note4

advertisement

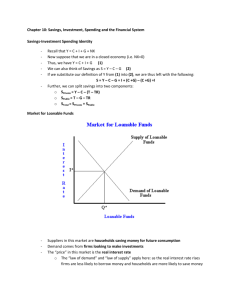

1 CHAPTER FOUR THE LEVEL OF INTEREST RTAE What are the factors that establish the level of interest rates in the economy and cause it to change? What is the effect of inflation on the level of interest rates and how investors and financial institutions forecast interest rate movements. But first what are interest rates? WHAT ARE INTEREST RATES? Interest rates are the price of borrowing money for the use of its purchasing power. (It is a rental price of money). To borrowers, interest is the penalty paid for consuming income before it is earned. To lenders, interest is the reward for postponing (delaying) current consumption until the maturity of the loan. Like other prices, interest rates serve an allocative function in the economy. They allocate funds between surplus spending units (SSUs) and deficit spending units (DSUs) and between financial markets. For SSUs, the higher the rate of interest, the greater the reward for delaying current consumption and thus the greater the amount of savings in the economy. For DSUs the higher the yield (interest rate) paid on a particular security, the higher the cost of money. Thus, SSUs want to buy financial claims with the higher returns whereas DSUs want to sell financial claims at the lowest possible interest rate. So how interest rates are determined? THE REAL RATE OF INTEREST Interest rate depends on tow things: 1- The rate of return on investment: the higher the return on investment, the more likely producers are to undertake a particular investment project. 2- The time preference between current and future consumption: most people prefer to consume goods today rather than tomorrow. This is known as the positive time preference for consumption. Investment is negatively related to interest rate. That is, other things remaining equal, the higher the interest rate the lower the investment (because cost of borrowing increase if interest rate increase). Saving is positively related to the interest rate. That is, other things remaining equal, the higher the interest rate, the higher the savings are. This relationship gives: Downward sloping demand curve for desired investment, and Upward sloping supply curve of desired saving. The interaction of these two determine the rate if interest as shown in the figure below: The two curves show that consumers will save more if producers offer higher interest rates on savings, and producers will borrow more if consumers will accept lower return on their savings. The market equilibrium rate of interest (r*) is achieved when desired saving (s*) by savers equals desired investment (I*) by producers across all economic units. This equilibrium rate of interest is called the real rate of interest. The real rate of interest is the fundamental long-run interest rate in the economy. It is called the "real" rate of interest because it is determined by the real output of the economy. 1 2 Interest rate Desired Savings (DS) r* Desired Investments (DI) Saving & investment * * S =I THE LOANABLE FUNDS THEORY & INTEREST RATES: As noted above, the real interest rate is a long-run interest rate, so what determine interest rate in the short-run. The loanable funds theory is a framework used to determine interest rate in the short-run. According to this the interest rate is determine by the demand for and supply of direct and indirect financial claims on the primary and secondary markets during a given time period. The need to sell financial claims represents the demand for loanable funds. Buying of financial claims to earn interest represent the supply of lonable fund.. In general: Increases in interest rate will stimulate (motivate) more saving and increase supply of loanable funds. So, the loanable fund supply curve slopes upward. That is, there is a positive relationship between interest rate and supply of loanable funds. Demand for loanable funds decreases as the interest rate increases (due to increase in cost of borrowing). That is, there is a negative relationship between interest rate and demand for loanable funds. So that demand for loanable funds curve slopes downward. The intersection of supply and demand for loanable funds determines the equilibrium interest rate and the equilibrium quantity of loanable funds loaned out and demanded. Changes in interest rate, brings changes in quantity demanded and supplied of loanable funds, and is represented by a movement along SL and DL curve. Therefore: If interest rate is at r1 (below equilibrium), shortage of loanable funds exist, which force the interest up. And If interest rate is at r2 (above equilibrium), surplus of loanable funds exist, which force the interest rate down. 2 3 Interest rate SL r2 r0 r1 DL Loanable funds Q0 Changes in factors other than interest rate, changes the supply and demand for loanable funds. That is, SL and/or DL curves shift upwards or downwards, and as a result a new equilibrium occurs. What are the factors other than the interest rate? FACTORS AFFECTING SUPPLY OF LOANABLE FUNDS 1- CHANGES IN THE QUANTITY OF MONEY: If quantity of money increases (Δ M is +), supply of loanable funds increases (people have more money to save), the SL curve shifts to the right (or downwards), resulting in a new equilibrium with lower interest rate and higher equilibrium quantity. 