Accounting

advertisement

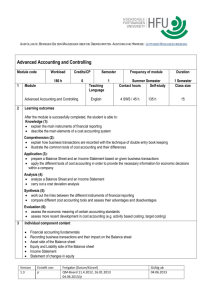

Course outline Course unit title Name and title of lecturer Level of course Semester ECTS credits Working hours Prerequisites Language of instruction Objectives of the course Adjusted with the expected learning outcomes Accounting theory Viktoras Filipavičius, Ph.D. Cycle 1 3 5 Contact hours 48 lectures 24 seminars classes 16 laboratory classes consulting 8 Self-study 82 Total 130 Microeconomics, Business English Lithuanian and English Learning outcomes Student knowledge, comprehension, skills and abilities Assessment methods Activities where the learning outcomes are demonstrated, proved Will comprehend accounting as an information system and will be able to use it in making decisions on the enterprise management. Will know the basic accounting concepts, regulations and principles. Will be able to work independently with information sources. Will comprehend the calculation procedures of assets, equity and liabilities, revenue and cost structure, financial performance. Will comprehend major economic activity fundamentals Will be able to make basic financial statements Will be able to independently analyse and evaluate the contents of the financial statements. Teaching methods lectures classes discussions case studies The main goal of the course is to make students to be fluent in finance reporting as well as be familiar with the basics of financial accounting Course unit content Topic 1. Tests. Progress tests. Practical classes. Examination. Contact hours Typical economic activities of the company. Accounting 1 2 Self-study assignments and hours Read and solve problems: incorporation into management cycle. Internal and external information users. 4 questions accountant must answer while processing information about entity’s transactions. Financial position of the company. The double entry in accounting. The master equation in accounting. The definitions of the assets, and claims. 2. Journalizing the economic transactions of the sample company. Preparing of elementary internal and external financial reports 3. Symmetry in accounting and debit-credit rules. Journalizing the economic transactions of the sample company. Particular assessment: find unknown balance of one account in the trial Balance. Horngren et al., ch.1 Ivanauskienė 2,3 sk. 2 2 Read and solve problems: Horngren et al., ch.1&2 Ivanauskienė 2, 3 sk. 3 1 Read and solve problems: Horngren et al., ch.2 Ivanauskienė 4 sk. 4 1 Read and solve problems: Horngren et al., ch.1-3 Ivanauskienė, 8 sk. 2 3 Read and solve problems: Horngren et al., appendix E Ivanauskienė 4 sk. 2 1 Read and solve problems: Horngren et al., ch.1-3 Ivanauskienė, 1-8 sk. 4. Practicing working with T-accounts: various typical transactions with deferrals and accruals. Student team competition for bonuses. 5. Generally accepted accounting principles and harmonization with IFRS issue. Quiz. 6. MIDTERM EXAM 1 ON GENERAL ITEMS IN ACCOUNTING THEORY 7. General Journal-General Ledger accounting model. The compulsory properties of the source documents. GL as the instrument “data/filter”. Journalizing the economic transactions of the sample company. Trial Balance. Adjustments. Internal reports. External reports – Lithuanian extended Income statement and Balance sheet. 6 2 8. Accounting for cash and means of cash control. Short-term financial assets. 2 9. Accounting for Accounts Receivable. Doubtful accounts, bad debts. Fair value of Accounts Receivable. Control of Accounts Receivable. Average cash collection period. 10. Physical movement of the inventory in a trading and manufacturing company. Accounting for inventory, its valuation by FIFO, LIFO, average, gross profit methods. 11. Tangible and intangible long-term assets. Goodwill. Typical transactions of acquiring and disposal of long-term assets. Amortization, depreciation, depletion, deterioration, obsolescence of the long-term assets. Linear, accelerated depreciation, production method. Accumulated depreciation (amortization). 