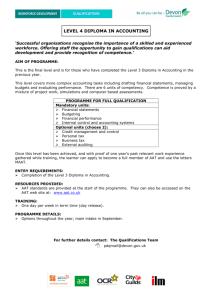

Expenses Allowable in Accounts of Small Businesses

advertisement

AAT RESPONSE TO THE HMRC CONSULTATION ON “TACKLING MARKETED TAX AVOIDANCE” 1 2 EXECUTIVE SUMMARY 1.1 The Association of Accounting Technicians (AAT) is pleased to comment on the issues raised in the HMRC consultation document (condoc) on “Tackling Marketed Tax Avoidance”. 1.2 AAT responded to HMRC’s 2013 consultation “Raising the Stakes on Tax Avoidance” and was interested in the Summary of Responses published by HMRC in January 2014. 1.3 AAT supports the principle of tackling tax evasion and aggressive and contrived tax avoidance schemes, to that extent we support the Government’s action to tackle tax avoidance by changing the economics of devising and entering into tax avoidance schemes (para 4.8). 1.4 However, for the sake of clarity and certainty, we also consider that proposed legislation should be restricted to marketed tax avoidance cases (para 3.2) disclosed under DOTAS and the most egregious GAAR cases. 1.5 AAT is concerned by the potential for “mission creep” (paras 3.3 & 3.4) as introduced by para 3.1 of the draft legislation where it enables the Treasury to bring other taxes into scope by statutory instrument. 1.6 AAT is concerned by the retrospective effect of the proposal concerning the payment notice in para 4.12 (condoc), whereby the proposed legislation will seek to apply to existing schemes registered under DOTAS, on the basis that tax legislation which introduces retrospectivity is, in principle, unfair on taxpayers who were following the law as it stood at the time of their action. VESTED INTERESTS 2.1 3 AAT is responding to this consultation from the wider public benefit perspective of achieving sound and effective administration of taxes. GENERAL OVERVIEW 3.1 AAT endorses the Government’s commitment to tackle tax avoidance by changing the economics of devising and entering into tax avoidance schemes (para 1.1 (condoc)) and AAT shares HMRCs view that “there is no inherent presumption that the tax should remain with the taxpayer during a dispute” para 1.3 (condoc). 3.2 However, we also consider that the proposed legislation should be restricted to marketed avoidance cases and not affect other enquiries where HMRC may not share the appellant’s view on a point of law or procedure. The decision in the Upper Tier Tribunal of HMRC v Anthony Bosher FTC/3/2013 illustrates the restrictions to taxpayer appeal, even when the First Tier Tribunal considers that penalties imposed by HMRC are disproportionate and excessive. 3.3 Over the years Parliament has introduced via legislation a multiplicity of incentives and investment opportunities which carry tax reliefs which, when appropriate, a tax agent will be obliged to explain to their client(s). In such instances such advice should be directly appropriate to the client and made as “marketed tax avoidance”. We are concerned that if the proposed legislation is not correctly drafted from the outset HMRC might seek to challenge such advice using the proposed legislation. 3.4 Marketed tax avoidance schemes should all, by law, have a DOTAS number. The distinction in para 4.2 (condoc) between, on the one hand, DOTAS/ GAAR cases and other cases suggests possible ‘mission creep’ of the process to non marketed cases which HMRC considers to be tax avoidance. This is a concern to AAT. 3.5 We believe that at paras 4.45 and 4.54 of our response to “Raising the Stakes on Tax Avoidance”1 pointed to existing legislation which enabled HMRC to challenge the economics of allowing tax to be held over after a similar judicial decision had been established in HMRC’s favour. 3.6 Para 5.10 (condoc) “Raising the Stakes on Tax Avoidance” indicated that “At present, the proposal is that these requirements should apply only in relation to direct taxes, including Stamp Duty Land Tax” and the responses given were restricted to that question. Sch. 10 of the Finance Act 2003 sets out the administrative legislation for Stamp Duty Land Tax and which follows the format of the Self Assessment legislation in Taxes Management Act 1970. AAT’s proposal was to use current legislation more effectively to avoid additional layers of legislation. 3.7 As regards VAT, section 84(3A) of VATA 1994 requires an appellant to pay the VAT upfront before an appeal is entertained. 3.8 AAT is aware that the Government announced in their 2013 Autumn Statement its intention to enlarge the scope of taxes under this consultation to cover all the various taxes and charges listed in the Draft Legislation at Schedule 1, Section 1, paragraph 2. AAT is also aware of the Government’s announced intention to put in place a requirement for users of tax avoidance schemes to settle their disputes on receipt of a notice (a ‘follower notice’) para 3.1 (condoc). 3.9 AAT accepts that it makes sense to draw together the different legislation of the various taxes and charges into a common legislative structure for anti tax avoidance purposes. A copy of the AAT response to “Raising the Stakes on Tax Avoidance” can be downloaded from the AAT website at http://www.aat.org.uk/about-aat/aat-policy-work 1 4 TACKLING MARKETED TAX AVOIDANCE; AAT’S RESPONSE TO THE CONSULTATION QUESTIONS Q1: Do you agree with the proposals for the timing and issue of payment notices? 