File - 10 Commerce

advertisement

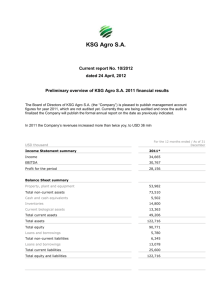

FINANCIAL STATEMENTS – In Detail Quick Summary Small businesses need to keep detailed records of the inflow and outflow of funds in their business so that they may track the success of the business and also for taxation purposes. The three types of financial statements that we will be looking at are: Revenue Statement Balance Sheet Cash flow statement Important Terms The following is a list of terms that are important to know when working on financial statements. We will discuss these terms as we move through the worksheet. Revenue expenses gross profit/loss Net profit/loss assets liabilities Owner’s equity liquidity Revenue Statement Businesses use revenue statements to measure their revenue against their expenses to figure out how much profit they are making. Important equations in a revenue statement are: Revenue – Cost of Goods Sold= Gross Profit Gross Profit- Expenses = Net Profit Revenue: The income earned by a business Expenses: costs incurred in running the business Gross Profit/loss: the amount remaining when the cost of goods sold is deducted from revenue Net Profit/loss: the amount remaining when operating expenses are deducted from gross profit What might be some expenses that a business might incur? _____________________________________________________ _____________________________________________________ _____________________________________________________ _____________________________________________________ Some things to remember when drawing up a Revenue Statement: There should be 3 columns The first column should hold the name of the cost or expense The second column should include the monetary figures related to the business’s expenses The third column should include the monetary figures related to the business’s revenue The third column should also include all the TOTALS , this includes the total gross profit, the total expenses and the total net profit An example of a REVENUE STATEMENT Revenue statement for the year ending 30 June 2012 $ Revenue Cash sales Less Cost of Goods Sold Gross Profit Less Expenses Wages Rent Electricity Net Profit $ 215,000 90,000 125,000 38,000 20,000 5,500 63, 500 61,500 Further Examples – Complete the Revenue Statements for the following businesses. Determine whether they have experienced a profit or loss for the year ending 30 th June. Sam’s Sports Cash Sales Cost of Goods Sold Wages Lease Payments Electricity Promotions Insurance $230,000 $125,000 $40,000 $15,675 $5,500 $2, 760 $4,900 $ $ Gloria’s Coffee Corner Cash Sales Cost of Goods Sold Lease Payments Electricity Free Samples Advertising Interest on Loan $195,000 $46,700 $15,000 $9050 $1,550 $5,500 $4,565 $ $ Matt’s Mechanic Cost of Goods Sold Gross Profit Wages Lease Payments Electricity Advertising Insurance $280,000 $450,000 $150,000 $30,580 $12,000 $5,000 $5,500 $ $ Diana’s Home Depot Cost of Goods Sold Gross Profit Wages Lease Payments Equipment Electricity Advertising Insurance Interest on Loan $75,080 $128,000 $42,000 $17,000 $5,000 $7,000 $4,560 $3,750 $4,590 $ $ Jayden’s Juice Store Cost of Goods Sold Gross Profit Wages Lease Payments Electricity Advertising Insurance $380,000 $440,000 $160,000 $20,580 $16,000 $6,000 $7,500 $ $ 1- What is the main use of revenue statement? ___________________________________________________________________________ ___________________________________________________________________________ 2- Construct a set of steps that somebody who doesn’t know much about revenue statements can use to construct one. ___________________________________________________________________________ ___________________________________________________________________________ ___________________________________________________________________________ ___________________________________________________________________________ ___________________________________________________________________________ Construct your very own Revenue Statement Name of Business: List of Revenue and Expenses Revenue Statement: $ $ Balance Sheet The balance sheet shows the statement of financial position of a business at a particular time. It can be thought of as a set of scales which weights what you own (assets) on one side and what you owe (liabilities) on the other. Both sides must balance The most important equation in a balance sheet is: Owner’s Equity= Assets- Liabilities OR Assets= Owner’s Equity + Liabilities Owner’s Equity: the value of the business to the owner Assets: items of value owned by the business Liabilities: debts owed by a business to others Some things to remember when drawing up a Cash Flow Statement: The left hand side of the balance sheet shows assets The right hand side of the balance sheet shows liabilities and owners equity Classify balance sheet items into one of the following categories Assets (Current or non-current) Liabilities (current or non-current) Owner’s Equity All statistics for each sub-topic should be written in the left-hand column of the appropriate section (assets, liabilities or owners’ equity) All totals for each section should be written in the right hand column of the appropriate section (assets, liabilities or owner’s equity). When all balance sheet items are entered on the balance sheet, both sides should have the same total. When determining the value of the owner’s equity, add up all items in the assets column, record the same total in the liabilities column, then subtract whatever liabilities are listed from the “Total liabilities and owners equity” figure. Important Terms Continued Examples of Current Assets Examples of Non-Current Assets Examples of Current Liabilities Examples of Non-Current Liabilities Examples of Owner’s Equity Example of a BALANCE SHEET Assets Current Assets Cash at bank Stock on hand $ $ $ $ Current Liabilities 68,000 Accounts payable 35,000 