12. Accounting for long-term liabilities: accounting for loans, financial 2 8 Read and solve problems: Horngren et al., ch. 3 Ivanauskienė, 6, 8 sk. 4 Read and solve problems: Horngren et al., ch.4 Bukevičius et al., 5.7 sk. 2 Read and solve problems: Horngren et al., ch.5 3 6 Read and solve problems: Horngren et al., ch.6 Ivanauskienė 9.3-9.4 sk. 6 Read and solve problems: Horngren et al., ch.7 Ivanauskienė 9.2 sk. 4 6 Read and solve problems: 4 lease, bonds, Horngren et al., ch.8 Bukevičius et al., 6 sk. 13. MIDTERM EXAM 2 ON CASH, ACCOUNTS RECEIVABLE, INVENTORY VALUATION, FIXED ASSETS DEPRECIATION ACCOUNTING 14. Cash flow statement. Direct and indirect methods of preparing of cash flow statements. Practicing preparing indirect cash flow statement. 15. Submit homework. 2 6 Horngren et al., ch.4-7 Ivanauskienė 9 sk. Bukevičius et al., 5.7 sk. 4 8 Read and solve problems: Horngren et al., ch.12 Ivanauskienė 10.5.3 sk. VAS6, IAS7 16. INTERIM EXAM ON EQUITY AND LONG-TERM LIABILITIES ACCOUNTING 2 17. 6 Read and solve problems: Horngren et al., ch.8&9 Ivanauskienė 2.3 sk. Bukevičius et al., 6 sk. 8 Read and solve problems: Horngren et al., ch.11-13 Ivanauskienė 10 sk. FINAL EXAM 10 48 82 Reading list Year of publishing 2004 2006 2007 Author‘s name, title of the publication Harrison W., Horngren Ch. Financial Accounting. Ivanauskienė A. Buhalterinės apskaitos pagrindai. Bukevičius J., Burkšaitienė D., Paliulis N., Žaptorius J. Apskaita vadybininkams Verslo apskaitos standartai: www.aat.lt International accounting standards: http://eurlex.europa.eu/LexUriServ/LexUriServ.do?uri=CONSLEG:2008R1126: 20111126:EN:PDF Publishing House Prentice Hall Vilnius: “TEV” Technika (el.versija) Audito ir apskaitos tarnyba IASB Additional reading Year of publishing 1993 2007 2012 2006 Author‘s name, title of the publication Dauderis H Finansų apskaita (I ir II dalys). Alexander D., Nobes C. Financial accounting. An international introduction. Rudžionienė K. Finansinės apskaitos teorijos. Atrill P. and McLaney E. Accounting and Finance for Non-Specialists, 5th ed. 3 Publishing House Kaunas: Pasaulio lietuvių kultūros, švietimo ir mokslo centras Prentice Hall Vilnius:VUL Prentice Hall 2010 Žaptorius J. Apskaita: pratimai ir testai. Assessment requirements Assessment criteria The composition of final cumulative mark Course outline composed by Approved by the Study Program Committee “Technika” The midterms and homework are in written. Midterm assignments are 50 percent approximately of multiple choice, and 50 percent are problems. The duration of each midterm is 2 hours. The final exam is in written. One assignment is of multiple-choice, and remaining five are problems. The duration of the exam is 3 hours. Knowledge of the set of annual financial reports. Ability to prepare Income statement and Balance sheet for a given Trial balance with approx. 20 account balances. Ability to extract relevant information from Income statement and Balance sheet. Knowledge of the basic correspondence between accounts. Knowledge about the information flow in the accounting system and its relevance to the management decisions. Final cumulative mark = 15% * the 1st midterm + 15% * the 2nd midterm + 15% * the 3rd midterm + 15% * homework + 40% * the final exam N.b.: students can gain bonuses for their midterms and the final exam. The bonuses are granted for: attendance, extra assignments, active participation in discussions and during classes. The bonus impact, say, to the 1st midterm is as follows: The final grade for the 1st midterm = Bonus + + (1 – Bonus/10) *Actual grade for the 1st midterm The same formula is applicable for remaining midterm 2 and 3, and for exam. The magnitude of the particular bonus is settled by the tutor. Viktoras Filipavičius 4