4.1 As stated in para 3.8, AAT accepts that the proposal for a ‘follower notice’ enables a common legislative structure to cover the assorted taxes and charges listed at Schedule 1, Section 1, paragraph 2 of the draft legislation published at Annex A of the condoc, to require users of tax avoidance schemes to settle their disputes on the premise that their case is on the same, or substantially similar, grounds as a case already decided in the tribunal or court; and for payment of the tax in dispute where a taxpayer who has received a ‘follower notice’ chooses not to settle the dispute on receipt of the notice. 4.2 AAT considers that the proposed 90 day response time is sufficient for taxpayers to consult their adviser, liquidate funds which may be tied up, for example in securities, and AAT agrees with the proposal at 3.12 of condoc. that the 'accelerated payment' would become due on the expiry of that time limit, or the extended period where the taxpayer asks for a review of the ‘follower notice’. 4.3 AAT agrees that the issue of a payment notice is common practice for tax demands. Q2. Do you agree with this proposed method for establishing the payment amount? 4.4 AAT agrees that the use of ‘the normal rule’ as defined at paragraph 10 (1) of Schedule 1 of the proposed legislation is appropriate: “for the purposes of calculating penalties under paragraph 9, the value of the denied advantage is the additional amount due or payable in respect of tax as a result of counteracting the denied advantage” Recalculation of the additional tax due on the return to remove the effects of the avoidance scheme is an eminently sensible method for establishing the payment amount. Q3: Do you agree with these grounds for objection to an accelerated payment notice? 4.5 AAT considers that the grounds for challenge proposed by HMRC ‘for example, has the notice been sent to the wrong person’ para 3.24 (condoc) are too narrow, especially in non DOTAS cases. Q4: Should there be any additional grounds for objection to an accelerated payment notice? 4.6 Current legislation provides for the taxpayer to apply for postponement of tax under section 55(3) of TMA 1970 where an appeal has been made against a revenue assessment. Where HMRC issues a ‘follower notice’ in a non DOTAS case AAT considers that the taxpayer should have the opportunity to apply for postponement of the tax where he/she is able to distinguish their case from HMRC’s decided failed case, especially where that case is not on ‘all fours’ with the appellant’s case. Q5: Do you agree that accelerated payments for cases under appeal should be handled by way of adapting the existing rules for postponed tax in TMA 1970? 4.7 AAT does not accept that the existing rules for postponement in TMA 1970 should be adapted for direct tax cases. 4.8 As previously stated at 3.5, we explained in our response to the consultation “Raising the Stakes on Tax Avoidance” (para 4.45 and 4.54), that existing legislation enabled HMRC to challenge the economics of allowing tax to be held over after a similar judicial decision had been established in HMRC’s favour. 4.9 As stated at 3.7 above, section 84(3A) of VATA 1994 requires an appellant to pay the VAT upfront before an appeal is entertained. 4.10 As acknowledged at paragraph 3.9 above, changes may be needed in respect to other taxes and charges to conform the different legislation of the various taxes and charges into a common legislative structure for anti tax avoidance purposes. Q6: Do you agree with this proposed approach to interest on unpaid and repaid amounts in relation to accelerated payments? 4.11 AAT agrees with the proposed approach to interest on unpaid and repaid amounts in relation to accelerated payments. Q7: Do you agree that the accelerated payment should be subject to a late payment penalty and the proposed amounts are reasonable and proportionate? 4.12 AAT accepts that it is reasonable that late penalty provisions should apply on a basis and rates similar to Schedule 56 of FA 2009. Q8: Do you agree to this treatment for payment of tax for cases in litigation? 4.13 AAT notes that “the Government does not propose to change the requirement to pay or repay tax in line with the judicial decision” and AAT accepts that this should apply to accelerated payments. Q9: Do you have any further comments on the principles or application of the proposal to issue accelerated payment notices in cases where a ‘follower notice’ is issued? 4.14 AAT offers no further comments to those expressed above. Q10: Do you have any comments about how information may be provided in such a way as to provide a reasonable balance between providing early certainty for taxpayers and not opening up a route to assist the development of future avoidance schemes? 4.15 Where arrangements disclosed under DOTAS do not involve any additional tax liability (as described in para 4.11 (condoc)) providing clearance to the taxpayer would not provide an opportunity of the type envisaged in para 4.14 (condoc), because there would be an absence of tax advantage. 