Investment Overview March 2013

advertisement

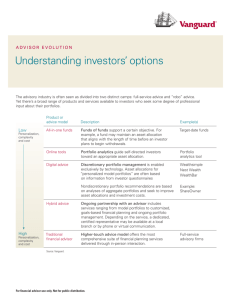

Investment Overview March 2013. ‘A timely reminder’ In both of the overviews completed so far in 2013 I have commented that even though the ‘growth’ we had experienced in the Investment markets was very welcome all the ‘nasties’ that had been impacting over the previous two years in most G8 Economies were still very prevalent and should not be ignored as they could come back into focus at any time. In the last couple of weeks this has been confirmed with continued budgetary problems in the US. Budget cuts, known as the ‘sequester’, that were drawn up two years ago take effect this year with reductions in the US Federal budget to the value of $85bn (£56bn). In the UK the recent budget speech confirmed that both Economic growth and Debt reduction will continue to create major problems for the UK Economy and the worse news of all is the resurrection of the Euro debt crises with Cyprus seeking a ‘bailout’ to stop the country going bankrupt. It is important to point out that none of these areas will ‘damage’ market confidence in the way the same negatives have done in the past. However, it will create a temporary pause in the growth of markets and ‘cool’ the investment opportunities that we have seen during January and February. I do not want to spend time in this overview looking at the ‘how’ and ‘why’ these negatives have emerged or are continuing. I believe it is more important to look at the consequences of what has occurred and how best, as Investors, we can continue to navigate through the ‘ups’ and ‘downs’ of the markets. One thing I feel should be pointed out is that the ‘Financial Collapse’ of 2008 that created the current recessionary pressures across the Global Economy is very unusual in terms of the frequency of it happening. In fact this was the first ‘global’ financial collapse in economic history therefore it is very difficult to analyse the way in which the Global economy will respond following such a major event. Historically, with ‘deep recessions’ (even global ones) you would start to see a ‘pick up’ in economies as Central Banks intervene with Quantitative Easing (QE) to manipulate growth. When growth is stimulated to a normal level QE will stop to reduce the effect of Inflation and normally the macro economies will function without any more intervention. You can look back at the UK’s history of dealing with recession on this basis and the only thing that is different in each case is the length of time it takes from falling into recession, coming out and moving back to a normal economic cycle. The current situation has shown how different a ‘financial collapse’ driven recession can be. Not only have we had to deal with unprecedented levels of ‘Central Bank Intervention’ we have also, had to deal with the impact of banking corporate debt on Government Finances. A number of peripheral nations in the Eurozone have had to seek bailouts in order to underpin their banking systems to prevent a banking collapse. With this additional QE and continued high levels of sovereign debt we know that future problems will arise from how this debt will be repaid along with the extra worry of inflation/deflation and possibly stagflation. The historical scenario that has similarities to all the negatives we have seen over the last five years is the economic position that Japan has faced over the last 12 years. Clearly the Japanese scenario was not a direct result of a banking failure however the way in which the economy has moved in terms of growth, debt levels, inflation/deflation, interest rates and gilt yields is very similar to how a lot of Economies have behaved since 2008. The only real difference is that Japan has been plagued by deflation within their economy right from the start of their problems whereas it seems most westernized economies will suffer inflationary pressures for the majority of the time that they are experiencing problems. I believe the other areas such as limited growth, high debt levels and low interest rates will mirror Japan’s experience. As it has taken them over 12 years to ‘break the shackles’ it is quite obvious that there will be no ‘quick fixes’ for the global economy and the pressures we are experiencing now will continue for some time to come. So how can an investor make sure they get the best from these markets if they are going to continue to be very volatile? Firstly, and most important, is that you need a portfolio that is actively managed and well diversified. Secondly, you need to understand the ‘Risk to Reward’ factor of what you are trying to achieve for your Investment and finally you need to understand the investment timelines that you are looking to achieve. Focusing on these areas individually, the first is already achieved by most Financial Advice Centre clients as they are in the Investment Review Service which automatically offers portfolios with maximum diversification and, for many clients, a very actively managed portfolio planning service. For me, as Investment Manager, I feel a lot more could be done for clients if the opportunity of a more actively managed position was taken. Since January, Financial Advice Centre Investment Services have been operating a ‘bespoke’ monthly managed portfolio service as part of their ‘menu of services’. For the months of January and February, where investment returns have been excellent across the board, you could look at this type of service and say “do I need to pay extra to get ‘marginally better returns’ when I am very happy with the returns I have got?”