Chapter 20

Chapter 24 Cost Accounting for Decision-making

A Relevant and irrelevant costs

1 Distinguish between relevant and irrelevant costs is important for business decision-making , as irrelevant costs are not to be considered in the decision-making process.

2 Relevant costs a Relevant costs are the expected future costs that must be considered when making a decision. b There are three major types of relevant costs

Opportunity costs

The opportunity cost of making a decision is the highest-valued alternative forgone.

Incremental costs

Incremental costs are the additional costs incurred when a certain action is taken.

Avoidable costs

Avoidable costs are the costs which can be reduced or avoided when a certain action is taken.

3 Irrelevant costs a b

Irrelevant costs are the costs that do not have to be considered when making a decision.

There are two major types of irrelevant costs:

Sunk costs

Sunk costs are the costs that have been incurred and cannot be recovered.

Unavoidable costs

Unavoidable costs are the costs which have to be incurred regardless of what action is taken.

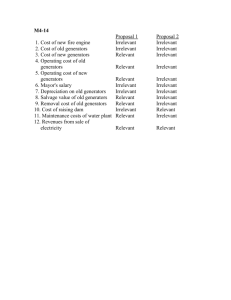

4 Determine the type of costs in the following situations: a A company plans to outsource its production activities. However, the company cannot lay off its factory workers due to contractual obligations. b

The wages of factory workers are an unavoidable cost.

A company plans to outsource some of its production activities. The part-time workers in its factory can be laid off without compensation after these production activities are outsourced.

The wages of part-time workers are an avoidable cost.

c d

A company purchased a motor vehicle five years ago for $50,000.

This purchases cost of $50,000 is a sunk cost.

A machine bought 10 years ago for $50,000 can now be sold for $10,000.

The $10,000 is the opportunity cost of keeping this machine. e A company incurs factory rental of $100,000 per month. After expanding the production capacity, factory rental will increase by $20,000 per month.

The $20,000 is the incremental cost of expanding the production capacity.

B Business decision-making

5 Management often needs to make a decision in the following situation: a b

Accept or reject an order at a special price

Hire, make or buy c d e

Sell or process further

Retain or replace equipment

Eliminate or retain an unprofitable segment

6 When making a choice, we should always compare the effect on net profit or total manufacturing costs.

7 When there is a limiting factor, you need to consider the opportunity costs associated with it.

8 The historical cost and net book value of an asset is usually irrelevant, while the disposal value of an asset is usually relevant.

9 When making a decision, besides considering the various costs, we should also consider the qualitative factors.

C Joint products

10 Joint products refer to two or more products produced simultaneously from the same raw material by a common production process.

11 Joint costs are the costs of a single production process that simultaneously yields multiple products.

12 Joint costs are irrelevant in incremental analysis as they are the same whether there is further processing or not.