IFRS Accounting of Pension Obligations

advertisement

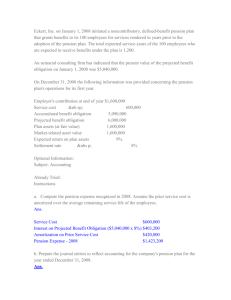

r itu For Inst ly. Use On vesto tional In Pension IFRS Accounting of Pension Obligations Highlights Understand. Act. PortfolioPraxis: Akademie 2 Pension Content 5 Introduction 5 Defined Contribution vs. Defined Benefit Plans 6 Defined Contribution Plans 8 Defined Benefit Plans Imprint Allianz Global Investors Europe GmbH Mainzer Landstraße 11–13 60329 Frankfurt am Main Global Capital Markets & Thematic Research Hans-Jörg Naumer (hjn), Dennis Nacken (dn), Stefan Scheurer (st), Maximilian Loebermann (ml) 3 Pension IFRS Accounting of Pension Obligations International accounting, in particular on the basis of International Financial Reporting Standards (IFRS), has become increasingly important in recent years. This development dates back at least to the so-called IAS Regulation of the European Union of 19 July 2002 (No. 1606 / 2002). This regulation requires European enterprises listed on a European exchange to prepare their consolidated financial statements in accordance with International Financial Reporting Standards, beginning financial year 2005. Dr. Martina Bätzel has been working in the Pensions department of Allianz Global Investors KAG since mid-2007 and was appointed Managing Director of Allianz Treuhand GmbH in September 2010. Following an apprenticeship in banking with Deutsche Bundesbank, she studied economics as well as business/ economics education in Mainz. After having obtained her doctorate in economic policy, she worked from 2001 to 2007 as consultant and executive assistant at Dr. Dr. Heissmann GmbH (now Towers Watson). Michael Heim is a DAV actuary and an IVS-examined actuarial expert for pension schemes at Allianz Global Investors Pensions department. After his studies in business mathematics at Ulm University he started his career with Allianz in 1997. He has more than 15 years experience in the field of occupational pension schemes. 4 1. Introduction Within IFRS, Standard IAS 19 “Employee Benefits” (IAS: International Accounting Standard) governs the accounting of employee benefits. Employee benefits include: short-term benefits (e. g. wages, salaries, paid annual leave), long-term post-employment benefits (e. g. retirement benefits), other long-term benefits (e. g. jubilee benefits, claims from working-life time accounts), and termination benefits (e. g. termination payments). The majority of the content of IAS 19 addresses post-employment benefits, i. e. requirements that pensions be accounted for under IFRS. Pensions in Germany can be classified according to the five ways of implementing them – pension commitment, direct insurance, German Pensionskasse, pension funds and support funds (Unterstützungskasse). As part of employee remuneration or as a supplement to pensions, increasing use has also been made in recent years of so-called working-life time accounts. Among other reasons, against the background of this very diverse and sometimes complex array of pension schemes, it is always a challenge for German IFRS adopters to properly and yet practically apply the accounting rules in IAS 19, which are heavily influenced by Anglo-American accounting rules, to the specific German situation. The aim of this presentation is to outline the basic features of the regulatory content of IAS 19 for long-term post-employment benefits, while providing a means of classifying and applying the regulations taking into account the situation in Germany. For selected topics, explanations will be provided on specific national accounting features for the German balance sheet in accordance with the German Accounting Law Modernization Act (Bilanzrechtsmodernisierungsgesetz – BilMoG) and German tax accounting pursuant to the German Income Tax Act (Einkommensteuergesetz – EStG). In an explanatory note, Contractual Trust Arrangements (CTA) will be introduced as an alternative liquidity-friendly solution for the external funding of pension obligations in accordance with both the German Commercial Code (HGB) and IFRS. 2. Defined Contribution vs. Defined Benefit Plans While a distinction is made in German accounting between direct and indirect pension obligations, the important distinction under IAS 19 is between: Defined Contribution Plans and Defined Benefit Plans. In a defined contribution plan, the contributions (e. g. to a pension fund) are recognised as an expense in the period in which they are incurred. If the employer matches the amount and timing of his contributions to obligations for each accounting period, it is not necessary to recognise further liabilities. The accounting for defined benefit plans is more complex: using actuarial assumptions and methods, pension obligation and expenses are identified and compared with the separated assets or resulting return used to meet the obligation. 5 Pension 3. Defined Contribution Plans Example In the US, ABC company promises its employees an annual contribution of 2 % of pensionable salaries into the XYZ pension fund. The company does not incur any risks or obligations (e. g. negative investment performance) beyond the contributions. 3.1 Definition Under IAS 19.7, a defined contribution plan is defined using the three following cumulative requirements: 1. Fixed contributions: The company only has the obligation to make contributions to the plan. The amount of the benefits is based on these contributions, including the resulting investment return. 2. Separate entity: The contributions are paid to an external pension provider (e. g. a pension fund) that is legally separate from the company. 