. In many circumstances this could be a correct assumption however, in reality, the returns achieved for the bespoke clients have not been ‘marginally’ better, they have been (on average across the risk rated areas) 1% better return over the quarter than the Standard Portfolios. This has been due to just a couple of portfolio changes that we have not instigated as yet into the Standard Portfolios. The real benefit of ‘Bespoke’ portfolio management will be seen over the coming months when we experience Investment Growth stagnation and market conditions become a lot more volatile. It is in these markets where growth can still be achieved from ‘niche’ areas and areas that may provide an investor with only a very short period to make a gain from the Investment. These will be times when short term management of opportunities will be key. (Please speak to your adviser regarding the ‘Bespoke Service’ and what it can offer you together with the additional costs involved or, if you wish, you can contact me direct on 0121-4477491). In connection with the second area - ‘Risk to Reward’ – it is very important for investors to review this on a regular basis. At Financial Advice Centre Ltd we do try to support this by offering clients a potential ‘benchmark’ return for each of the risk categories that we link to our portfolio management. Clearly ‘rewards’ are not the whole story and I feel it is more important for a client to understand ‘capacity for loss’ within the risk strategy they are taking. In both 2008 and 2011 we experienced losses in the portfolios despite them being well diversified and balanced. As an investor you must make sure that you balance your quest for growth against the risk you are taking for potential losses. For all clients there will be investment periods when losses occur, however the actively managed, well diversified portfolios will control these during the period of loss and then allow you to be in a position to benefit from the upturn in markets when it occurs. The level of losses will be affected by the level of ‘risk’ you have taken for that investment, clearly the higher the risk taken the higher the potential loss position will be however, as covered above, the loss position can be absorbed when market conditions improve. An example of this can be seen during the period August to November 2008 when our current cautious portfolio would have lost approx. 18.7% in that period - a very heavy loss for a cautious client. If this client remained in the same portfolio for another 9 months they would have achieved 10.9% gain in quarter two of 2009 and a further 14.7% gain in quarter three of 2009 effectively absorbing all the losses they had occurred and making a small gain. It is, therefore, ‘key’ for a client to understand the risk they are taking for the potential rewards that could be gained and accept that for a number of years their investment returns will be volatile and over a short period of time there could be a real potential for loss as well as a real potential for gain. This leads nicely into the third area - the timeline for an investment that is determined by the investor but needs to be controlled by the Investment Manager. Many clients when they invest monies will not have any idea when they may wish to access some, or all, of this money. For certain investments like Pensions it is a little easier to understand the time scales for the investment as there is a minimum age before you can access benefits, however nearly all other investments do not have a product driven timeframe to work from. If you take the example in the previous paragraph of the losses and then gains achieved in a short period of time an investor who is not looking to access the money in that period of time should be ‘ok’. The only negative for those individuals is the loss of time which can be made up over subsequent months and years. The real losers in that period would have been investors who needed to access the money and they would have experienced a large crystalized loss. So how can this be managed? For most individuals who had to withdraw monies in a certain period of time they would (normally) have prior knowledge of knowing they needed access to the money. For these people, even for the lower risk levels, this knowledge is very important as the market situation can be assessed at a date prior to monies being required and, if necessary, a ‘no risk strategy’ employed for the investment, locking in gains that clients have made and ensuring that no loss/or a minimum amount of loss was taken by the investment. So for all investors I recommend that for any monies held, whether it is a ‘cash account’ at your bank or in a daily priced investment vehicle, that you review, on a regular basis, the potential timescale for that investment. You could be holding an investment in a cash area that is providing very little return for a long period of time before it was accessed therefore seriously reducing the opportunities for returns. Conversely you could be holding monies in investment areas that could move quickly and sharply into negative areas at a time when you need to access that money quickly. (Please contact your adviser or phone me direct on 0121 4477491 if you need any assistance with timelines). Finally, as we are at the end of the 1st Quarter 2013 I will provide a brief overview of the key investment sectors against the in-depth review I provided for each sector in my December 2012 overview. (If you wish to have a copy of this overview please email on investments@face-uk.com) 1) Cash- Continuation of low interest rates and banks being forced to ‘shore up’ their reserves will mean that shorter term deposits will become very unattractive to savers and certainly those looking at supporting income will find it a lot harder to achieve the returns they seek. The main area for cash returns will come from structured deposits which will now open up as banks look to other areas to secure monies for their balance sheets rather than borrowing through the Bank of England’s liquidity scheme. Coupons on these particular products are attractive and offer a very sensible alternative to clients shorter term cash objectives. 2) UK Gilts and Sovereign Debt- Yields on most major sovereigns remain reasonably attractive especially on a shorter duration basis. Despite the UK downgrade from ‘AAA’ and the recent ‘opening up’ of the Euro crises, yields in selected areas (US, UK and Germany) will continue to remain low. However, we will see spreads rise against some of the peripheral nations of Europe (including Italy) where yields will continue to remain at rates that offer no real comfort in the short or longer term. An example of this can be seen in Italian 10 year yields that have risen from 4.27% (2nd January) to 4.78% (27thMarch). I do see yields across all areas moving upwards as we go through the year however at this time they still remain reasonably attractive. One area that I feel will continue to offer a good opportunity to investors is the Index Linked Gilts (both UK and Globally). As indicated above I do believe that this year’s conventional gilt yields on, Bunds and US Bonds will increase, however, for Index Linked gilts we expect to see a continued fall. As with conventional gilts ‘Duration’ will be the key area for investors in the index linked area. 3) Bonds- We have certainly seen a very different corporate and high yield bond market in the early stages of 2013 compared to 2012. I do not think that the ‘bubble has burst’ in the bond market, however, what we are experiencing now is a correction in both yields and price. Once this mini correction has run it’s course I feel that both corporate and high yield bonds will provide investors with a ‘normal return’ opportunity from the respective areas although not the ‘double digit’ returns we have seen over the past 12 months. As with conventional gilts an area of opportunity (even though it is very limited in terms of funds available) is through inflation linked bonds and short duration index linked corporate bond funds that we believe will provide an attractive return for investors alongside their conventional counterparts. 