4.16 On the other hand, it is reasonable to advise the taxpayer as early as possible of any impending charge. Any new schemes would require separate notification to HMRC under DOTAS. Q11: Do you agree that the proposed time limit for payment of an accelerated payment as a result of a DOTAS scheme should be the same as for accelerated payments linked to a ‘follower’ notice? 4.17 AAT supports the Government preference for the first option outlined in para 4.15 (condoc) - that the proposed time limit for payment of an accelerated payment as a result of a DOTAS scheme should be the same as for accelerated payments linked to a ‘follower’ notice – for the reasons outlined at para 4.16 (condoc) (namely that the reduction of potential complexity and that common payment timescales will help to remove unnecessary disputes about which criterion has been applied). Q12: Do you have any further comments about the proposed extension of this measure to cases involving schemes disclosed under DOTAS? 4.18 In paragraph 3.1 above we expressed the view that this consultation was to counteract tax advantage gained through entering into a marketed tax avoidance scheme so that there is no inherent presumption that the tax should remain with the taxpayer during the dispute. By law, all marketed tax avoidance schemes should have a DOTAS SRN which should be entered on the taxpayer’s tax return. Failure to do so should be challenged with the relevant penalties. However, the further link to DOTAS would seem to indicate HMRC’s intention to extend the ‘follower notice’ scheme to enquiries outside the scope of marketed tax avoidance cases, which is a concern for AAT. Q13: Do you agree that the scheme being challenged under the GAAR should be a criterion for issuing an accelerated payment notice? 4.19 AAT considers that due process should apply. There is a statutory process for GAAR schemes under Part 5 of FA 2013. AAT agrees that a scheme being challenged under GAAR should be a criterion for issuing an accelerated notice but only after the Advisory Panel has given guidance in HMRC’s favour or alternatively HMRC has obtained a judicial ruling. Q14: Do you agree with the timing proposal for the issue of an accelerated payment notice in a case being challenged by the GAAR? 4.20 AAT agrees that HMRC should issue the Payment Notice when HMRC decides to proceed to counteraction after receiving a GAAR Advisory Panel opinion on the arrangements. Q15: Do you have any further comments about the application of the policy to schemes that are challenged under the GAAR? 4.21 AAT fully supports HMRC’s actions to counteract tax arrangements that have been considered aggressive and abusive by the Advisory Panel. 5 6 2 CONCLUSIONS 5.1 AAT is supportive of the Government’s commitment to tackle tax avoidance by changing the economics of devising and entering into tax avoidance schemes (para 4.8). 5.2 We also share and recognise HMRC’s view that there is no inherent presumption that the tax should remain with the taxpayer during a dispute. However, AAT does consider that proposed legislation should be restricted to marketed avoidance cases (para 3.2) and not affect other enquiries where HMRC may not share the appellant’s view on a point of law or procedure. 5.3 AAT acknowledges and endorses the progress being made towards countering tax avoidance by HMRC and the success over the past two years outlined in para 2.2 and 2.3 (condoc), in halving the number of disclosed schemes from116 to 56 coupled with the fact that marketed Stamp Duty Land Tax (SDLT) schemes have almost disappeared from the market. 5.4 It is a fundamental aspect of any legal system that the citizen should be entitled to certainty on the law at any given point in time. Taking this in account we do not believe that the introduction of legislation with an element of retrospection is acceptable (see also 1.6), except where it merely seeks to back date a change to a day on which a Government announcement was made forewarning taxpayers that a change would be introduced in future legislation. ABOUT AAT 6.1 AAT is a professional accountancy body which has 50,000 full and fellow members and 80,000 student and affiliate members worldwide. Of the full and fellow members, there are 3,900 Members in Practice (MIPs) who provide accountancy and taxation services to individuals, not-for-profit organisations and the full range of business types2. 6.2 AAT is a registered charity whose objectives are to advance public education and promote the study of the practice, theory and techniques of accountancy and the prevention of crime and promotion of the sound administration of the law. 6.3 In pursuance of these objectives AAT provides a membership body. We are participating in this consultation not only on behalf of our membership, but also from the wider public benefit perspective of achieving sound and effective administration of taxes. Figures correct as at 31 December 2013 If you have any questions or would like to consult further on this issue then please contact the AAT at: email: consultation@aat.org.uk and aat@palmerco.co.uk telephone: 020 7397 3088 FAO Aleem Islan Association of Accounting Technicians 140 Aldersgate Street London EC1A 4HY