bushtaxcut

advertisement

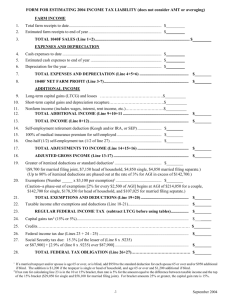

Inflation-Adjusted Tax Items for Tax Year 2003 By factoring inflation into the tax rates and certain other amounts, the law protects taxpayers from losing the value of various benefits. Each fall, the IRS issues two documents detailing the results of these adjustments for the coming year: * IR-2002-111 — pension plan limitations for 2003; * Revenue Procedure 2002-70 — tax rates, standard deductions, exemptions and more than 30 other items for 2003. After these documents were issued, the Jobs and Growth Tax Relief Reconciliation Act of 2003 made changes to these inflation-adjusted items: * The 10% tax bracket expands to the first $7,000 of taxable income for single persons and married persons filing separately, to the first $14,000 for married persons filing jointly and surviving spouses. * The 15% tax bracket for married persons filing jointly and surviving spouses expands to $56,800 of taxable income. For a married person filing separately, it expands to $28,400, the same amount as for a single person. * The tax rates above 15% drop to 25%, 28%, 33% and 35%. * The standard deduction for married persons filing jointly and surviving spouses rises to $9,500. For a married person filing separately, it rises to $4,750, the same as a single person's amount. Revised 2003 Tax Rate Schedules If TAXABLE INCOME The TAX Is THEN Is Over But Not Over This Amount Plus This % Of the Excess Over SCHEDULE X — Single $0 $7,000 $0.00 10% $0.00 $7,000 $28,400 $700.00 15% $7,000 $28,400 $68,800 $3,910.00 25% $28,400 $68,800 $143,500 $14,010.00 28% $68,800 $143,500 $311,950 $34,926.00 33% $143,500 $311,950 -$90,514.50 35% $311,950 SCHEDULE Y-1 — Married Filing Jointly or Qualifying Widow(er) $0.00 $0 $14,000 $0.00 10% $14,000 $56,800 $1,400.00 15% $56,800 $114,650 $7,820.00 25% $114,650 $174,700 $22,282.50 $174,700 $311,950 $39,096.50 $311,950 $14,000 $56,800 28% 33% $114,650 $174,700 -$84,389.00 35% $311,950 SCHEDULE Y-2 — Married Filing Separately $0 $7,000 $0.00 10% $0.00 $7,000 $28,400 $700.00 15% $7,000 $28,400 $57,325 $3,910.00 25% $28,400 $57,325 $87,350 $11,141.25 28% $57,325 $87,350 $155,975 $19,548.25 33% $87,350 $155,975 -$42,194.50 35% $155,975 SCHEDULE Z — Head of Household $0 $10,000 $0.00 $10,000 $38,050 $1,000.00 15% $38,050 $98,250 $5,207.50 25% $98,250 $159,100 $20,257.50 28% $159,100 $311,950 $37,295.50 $311,950 10% $10,000 $38,050 $0.00 $98,250 33% $159,100 -$87,736.00 35% $311,950 What is alternative minimum tax? The alternative minimum tax prevents a taxpayer with substantial income from avoiding a significant tax liability. It equals the excess of the tentative minimum tax over the regular tax. The tax laws give preferential treatment to certain kinds of income and allow special deductions and credits for some kinds of expenses. The alternative minimum tax attempts to ensure that all individuals who benefit from these tax advantages will pay at least a minimum amount of tax. The alternative minimum tax is a separate tax computation that, in effect, reduces the benefit of certain deductions and credits, thus creating a tax liability for an individual who would otherwise pay little or no tax. You may have to pay the alternative minimum tax if your taxable income for regular tax purposes, plus any of the adjustments and preference items that apply to you, is more than a specified exemption amount. The Sales and Growth Tax Relief Reconciliation Act of 2003 increased the exemption amounts to $40,250 (from $35,750) for unmarried individuals, and to $58,000 (from $49,000) for joint filers. To determine if you may be subject to the alternative minimum tax, refer to the Instructions for Form 1040 (General Inst.) for line 41, or refer to Form 6251 (PDF), Today's Economic Lesson in Taxation Let's put tax cuts in terms everyone can understand. Suppose that every day, ten men go out for dinner. The bill for all ten comes to $100. If they paid their bill the way we pay our taxes, it would go something like this: * The first four men (the poorest) would pay nothing. * The fifth would pay $1. * The sixth would pay $3. * The seventh $7. * The eighth $12. * The ninth $18. * The tenth man (the richest) would pay $59. So, that's what they decided to do. The ten men ate dinner in the restaurant every day and seemed quite happy with the arrangement, until one day, the owner threw them a curve. "Since you are all such good customers," he said, "I'm going to reduce the cost of your daily meal by $20." So, now dinner for the ten only cost $80. The group still wanted to pay their bill the way we pay our taxes. So, the first four men were unaffected. They would still eat for free. But what about the other six, the paying customers? How could they divvy up the $20 windfall so that everyone would get his 'fair share'? The six men realized that $20 divided by six is $3.33. But if they subtracted that from everybody's share, then the fifth man and the sixth man would each end up being 'PAID' to eat their meal. So, the restaurant owner suggested that it would be fair to reduce each man's bill by roughly the same amount, and he proceeded to work out the amounts each should pay. And so: * The fifth man, like the first four, now paid nothing (100% savings). * The sixth now paid $2 instead of $3 (33% savings). * The seventh now paid $5 instead of $7 (28% savings). * The eighth now paid $9 instead of $12 (25% savings). * The ninth now paid $14 instead of $18 (22% savings). * The tenth now paid $49 instead of $59 (16% savings). Each of the six was better off than before. And the first four continued to eat for free. But once outside the