2- CHANGE IN THE INCOME TAX: A decrease in income tax increase saving. Thus, the supply of loanable funds increases, shifting the SL curve to the right, decreasing r0 and increasing Q0. 3- CHANGES IN GOVERNMENT BUDGET FROM DEFICIT TO SURPLUS POSITION: Reduced government expenditure increases government savings, thus shifts the SL curve to the right. 4- EXPECTED INFLATION: If lower rates of inflation are expected in the future, saving increase (current consumption decreases waiting for the expected reduction in prices), and supply of loanable fund will increases, which shift the SL curve to the right. 5- CHANGE IN SAVING RATE or public desire to hold money balances: An increase in saving rate (the percentage of income saved) will increase the supply of loanable funds, shifting the SL curve shift to the right. 6- CHANGES IN BUSINESS SAVING: An increase in business saving of course increases supply of loanable funds and SL curve shift to the right. FACTORS AFFECTING DEMAND FOR LOANABLE FUNDS 1- CHANGES IN FUTURE EXPECTED PROFITS OR BUSINESS ACTIVITIES: If business expected higher profit in the future demand for investment or investment demand increase, and so does demand loanable funds, DL curve shifts to the right (or upwards), resulting in a new equilibrium with higher interest rate and higher equilibrium quantity. 2- CHANGES IN GOVERNMENT BUDGET FROM SURPLUS TO DEFICIT POSITION: Increase in government expenditure, increases government borrowing to cover its deficit, therefore the demand for loanable funds increases, and the DL curve shifts to the right. 3 4 3- CHANGES IN TAX: A decrease in tax, increase government deficit (since government revenue decreases), and thus increases the demand for loanable funds, and DL curve will shift to the right. In summary, If SL only increases, Q0 will increase and r0 decreases. If DL only increases, Q0 will increase and r0 will increase. If both SL and DL increases, Q0 will increase r0 might increase, decrease, or remain unchanged. SOURCES OF DEMAND AND SUPPLY OF LOANABLE FUNDS: SOURCE OF SUPPLY LOANABLE FUNDS: - Consumer savings. - Business savings - Government savings - Central bank, changing quantity of money. SOURSE OF DEMAND LONABLE FUNDS: - Business investment. - Consumer credit purchase. - Government budget deficit. PRICE EXPECTATIONS AND INTEREST RATE Changes in price affect both: - Realized return that lender receive on their loans, and - Cost that borrowers must pay for them. If price increase: purchasing power decreases, and borrowers will repay lender in inflated dollars (dollars with less purchasing power) lender will loose (they are paid in less purchasing power money). Borrowers will benefit (they pay in less purchasing power). Opposite will happen if price decreases. How to protect against price changes? To protect against price changes, inflation is incorporated in the interest rate on a loan contract. Suppose SSU and DSU plan to exchange money and financial claims for a period of one year. Both agreed that a fair rental price for the money is 4 percent and both anticipate an 8 percent inflation rate of the year. Then what would be the contract rate on the loan? To answer this question we need to introduce the Fisher effect. THE FISHER EFFECT Inflation is incorporated through the fisher effect theory, which states that the nominal interest rate (contract rate) includes real interest rate and expected annual inflation rate. The contract rate is determined from the Fisher equation, which states that: (1 + i) = (1+r)(1+ΔPe) ---------------(1) Where i = the nominal rate of interest (the contract, observed, or market rate) r = real rate of interest in the absence of price level changes ΔPe = expected annual change in commodity prices (expected inflation) Solving the Fisher equation for i, we get the following equation: i = r + ΔPe + (rΔPe) ---------------(2) 4 5 This equation shows the relationship between nominal (contract) rates and rates of expected inflation. The inflation component of the equation (ΔPe + (rΔPe) is commonly referred to as to fisher effect. It is named after economist Irving Fisher, who is credited with first developing the concept. Returning to the loan example, the contract rate is: i = 0.04 + 0.08 + (0.04 X 0.08) = .1232, or 12.32% The final term of the Fisher equation (rΔPe) is approximately equal to zero. So in many situations it is dropped from the equation without creating a critical error. The equation without the final term is referred to as the approximate Fisher equation and is stated as follows: i = r + ΔPe Therefore, approximately i = 4% + 8% = 12% Note that the equation can be used to calculate any of the unknowns if we know the other two: Time period Real rate 0 1 2 3 4 5 6 5 5 5 5 5 5 5 Expected price change 0 7 7 9 3 -2 -7 Approximate Nominal rate 5 12 12 14 8 3 0 Exact Nominal rate 5.00 12.35 12.35 14.45 8.15 2.90 0 Notes that ΔPe is the percentage rate of price level change and not the level of prices. The above exhibit illustrates the importance of this statement. Suppose the real of interest rate was 5 percent and inflation increased from zero to 7 percent. The nominal rate of interest thus went from 5 to 12.35 percent. For the next time period, what happen to nominal rate of interest if prices are expected to continue to rise at 7 percent annually? The nominal