recovery of arrears of revenue

advertisement

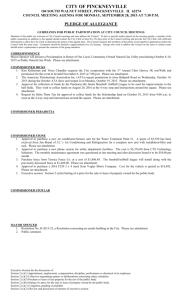

WELCOME An overview on RECOVERY OF ARREARS OF REVENUE “Doubt is not a pleasant condition, but certainty is absurd” -Voltaire RECOVERY OF ARREARS OF REVENUE Arrears arise as a result of OIO, OIA, Tribunal orders, Courts’ Orders or Default under Rule 8 Thousands of crores due Not only huge amount is locked up, recovery of arrears helps in achieving the targets and nation building. Board has set it as a top priority area Therefore, is an important task FOLLOWING ARE NOT ARREARS: Unconfirmed demands Orders set aside Orders sent for denovo adjudication SCNs transferred to call book Cases under investigation RECOVERABLE OR NOT All stayed arrears are not recoverable. All unstayed arrears are recoverable. ( Chief Commissioner (TAR) letter in C.No.CC(TAR)79/2011 dated November 29,2011) Recoverable(unstayed) arrears are three types Restrained Fit for write-off Unrestrained Unstayed but Restrained Arrears Cases where department is prevented from recovery for some reason- BIFR /DRT/OL cases Cases where Stay Applications by Commissioner(A)/CESTAT not decided Cases where 180 days has elapsed after grant of stay by CESTAT but party has applied for extension of stay before CESTAT Cases pending with Settlement Commission and R.A Cases pending under Section 11C (Circular 684/75/2002 CX) Fit for Write –Off Cases: Units closed Defaulters not traceable Directors of Public/Private Limited Companies available but assets of the Company not available All types of action to recover exhausted Unrestrained Arrears: All other arrears are “unrestrained recoverable” arrears. For example cases where Sec 11 action initiated/intended Certificates to District Collector are sent Sec 142 action initiated/intended letters are sent to DGCEI/DRI/FIU for identifying assets certificates to other Customs /C.E formations awaiting reply awaiting sale of movable/immovable property cases where Sec 87 action initiated/intended other recoverable arrears cases where factories are running/operational and assets are available ACTIONS : Persusasive action Coercive action Write off COERCIVE ACTION: Deducting from any money owed to the defaulter (Sec 11) Attachment and sale of excisable goods belonging to the defaulter (Sec 11 ) Attachment and sale of goods in possession/custody of transferee/successor (Sec 11) Certificate Action to the District Collector (Sec 11) Deducting any money owed to the defaulter/detention and sale of goods under any other officers of Customs , Central Excise (Sec 142 (1 ) (a)&(b)) Attachment and sale of movable and immovable properties (Sec 142 (1)(c) (ii)) COERCIVE ACTION Primary responsibility is on Range Officers and Divisional AC/DC Headquarters level AC/DC (ARC) is authorised by the Commissioner for attachment and sale of movable and immovable properties after the proposal is received from the divisional AC/DC Commissioner (ARC) at metros monitors the recovery COERCIVE ACTION-STATUTORY PROVISIONS Section 11 of CEA, 1944 – Recovery of sums due to the Government - Any duty and any other sums payable under the Act or Rules - Officer may deduct the amounts from any money owing to such person which is in the officers hand or disposal or control - or, the officer to recover the amount by attachment or sale of excisable goods belonging to the defaulter STATUTORY PROVISIONS ….CONTD. if not so recovered, the officer should prepare a certificate and send it to the District Collector to recover it as arrears of land revenue (for amounts less 1 than Rs. lakh only and if not recovered within 3 months attachment movable/immovable properties process to be adopted. As per Board circular No. 54/95 dated 30-5-95 and 552/48/2000Cx dt. 4-10-2000.) STATUTORY PROVISIONS ….CONTD. - If the defaulter transfers or disposes whole or part of the business/trade or effects change in the ownership, all excisable goods, materials, preparations, plants, machineries, vessels, utensils, implements and articles in the custody or possession of the successor to be obtained and sold after obtaining written approval from the Commissioner of Central Excise. (Since 2004) STATUTORY PROVISIONS ….CONTD After exhausting the options mentioned already, if dues still remain unrecovered, action to be initiated under Sec. 142 (1)(b) of Customs Act made applicable to Central Excise matters as per Notification No. 68/63 CE dated 4-5-1963 by which AC/DC can require any other AC/DC of customs/excise anywhere in India to deduct from any refund/rebate or detain and sell any goods belonging to the defaulter . STATUTORY PROVISIONS ….CONTD. After exhausting the options mentioned already, if dues still remain unrecovered, action to be initiated under Sec. 142 (1) (c)(ii) of Customs Act, 1962 made applicable to Central Excise matters as per Notification No. 68/63 CE dated 4-5-1963 - CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 Rule 3 - Issue of Certificate - (Appendix I) Rule 4 - Issue of Notice (Appendix II) Rule 5 - Attachment of property (Appendix IIIA for Movable Property and Appendix III B for Immovable property) Rule 6 - Attachment not to be excessive Rule 7 - Attachment between sunrise