restaurant, the men began to compare their savings. "I only got a dollar out of the $20," declared the sixth man. He pointed to the tenth man "but he got $10!" "Yeah, that's right," exclaimed the fifth man. "I only saved a dollar, too. It's unfair that he got ten times more than me!" "That's true!!" shouted the seventh man. "Why should he get $10 back when I got only $2? The wealthy get all the breaks!" "Wait a minute," yelled the first four men in unison. "We didn't get anything at all. The system exploits the poor!" The nine men surrounded the tenth and beat him up. The next night the tenth man didn't show up for dinner, so the nine sat down and ate without him. But when it came time to pay the bill, they discovered something important. They didn't have enough money between all of them for even half of the bill! And that, boys and girls, journalists and college professors, is how our tax system works. The people who pay the highest taxes get the most benefit from a tax reduction. Tax them too much, attack them for being wealthy, and they just may not show up at the table anymore. There are lots of good restaurants in Europe and the Caribbean. David R. Kamerschen, Ph.D. Distinguished Professor of Economics 536 Brooks HallUniversity of Georgia AUTHOR: TITLE: SOURCE: Mortimer B. Zuckerman Hey, Big Spender U.S. News & World Report 127 no24 72 D 20 1999 If anybody had said that we would threaten one of our greatest public policy successes of the past decade--to wit, the painfully achieved federal budget surplus--I would have said, "Not in this century!" But the century is nearly over and they are back, the big spenders and the tax spendthrifts. Bill Bradley personifies the spenders. His health care program would add $1 trillion to federal expenditures, a sum roughly consuming the entire federal surplus for the next 10 years. Republicans in Congress wanted to fritter the surplus on a tax cut. They were repulsed by a Clinton veto, but now George W. Bush talks of blowing the entire $1 trillion on his tax-cut program. Thank heavens we don't have to eat either bowl of porridge. Fiscal conservatives have cooked up a Goldilocks bowl that is not too hot, not too cold, but just right. This is to maintain the discipline of explicit spending caps on discretionary spending and to use whatever surplus emerges to reduce the debt government has accumulated over the past two decades. The benefits of the spending caps, accompanied by modest tax increases initiated by President Bush in 1990 and extended more ambitiously by President Clinton in 1993, are palpable. That is how we got control of the deficit. It was the springboard for recovery. The financial community regained confidence in government, which enabled the Federal Reserve to lower interest rates. Private investment surged from 7 percent of the gross domestic product in the early 1990s to 13 percent today, the highest level in this century. The investment has generated a burst of productivity, which has in turn constrained and contained inflation, despite much higher rates of GDP growth alongside the lowest levels of unemployment in almost 30 years. What the spenders and tax spendthrifts obscure by their fast talk is that the projected surplus is no more than an estimate. It assumes adherence to spending caps and even further cuts in discretionary spending over the next decade. Can Congress be trusted to maintain a budget surplus without touching the Social Security surplus? One has only to ask. Both House and Senate have shown a marked inability to live within the budget caps. This year, they took the easy way by looking around for the highest revenue estimates, then investing in gimmicks. They took $28 billion out of the budget and called it "emergency spending." They even sought to use some of the projected surplus from the year 2001 to create the illusion of a budget balance. Simultaneously, and here is the hypocrisy of it, they set new records in pork-barrel spending. Our politicians, of course, are pandering to the dominant wings in their respective parties. Bill Bradley is appealing to the spend-and-tax left wing of the Democratic Party. Not only would his massive health care program exceed the estimated on-budget surplus of $1 trillion over the next decade, but he acknowledges it may even require more taxes-and this for a program that dumps Medicaid and places nursing homes under the less stringent controls of the states. The people are right. George W. Bush, of course, tries to justify his tax-cut program with Republican rhetoric about giving money back to the people and limiting government. But what is given away now in an election will have to be recovered later either by higher payroll taxes or by deep cuts in Social Security and Medicare benefits. Never mind that he has, in addition, proposed spending increases for defense and other items. Both the spenders and tax spendthrifts would jeopardize our prosperity by forcing the government back to an inflationary borrow-and-spend spiral. The good news is that fiscal prudence is supported by the American people. Politicians who have in recent years tried to bribe voters with increased spending programs or big tax reductions have been rejected. Voters reckon that the economy is working on all cylinders so that bigger spending or tax cuts would provoke the Federal Reserve into raising interest rates, which would in turn dampen the surge of investment. The country needs more national savings, not less. The government needs larger budget surpluses to deal with Social Security and reduce our dependence on foreign borrowing. This is no time to change our program. It ain't broke. Don't fix it.