3. No legal or constructive obligation for further contributions: The company must not have any subsidiary responsibility or supplementary contribution liability, e. g. in the case of negative investment performance. Similarly, a positive investment performance may not lead to reductions in contributions or refunds of contributions. In a defined contribution plan under IAS 19.7, the company consequently bears no risks, neither biometric risks nor investment risks, nor any other obligations associated with the pension plan. 3.2 Accounting The IFRS accounting for defined contribution plans is comparatively simple: For each accounting period, the amount recognised and presented in the notes as pension expense is the contribution amount resulting from the underlying pension plan formula (in exchange for the employee’s service in the same period). Because the company’s liability, consisting of this contribution, can be clearly identified, and the company then fulfils this obligation by making the contribution, accounting for defined contribution plans in general does not require any actuarial assumptions or assessments. Only if the contribution is due more than a year after the end of the accounting period in which the employee rendered the service the future payment must be discounted. This discount is based on the actuarial interest rate of defined benefit plans. Figure 1: Structure of defined contribution plans Company Service Contributions Wages and contribution commitment Benefits Employee Risks and rewards lie with the employee Source: Own research, Allianz Global Investors Pensions 6 Pension Fund The balance sheet is impacted by defined contribution plans only if the company has not matched the timing and amount of its contributions to obligations during the accounting period: A liability is incurred when the plan is underfunded, i. e. the amount paid is lower than the contributions due (deferred liability). An asset is recognised when the plan is overfunded, i. e. the amount paid is greater than the contributions due (prepaid expense). Once a company’s commitment to (matching) contribution payments has finally been fulfilled, no further consideration regarding the recognition of liabilities is necessary. Contributions are paid to a legally separate entity. This entity is exclusively responsible for the future payments to beneficiaries. The company itself no longer has access to the plan assets after payment of the contributions. The company is then no longer to be considered the legal or economic beneficiary of the assets, which are attributable to the eligible employees and are not to be recognised on the balance sheet of the company. 3.3 Practice: Do Defined Contribution Plans Exist in Germany? Due to the employer’s subsidiary responsibility (see § 1 para. 1 German Company Pension Act), there are no defined contribution plans in Germany following a strictly formal interpretation of IAS 19.7. A word of caution: this means that the term “Defined Contribution Plan”, which we will be using throughout this document, is not directly applicable in any discussion concerning the German system of pension plans. In many instances, a more accurate term might be “ContributionOriented Plan”. Even contribution-oriented plans should initially be classified as defined benefit plans. However, in specified circumstances, IAS 19 permits the treatment of these commitments as defined contribution plans. This applies, in particular, for so-called insured plans according to IAS 19.39. An insured plan is defined as a pension plan whose benefits are financed through the payment of insurance premiums. Plans of this type can be treated as defined contribution plans unless the company has a legal or constructive obligation to: pay the employee benefits directly when they fall due, or pay further amounts if the insurer does not pay all future employee benefits relating to employee service in the current and prior periods. Question: Do the insurance-based solutions in Germany, such as direct insurance, meet the conditions for insured plans? The prevailing opinion of the accounting working group of the DAV / IVS Committee (DAV: German Actuarial Association; IVS: German Institute of Actuarial Experts) is that, in insurance-based solutions, the final liability is to be considered only as a contingent liability. Direct insurance, German Pensionskasse and pension funds can in general be classified as insured plans in accordance with IAS 19.39, and thus as defined contribution plans, if the following criteria are met: The company is the policyholder and thus is liable for the contributions. The employee is the insured person and has the right to the benefits. The employee has a legally enforceable right vis-à-vis the pension provider. The pension provider guarantees the benefits in compliance with regulatory requirements. The guaranteed benefits are based solely on the contributions paid, plus any guaranteed interest, less cost and risk premiums. 7 Pension The surplus will be credited to the employee. Fully vested benefits are fully funded upon termination of employment. The amount of the post-employment benefits is determined by the amount of capital reserves. Pension adjustments depend on policyholder bonus. Finally, the classification of an insurancebased solution as defined contribution plan requires approval by the company’s auditor. 