and sunset CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 ….Contd. Rule 8 - Inventory Rule 9 - Defaulter or his representative not competent to mortgage, lease or otherwise deal with property or any transfer or delivery of the property to be void. Rule 10 - Share in property- attachment to be made by notice to the defaulter prohibiting from transferring the share or interest or changing it in any way CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 ….Contd. Rule 11 - Attachment of property in custody of court or public officer- Authorised officer to give a notice in Appendix V or VI to such court or the officer requesting that such property and any interest or dividend becoming payable thereon may be held subject to the further order of the authorised officer. Rule 12 - Service of notice of attachment Rule 13 Proclamation of attachment CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 ….Contd. Rule 14 Property exempt from attachment - Any property exempted from attachment and sale for execution of a decree of a civil court as per Code of Civil Procedure 1908 to be exempt from attachment Rule 15 - Sale of property - to be initiated after 30 days of the attachment of the property. Commissioner to fix the reserve price CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 . ….Contd Rule 16 - Negotiable instrument and shares in a corporation – to be sold through a broker – order of attachment on negotiable instrument in the form of Appendix VII A. In the case of shares, order in Appendix VIIB to be issued to the defaulter and principal officer of the company prohibiting them from transfer of any shares CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 ….Contd. Rule 17 - Proclamation of sale - to be made in the language of the district Rule 18 - Contents of the proclamation – shall state the time and place of sale and specify (a) Property to be sold (b) the revenue if any, assessed on the property (c) the amount for the recovery (d) the reserve price, etc. CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 . ….Contd Rule 19 - Mode of making proclamation – Beat of drum or other customary mode and copy of the proclamation shall be affixed on the property as well as in the office of the proper officer Rule 20 - Setting aside of the sale where defaulter has no saleable interest – within 30 days of the sale CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 . ….Contd Rule 21 - Confirmation of the sale – in the form of Appendix X – If confirmation is not made, notice to the interested parties to be issued in the form of Appendix IX Rule 22 - Sale certificate in the form of Appendix XI CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 . ….Contd Rule 23 - Purchaser’s title – from the time the property sold and not from the time the sale become absolute. Rule 24 - Irregularity not to vitiate sale, but injured person may sue Rule 25- Prohibition against bidding or purchase by officers Rule 26 - Prohibition against sale on holidays CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 . ….Contd Rule 27 - Disposal of the sale proceeds (a) first towards meeting of the cost of the sale (b) towards the recovery of the arrears mentioned in the certificate and cost of detention of the property (C) the balance if any towards recovery of any other government dues payable by the defaulter (d) balance if any, to be paid to the defaulter CUSTOMS (ATTACHMENT OF PROPERTY OF DEFAULTERS FOR RECOVERY OF GOVERNMENT DUES) RULES, 1995 ….Contd. Rule 28 - Procedure on death of defaulter – if defaulter dies after the certificate under Rule 3 is issued, proceedings to be against the legal representatives of the defaulter Procedure and formats of the Appendices given in Board’s Circular No. 365/81/97-CX dated 15-12-1997 Procedure where defaulter is not traceable: Write to Sub Registrar to get details of immovable properties Write to Municipal authorities to ascertain the title/ownership of the land/building where the unit is located Write to Income Tax Department and obtain Income Tax Returns Write to Bank and obtain details likd cash balance / FD’s /lockers etc., Obtain details from RTA on the vehicles/cars Write to Registrar of Companies (ROC) to ascertain the assets and liabilities , any new companies started, details of Directors and their assets etc., Write to Post Office for ascertaining changed address and whereabouts Write to Police for changed address and whereabouts Write to respective trade associations for whereabouts, present address and activities Make discreet enquiries to trade rivals - Standing order No. 09/2010 CE Dt. 30.9.2010 issued by Hyderabad III Commissionerate WRITE OFF Sl. No. Competent Authority Constitution of the Committee Powers delegated 1. Chief Commissioner of Customs & Central Excise/ Central Excise/ Customs Committee of two Chief Commissioners of Customs & Central Excise/ Central Excise/ Customs and the Chief Commissioner (TAR) (a) Full powers for abandonment of irrecoverable amounts of fines and penalties imposed under Customs Act, 1962, and Central Excise Act, 1944. Committee of two Commissioners of Customs & Central Excise/ Central Excise/ Customs and one Commissioner (TAR) nominated by CC(TAR)) (b) To write off irrecoverable amounts of Customs/Central Excise duties upto Rs. 15 lakh subject to a report to the Board (a) Full powers for abandonment of irrecoverable amounts of fines and penalties imposed under Customs Act, 1962, and Central Excise Act, 1944. 