Total 35,000 22,300 Total 90,300 Non-Current Assets Equipment Liabilities Non-current liabilities 58,00 Motor Vehicle 37,000 Glasses and Cutlery 12,500 Bank loan 55,000 Total 55,000 Owner’s Equity Net Profit Retained Capital 61,500 46,300 Total 107,500 Total 107,800 Total Assets 197,800 Total liabilities and owners equity 197,800 Further Examples – Complete the Balance Sheets for the following businesses. Determine whether they have experienced a profit or loss for the year ending 30th June. Paul’s Pizza Cash Creditors Mortgage Pizza Ovens Assets Current Assets Total Non-Current Assets Loan Stock Delivery Vehicles Capital $450 $2,400 $10,000 $1,500 $ $ Liabilities Current Liabilities Total Non-current liabilities Total Owner’s Equity Total Total Assets Total Total liabilities and owners equity $680 $550 $15,000 $4,420 $ $ Ben’s Bakery Creditors Cash at bank Goodwill Capital Building Assets Current Assets Total Non-Current Assets $23,000 $8,000 $2,000 $13,500 $4000 $ $ Ovens Accounts receivable Profit Shares(in a company) Liabilities Current Liabilities Total Non-current liabilities Total Owner’s Equity Total Total Assets Total Total liabilities and owners equity $3,500 $23,500 $9,500 $5000 $ $ Frank’s Pharmacy Owner’s investment Bank loan Cash Equipment Assets Current Assets Total Non-Current Assets $10,000 $18,000 $15,000 $4,500 $ $ Stock Accounts payable Debtors Premises Liabilities Current Liabilities Total Non-current liabilities Total Owner’s Equity Total Total Assets Total Total liabilities and owners equity $5,500 $15,000 $8,000 $10,000 $ $ Sally’s Sports Debtors Owner’s Investment Creditors Cash at Bank Building Assets Current Assets Total Non-Current Assets $15,000 $3,500 $21,000 $8,000 $10,000 $ $ Bank Loan Stock Accounts payable Goodwill Liabilities Current Liabilities Total Non-current liabilities Total Owner’s Equity Total Total Assets Total Total liabilities and owners equity $4,500 $1,500 $9,000 $3,500 $ $ Danny’s Deli Cash in store Owner’s investment Debtors Building Bank Loan Creditors Profit Stock Assets Current Assets Total Non-Current Assets $6000 $8,505 $5,100 $5,000 $15,000 $2,745 $3,500 $6,500 $ Cash at Bank $20,100 $26,000 $3,500 $7,300 $1250 $3000 $5000 Capital Accounts payable Accounts receivable Goodwill Shares Equipment $ Liabilities Current Liabilities Total Non-current liabilities Total Owner’s Equity Total Total Assets Total Total liabilities and owners equity $ $ Cash Flow Statements A cash flow statement is used to keep track of the movement of cash within a business. By regularly comparing cash inflows and cash outflows a business is able to calculate its surplus or deficit cash. This is an important indicator of a business’s liquidity. Some important equations to remember when drawing up a cash flow statement is: Net Cash Flow= Total Cash Inflow – Total Cash Outflow Closing Cash Balance= Opening Cash Balance + Net Cash Flow Cash inflows: Money received by an organization as a result of its operating activities, investment activities, and financing activities. Money coming in. Cash outflows: Money paid out by an organization as a result of its operating activities, investment activities, and financing activities. Money going out. Net Cash flow: Total Cash inflow minus the Total Cash Outflow Opening cash balance: The cash already existing within the business. The closing cash balance from the previous cash flow statement. Closing cash balance: This is the Opening Cash Balance plus the Net Cash Flow. Steps to remember to when drawing up a Cash Flow Statement: 1. 2. 3. 4. Calculate the total cash inflows by adding up all the cash coming IN to the business. Calculate the total cash outflows by adding up all the expenses of the business. Calculate the Net cash flow (Total Cash Inflow minus Total Cash Outflow) Calculate the Closing Cash Balance (Net Cash Flow + Opening Cash Balance) How to set out a Cash flow statement: There should be 3 Columns The first column contains all the headings/labels. The second column contains all the monetary figures of things such as cash inflows and cash outflows The third column contains all the totals: total cash inflows, total cash outflows, net cash flow, opening cash balance and closing cash balance. Example of a Cash Flow Statement Sam’s Soccer Boots Cash flow statement for the year ending 30 June 2012 Net Operating Activities- 75,300 Wages – 38,000 Borrowed Funds- 55,000 Rent – 20,000 Opening Cash Balance – 11,000 Electricity- 5,500 $ $ Cash Inflows Net Operating Activities 75,300 Borrowed Funds 55,000 Total cash inflows 130,300 Cash outflows Wages 38,000 Rent 20,000 Electricity 5,500 Total cash outflows 63,500 Net cash flow (TCI-TCO) 66,500 Opening cash balance 11,000 Closing cash balance 77,500 Further Examples – Complete the Balance Sheets for the following businesses. Determine whether they have experienced a profit or loss for the year ending 30 th June. Peter’s Paint Store Net Operating Activities Borrowed Funds Wages Rent Electricity Maintenance Opening Cash Balance $85,000 $65,000 $20,000 $15,000 $6000 $4000 $10,000 $ $ Sam’s Skateboard Store Net Operating Activities Borrowed Funds Wages Paint Supplies Rent Electricity Maintenance Opening Cash Balance $65,000 $75,000 $30,000 $6000 $12,000 $4000 $2000 $12,000 $ $ Tim’s tutoring Net Operating Activities Borrowed Funds Wages Stationary Supplies Rent Electricity New Furniture Opening Cash Balance $85,000 $15,000 $35,000 $8000 $13,500 $4000 $7000 $21,000 $ $ Adam’s Aussie Restaurant Net Operating Activities Borrowed Funds Wages Ingredients Rent Electricity New Tables and Chairs Opening Cash Balance $105,000 $11,000 $25,000 $18,000 $17,500 $7000 $7000 $52,000 $ $ Tanya’s Telecommunications Net Operating Activities Borrowed Funds Wages New Display cabinets Rent Electricity Glass Cleaner’s fee Opening Cash Balance $305,000 $17,000 $75,000 $11,000 $23,500 $12,000 $7000 $22,000 $ $