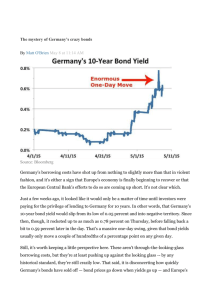

Forecasting interest rates - Risk Policy and Regulation

advertisement