2. Commissioner of Customs & Central Excise / Commissioner of Customs / Commissioner of Central Excise (b) To write off irrecoverable amounts of Customs/Central Excise duties upto Rs. 10 lakh subject to a report to the Chief Commissioner WRITE OFF …. Interest amount would get automatically written off once the duty involved is written off. Proforma for sending proposals for written off is very stringent and exhaustive and is required to be signed by the DC/AC Incharge. Suppose duty , fine, penalty are paid and only interest is required to be paid, can it be written off under this Circular? (Authority -Circular 946/07/2011 dt 01-06-2011) CBEC Circular 788/21/2004CX dated 25-5-2004 If stay application is filed before Commissioner (Appeals), no coercive action till the disposal of the stay application. Normally, 3 months from the date of communication of the order/OIA to be provided before taking coercive action. In respect of Tribunal/High Court/GOI orders, one month to be given before taking coercive action. CBEC Circular 778/21/2004CX dated 25-5-2004… contd. In case of Supreme Court Order only 15 days to be given. Same procedure to be applicable for recovering of defaulted amounts under Rule 8 also. If only is appeal is filed before Commissioner (A) and no stay application is filed, recovery proceedings to be started after 60 days. CBEC Circular 778/21/2004CX dated 25-5-2004… contd. If only appeal is filed to Tribunal but no stay application is filed, against Commissioners orders, 90 days time to be given before taking coercive action in respect of stay application filed before Tribunal against Commissioner’s orders, 6 months time or time till the disposal of the stay petition , whichever is earlier to be given- (Sec. 35C(2A) of CEA,1944). This is for first stage appeals only. Action on expiry of stay orders by CESTAT (Circular No. 925/15/2010 Cx dated 25.5.2010): Department to issue a simple letter asking the party to pay and party will be at liberty to go back to the tribunal for seeking extension of stay Tribunal order granting indefinite stay could be challenged before the jurisdictional High Court Provisional Attachment of Property during Pendency of Proceedings 11 Sec. DDA of CEA, 1944 w.e.f. 13-11-2006 (Sec 73C in case of S.T)provides for provisional attachment of property to protect the interest of revenue during the pendency of any proceedings u/s 11A or 11D Proceedings to be initiated only after SCN is issued Proposal to be put up to Commissioner within one month of issue of notice Provisional Attachment of Property during Pendency of Proceedings ….Contd. Grounds to entertain the belief that the noticee would dispose off or remove the property and the source of information should be clearly stated. The remedy of attachment being extraordinary in nature, to be resorted to with utmost circumspection, maximum care and caution. Disciplinary action, if powers are exercised frivolously without sound reasons Provisional Attachment of Property during Pendency of Proceedings … contd. Commissioner to issue notice to the person and after following principle of natural justice grant approval Offences covered are: clandestine removal, undervaluation, fraudulant cenvat credit availment, issue of invoice without delivery of goods, claiming of fraudulent refund/rebate. Provisional Attachment of Property during Pendency of Proceedings …. contd. Attachment only if duty or credit is above Rs.25 lakhs Period of attachment to be operational only for 6 months, Chief Commissioner can extend for another 2 years Personal property in use of the person of a sole proprietorship or partners of a firm should not be attached. Immovable property used in commercial purpose can be attached. Provisional Attachment of Property during Pendency of Proceedings … contd. Movable property to be attached only if immovable property is not available Normal manufacturing activities should not be hampered, i.e., raw materials/inputs should not be attached. Inventory to be drawn and copy to be handed over to the person Provisional Attachment of Property during Pendency of Proceedings … contd. Property exempted for sale by a decree of a civil court not to be attached Authority Board Circular No. 874/12/2008 CX dated 30-6-2008 RECOVERY OF S.T ARREARS SECTION 87 Recovery of any amount due to Central Government (a) the Central Excise Officer may deduct or may require any other Central Excise Officer or any officer of customs to deduct the amount so payable from any money owing to such person which may be under the control of the said Central Excise Officer or any officer of customs RECOVERY OF S.T ARREARS…. (b) (i) the Central Excise Officer may, by notice in writing, require any other person from whom money is due or may become due to such person, or who holds or may subsequently hold money for or on account of such person, to pay to the credit of the