4) UK Equities- Continues to be a mixed bag of opportunities. As indicated in December, Small and Micro Cap are the areas that are offering clients the best opportunities via both growth and dividends. In connection with dividends I feel, over the next few months, we will see big move backwards by a number of senior players in the markets. A large number of ‘defensive stocks’ have come under significant pressure lately in terms of holding dividends at current levels. Aviva have already announced a significant cut in their dividends and I would not be surprised to see the same situation occurring at companies like AstraZeneca and Glaxo SmithKline. Along with the potential damages that BP will be forced to pay following the start of the Deepwater Horizon lawsuit a large chunk of the Dividend activity coming from the UK FTSE 100 is under threat. I believe this threat will start to manifest itself in the UK Equity income sector where a large number of fund managers have relied on the corporations that I feel will come under threat. This will have a quite serious impact in this area and on investor returns. 5) European Equities- Despite the fall seen in the last couple of weeks the European equity market has been one of the top performers since the start of the year, carrying on from where it left off in the final 3 to 4 months of 2012. I still feel many stocks in Europe are undervalued and therefore offer ‘quality fund managers’ a real opportunity to make good returns for their funds. As with the UK, dividend activity in this area will also be key to returns so Income funds will feature across most of the medium to higher risk portfolios. With Europe there continues to be a downside from the point of Market sentiment. The reason why European valuations are ‘cheap’ at the moment is because investor sentiment has created it. At the first sign of any trouble in Europe investors seem to ‘run to the hills’ so holding European funds has a volatility warning that reads ‘please wear your tin helmet at all times’. 6) American Equities- As pointed out in December, this area continues to offer best value on a risk to reward basis for investors. Now that the ‘fiscal cliff’ situation is in a position where it can be worked through over the remaining term of Presidents Obama time in office we should see the world’s largest economy continuing to move out of the recessionary pressures that have burdened the world economy over the last five years - showing the rest of the world the ‘right way’ of doing things. This area will form a large part of the total equity content of my portfolios. 7) Japan- I hold my hands up, I got this area totally wrong in my summary of December 2012. At that stage I called it the ‘basket case of all basket cases’. Well how wrong can I be! Within a month of making that statement I was offering a route into Japan for all the ‘bespoke clients due to the complete reversal of Government policy targeting External growth via a ‘devaluation of the Yen’ (some like the US say by underhand measures). Along with Internal monetary policy decisions that are clearly inflationary and are already driving inflation into the Japanese economy for the first time in over 12 years. I now see Japan, like America, being a vital part of the portfolio management. 8) Emerging Market & Asian EX Japan Equities- I am very much undecided about the Risk to Rewards of this sector. Even though many economies in this area are immune to the Westernized Financial Problems of 2008, they have been caught up in their own individual economic negatives which are based around growth and Inflation. Add into this Political and Corporate Issues clients in Financial Advice Centre can understand my reluctance to get heavily involved in this sector. I do believe in the benefits that this area can bring to a portfolio but my worry is at what cost. So at this stage it will be a sector which has limited exposure mainly around the Income sector with a view to support the ‘bespoke portfolios’ if an area shows real promise going forward. 9) Alternative Investment Areas- As stated in December, as a diversification tool this area is going to be key going forward. We have already started to introduce daily priced funds from this sector into portfolios supporting the work that we have done with some clients during 2011 and 2012 in the structured product area. This is an area that can support clients’ investments from funds that offer 100% guarantees to areas such as Venture Capitalist Trusts (VCT) where the Managers of the funds invest into companies on the Aims Markets, etc which is at the highest level of the risk spectrum. Also they offer excellent tax breaks for many investors as well as potentially good investment returns. This area is, and will be, very explored and researched during 2013 so watch this space. In conclusion, as an investor you should not get ‘carried away’ with the returns that we have seen over the first quarter of 2013, however, you do not have to retreat into a bunker with your ‘Tin Helmet’ on either as the markets do seem to have shown a resilience and understanding of what the global economy is experiencing and will continue to experience. Active Management and Diversification will be key along with a client’s understanding of the risk they are taking to the rewards on offer. If we, as your Investment Managers, and you, as investors, get this right then 2013 and beyond could be very rewarding. Ian Jackson Investment Manager (Sources- O&M Investment Cautious factsheet- M&G Inflation Overview Jan 2013Investec Weekly Digest and Bloomberg.)