for acquisitions and cash disbursements. b. What should the auditor use as a sampling unit in performing tests of acquisitions? c. Assume that no misstatements are discovered in the auditor’s tests of controls for acquisitions and disbursements. How will that assumption affect the verification of accounts payable? d. Discuss the reasonableness of the client’s request for an early completion of the audit and the implications of the request from the auditor’s point of view. e. List the audit procedures that should be performed in the year-end audit of accounts payable to meet the cutoff objective. f. State your opinion as to whether it is possible to conduct an adequate audit in these circumstances. Accounts Payable Solutions-28 Problem 16-22, p. 531 You were in the final stages of your examination of the financial statements of Ozine corporation for the year ended December 31, 2011, when the corporation’s president came to talk to you. He believed that there was no point to your examining the 2012 acquisitions data files and testing data in support of 2012 entries. He stated that (1) bills pertaining to 2011 that were received too late to be included in the December acquisitions data files were recorded by the corporation as of the year end by journal entry, (2) the internal auditor made tests after the year end, and (3) he would furnish you with a letter confirming that here were no unrecorded liabilities. REQUIRED a. Should a public accountant’s test for unrecorded liabilities be affected by the fact that the client made a journal entry to record 2011 bills that were received late? Explain. b. Should a public accountant’s test for unrecorded liabilities be affected by the fact that a letter is obtained in which a responsible management official confirms that, to the best of his or her knowledge, all liabilities have been recorded? Explain. c. Should a public accountant’s test for unrecorded liabilities be eliminated or reduced because of the internal audit tests? Explain. d. Assume that the corporation, which handled some government contracts, had no internal auditor but that the Auditor General’s office spent three weeks auditing the records and was just completing her work at this time. How would the public accountant’s unrecorded liability test be affected by the work of the auditor from the Auditor General's office? e. What sources in addition to the 2011 acquisitions data files should the public accountant consider to locate possible unrecorded liabilities? Accounts Payable Solutions-29