Central Government either forthwith upon the money becoming due or being held or at or within the time specified in the notice, not being before the money becomes due or is held, so much of the money as is sufficient to pay the amount due from such person or the whole of the money when it is equal to or less than that amount RECOVERY OF S.T ARREARS…. (iv) every person to whom a notice is issued under this section shall be bound to comply with such notice, and, in particular, where any such notice is issued to a post office, banking company or an insurer, it shall not be necessary to produce any pass book, deposit receipt, policy or any other document for the purpose of any entry, endorsement or the like being made before payment is made, notwithstanding any rule, practice or requirement to the contrary; RECOVERY OF S.T ARREARS…. (iii) in a case where the person to whom a notice under this section is sent, fails to make the payment in pursuance thereof to the Central Government, he shall be deemed to be an assessee in default in respect of the amount specified in the notice and all the consequences of this Chapter shall follow; RECOVERY OF S.T ARREARS…. (c) the Central Excise Officer may, on an authorisation by the Commissioner of Central Excise, in accordance with the rules made in this behalf, distrain any movable or immovable property belonging to or under the control of such person, and detain the same until the amount payable is paid; and in case, any part of the said amount payable or of the cost of the distress or keeping of the property, remains unpaid for a period of thirty days next after any such distress, may cause the said property to be sold and with the proceeds of such sale, may satisfy the amount payable and the costs including cost of sale remaining unpaid and shall render the surplus amount, if any, to such person; RECOVERY OF S.T ARREARS…. (d) the Central Excise Officer may prepare a certificate signed by him specifying the amount due from such person and send it to the Collector of the district in which such person owns any property or resides or carries on his business and the said Collector, on receipt of such certificate, shall proceed to recover from such person the amount specified there under as if it were an arrear of land revenue. S.T. ARREARS VIS-À-VIS CENTRAL EXCISE ARREARS No provision for write off of ST arrears No provision for recovery of ST arrears from the successor/transferee Special provision for recovery of ST arrears from any funds owing to the defaulter which may be lying with a third party /Bank/Post Office/Insurance Company etc., GENERAL One more effective provision is powers u/s 37E to publish name of persons, companies, etc. Even names of partners, directors, managing agents, secretaries, members of associations can be published. In case of penalty no publication till the appeal period is over. Penalty to be paid in cash only and not by debiting the CENVAT credit. GENERAL … contd. Powers of recovery can be used against surety or guarantor also. Award scheme extended to informants of property of defaulters – MF (DR) letter No. 13011/3/2004 CUS (AS) dated 12-8-2005 Adjustment from refund/ rebate claims only after notice issued and principles of natural justice followed GENERAL … contd. Department itself cannot debit in PLA or Cenvat credit account to recover arrears. Goods not belonging to the person but under his control can be attached and sold Committee of Disputes (COD) procedure regarding appeals against PSUs dispensed with. (Director (Judicical Cell), instructions vide F.No. 390/R/262/09-JC dated 24.3.2011) GREY AREAS Power to grant installments? Adjustment from the amounts due to the another unit of the same company with different registration? Often machineries mortgaged to financial institutions and raw materials hypothecated to banks. Can they be attached? Meaning of the successor of the business- change of ownership/integrity of business remains the same/ substantially changed Crown Debts Krishna Lifestyle Technologies Ltd. Vs. UOI - Recovery of arrears- state has no priority State priority not applicable to secured creditors Attachment by CEX has no consequences over the bank’s right Bombay High Court judgment delivered in Feb., 2008 has been upheld by Supreme Court in 2009. Supreme Court held that excise authorities would have priority of claim only if there is a specific provision giving such priority to the state dues. Crown Debts…. Section 11E of CEA/Sec 88 of FA : (w.e.f 8-4-2011) creates a first charge on the property of a defaulter for recovery of Central Excise dues subject to the provisions of the Companies Act, Recovery of Debt Due to Banks and Financial Institutions Act, 1993 and Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002. This implies that after the dues, if any, owing under these provisions, dues under the Central Excise Act shall have a first charge. Disclaimer: This presentation is only meant to refresh your knowledge on the subject and all are requested to go through the relevant sections/rules/regulations/circulars/directions/ orders etc. before taking action in specific cases. THANK YOU D.V.REDDY Additional Commissioner