Accounting 101 – Bank Reconciliation

advertisement

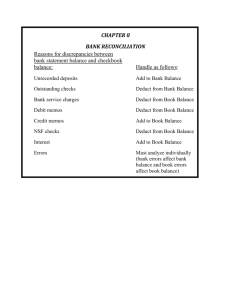

Accounting 101 – Bank Reconciliation Learn how to perform a bank reconciliation to ensure the check register balance. The bank reconciliation is an important part of good basic cash management practices. Cash Asset Management and Bank Reconciliation The bank reconciliation ensures the accuracy of the cash general ledger account. Just like performing a physical inventory count ensures the accuracy of the inventory, balancing the check register ensures that the cash account is correct. The bank reconciliation is normally performed once a month, usually when the bank statement is received. There are many cash transaction errors that can occur during the course of daily business activities. Some of the common errors may include: • Lost checks • Cash receipts errors • Deposit errors • Insufficient funds for deposited checks • Bank transaction errors • Interest earned errors • Bank fees Bank Reconciliation – Adjusting the Bank Statement There are basically four items that’s needed to adjust the checkbook register, a calculator, pen or pencil and the monthly checking account bank statement. Compare the checking account bank statement with the check register. Insure that all the transactions are correct and agree with the figures in the check register. Look for bank errors or any other inappropriate transactions. 1. List the ending balance on the bank statement 2. Add deposits recent deposits not listed on the bank statement 3. Deduct outstanding checks not recorded on the bank statement 4. Add or deduct any bank errors Bank Reconciliation – Adjusting the Cash General Ledger Once the bank statement is adjusted, the next step is to adjust the cash general ledger. The cash account needs to be adjusted at this point to reflect the true amount. The following will be actual adjustments made with a journal entry to the cash account. 1. Deduct bank service charges and fees 2. Add interest earned or any other income not recorded to the cash GL 3. Add or deduct errors in the cash GL account. The above transactions will be recorded as debit or credit to the cash account, usually performed through the general journal. A debit (add) is recorded as an increase to cash and a credit (deduct) is recorded as a decrease to cash. For each journal entry a reciprocal (debit or credit) must be recorded. For example a debit to cash and a credit to interest earned. After the adjustments are made to the bank statement and the cash account, both ending balances should be equal. If the two do not equal, further analysis will be required to pinpoint the error(s). How to Remember Debits & Credits Instructions • Step 1 Listen to the sound of the word. Debit sounds like debt, something you have to pay. 2 Associate the word debit with a debit card. Debit cards always take money out of your account. Step 3 Think about how the word makes you feel. Credit is a good thing. In sports, think of “who got credit • Step • for the winning score?” • Step 4 Associate the first letter of the word debit with another word that has the same first letter. Debit starts with D, which stands for “Decrease” and “Deduct from your account.” Step 5 Associate the first letter of the word credit with another word that has the same first letter. Credit starts with C, which stands for “Come to me” and “Cultivate (grow) your money.”