rate stays at 12.35 percent. This is because in each period new loans are made with money already protected against past changes in purchasing power. However if the expected annual inflation rate accelerates from 7 to 9 percent, the nominal interest rate will jamb to 14.45 percent for all new loans. Thus the nominal interest rate will become greater only if the rate of price-level increases become greater. Finally if price begins to fall (deflation), the nominal rate will be below the real rate by the amount of the expected rate of price decline. Thus if prices are expected to decline 2 percent annually, the nominal rate in our example will be 2.90 percent. However the nominal rate cannot decline below zero regardless of the rate of price decline. Lender would always prefer to retain their money and purchase goods and services rather than to pay someone else (negative interest) to do the same. The nominal rate of interest is directly influenced by changes in the expected rate of inflation. That is the higher the expected rate of inflation, the higher the nominal rate of interest. THE REALIZED REAL RATE Actual inflation could be different from expected inflation rate. This may lead to the realized rate of return on a loan could be different from nominal interest rate agreed at the time of the loan contract. Realized real rate is calculated using this formula: r = i - ΔPa Where: r = is the realized real rate of return. ΔPa = is the actual rate of inflation. i = is nominal interest rate. 5 6 Example: If real rate of interest (r) = 4% Expected annual inflation rate (ΔPe) = 8% So, nominal rate (i) = 4% + 8% = 12% If actual inflation rate (ΔPa) was 5% Then the realized rate of return is: r = i+ ΔPa = 12% - 5% = 7% If actual inflation rate was 2% r = 12% - 2% = 10% If actual inflation rate (Δpe) was 15% then, r = 12% - 15% = -3% So, realized rate of return can be negative. INFLATION AND LOANABLE FUNDS MODEL The loanable funds theory can be used to illustrate inflation’s effect on financial markets. The higher the expected inflation rate, the higher is the demand for loanable funds (present consumption increase), so the DL will shift upward (to the right) by the amount Δpe. The shift from DL0 to DL1 implies that borrowers are willing to pay the inflation premium of Δpe. Similarly, the higher the expected inflation rate, the lower is supply for loanable funds (saving decrease), so the SL will shift upward (to the left) by the amount Δpe. The shift from SL0 to SL1 will be such that lenders are given a higher nominal yield to compensate for their loss of purchasing power. The net effect is that the market rate of interest will rise from r to i, where the different between i and r is the expected inflation rate (Δpe). Even though the real rate of interest (r) remains unchanged, the nominal rate of interest (i) has adjusted fully for the anticipated rate of inflation (Δpe), and the quantity of loanable funds in the market has remained the same at Q0. IR SL1 SL0 i Pe r DL1 DL0 LF 6 7 INTEREST RATE MOVEMENTS AND INFLATION Interest rate vary directly with inflation rate, and directly with the level of economic activities, (recall that i= r + ΔPe , so any change in r or ΔPe will change r directly). Generally. short-term interest rates are more responsive to changes in expected inflation than longterm interest rate. Inflation rate is for the life of the loan contract. The effect of a change in inflation would be more felt in short periods than in long periods. Thus, a monthly change in the rate of inflation would have a large affect on the expectation across a three-month contract while it would have a small effect across a ten-years contract. FORCASTING INTEREST RATES Since interest rate affect the price or return on a financial asset, there is keen interest from investors and financial institutions to forecast the movement of interest rates. To protect against changes in interest rate (interest rate risk), investors and managers use two approaches: 1- Hedge interest rate risk (using hedging contract) Hedging means taking an action to reduce or eliminate interest rate risk, e.g. using contract to guarantee future prices, like future, forward, or options contracts. 2- Forecasting interest rate movements: Two main approaches are used to forecast interest rate: - Economic models - Flow of funds accounting approach ECONOMIC MODELS Here interest rate is forecasted by estimating the statistical relationship between measures of economic output (main economic indicators) and interest rate. These models vary from a simple single equation models to complex simultaneous equation model. The economic variables are entered into different models and interest rate is forecasted. FLOW-OF-FUNDS ACCOUNT FORCASTING Here the framework of loanable funds theory is used to forecast interest rate. The flow-of-funds data show the movement of savings----the sources and uses of funds---through the economy in a structures and comprehensive manner. The data used therefore is the flow of funds accounts rather than the national income account. Interest rate is forecasted after projecting supply and demand for loanable funds. This is based on estimating factors, which affect the SL and DL, like changes in money supply (monetary policy), fiscal policy, expected inflation, and other economic activities. 7