4. Defined Benefit Plans 4.1 Definition Defined benefit plans are characterized by the fact that – as opposed to defined contribution plans – the risks and obligations of the pension commitment remain with the company even after the accounting period. Example The company XYZ Inc. grants retirement benefits to its employees. The lifelong pension benefit amounts to 1 % of last gross salary before retirement for each eligible year of service. The company bears all risks and obligations from the pension commitment, such as the investment and longevity risk. 4.2 Accounting In general, every pension plan is a defined benefit plan unless it definitely meets the requirements for classification as a defined contribution plan. Pursuant to IAS 19.25, if there is any doubt, this distinction which is sometimes not that simple must be made based on the “economic substance of the plan”. While it is relatively simple to determine the expense of contributions for each accounting period for defined contribution plans, the (unknown) expense for each period, i. e. the contribution required for financing the pension benefit, must be determined actuarially on the basis of the (known) benefit when Figure 2: Structure of defined benefit plans Indirect commitment Direct commitment Company Risks lie with the company Company Risks lie with the company Service Benefits Wages and benefit commitment Employee Service Wages and benefit commitment Employee Source: Own research, Allianz Global Investors Pensions 8 Funding Pension Fund Benefits accounting for defined benefit plans. When these actuarial calculations are made, the following accounting principles in particular must be taken into consideration: actuarial assumptions must be established in such a way that they meet the best estimates. Suitable probabilities for the occurrence of biometric risks of death, disability, etc. Discounting of future benefits using an actuarial interest rate appropriate for the maturity Economic assumptions for trends and adjustments of pension benefits (e. g. cost of living and income) The primary goal of demographic assumptions is to describe the current status and the expected development of the number of people to be covered by the pension plan. The most important parameters for demographic assessment are the probabilities for the occurrence of the biometric risks of death and disability. Although these probabilities could, in principle, be determined individually for each set of people to be assessed, due to insufficient set size and excessive cost, statistical analyses are usually based on generally accepted actuarial tables for probabilities of death and disability. In Germany, the so-called Heubeck actuarial tables (current actuarial tables: Heubeck 2005 G by Klaus Heubeck) are customarily used for IFRS accounting of pension liabilities. These actuarial tables can also be customised for an individual company by applying modifications (increase or reduction of probabilities). 4.2.1 Accounting principles Under IFRS accounting for defined benefit plans, a basic distinction is made between demographic valuation assumptions and economic valuation assumptions. While demographic assumptions reflect the characteristics of the pension plan participants who are entitled to benefits, economic assumptions are determined by macroeconomic as well as company-specific indicators and trends. In accordance with IAS 19.73, all Demographic Valuation Assumptions 9 Pension Other demographic assessment parameters to be taken into consideration include employee fluctuation and assumptions about retirement age or the retirement behaviour of pension beneficiaries. Fluctuation probabilities are generally derived individually for each company as a function of gender, age and service time. Actuarial analyses have shown that taking fluctuation probabilities into consideration may reduce pension obligations by up to about 0.5 %, which means that it has a rather small impact on the valuation of pension obligations. Retirement age for valuation purposes must be in accordance with the provisions of the pension plan (fixed / earliest age from which retirement benefits may be drawn). In practice, the most likely retirement age is very often used as the basis for the assessment. The German Income Tax Directive R 6 a EStR states in paragraph 11 that “for some or all pension obligations, the earliest possible date for early retirement claims from statutory pension can be used as the date of entry into the benefit plan.” This guideline is often followed in the IFRS valuation of pension obligations. Economic Valuation Assumptions The central economic assumption is the discount rate at which future benefits are discounted to the valuation date. The discount rate should, in principle, reflect the time value of money and be based on the yields of high quality fixed-income corporate bonds on the valuation date. In practice, “high quality corporate bonds” usually means corporate bonds rated at least AA (using the terminology of Standard & Poor’s). The maturity and currency of the bonds and the pension obligation should also match. Since the introduction of the Eurozone, there has generally been a sufficiently liquid market for corporate bonds denominated in Euro to determine the discount rate. If, however, there is no sufficiently 10 liquid market for such corporate bonds, the market yield on government bonds may be used alternatively (taking into account a risk premium to compensate for the difference in credit quality). If there is no sufficiently active market for very long-term bonds (which is a particular issue for maturities longer than 30 years), the discount rate is derived using mathematical extrapolation methods. Historically, discount rates in accordance with IAS 19 have periodically been subject to significant fluctuations over time because of the closing date principle, with corresponding effects on the amount of the pension obligation: A higher discount rate ceteris paribus reduces the pension obligation, while a lower discount rate ceteris paribus increases the pension obligation. National accounting While the determination of the discount rate under IAS 19 grants a certain amount of leeway for calculation and interpretation, the German Accounting Law Modernization Act clearly states that the discount rates determined and published monthly by the Deutsche Bundesbank, based on a market-oriented average interest rate corresponding to the predicted residual maturity of the obligation, are to be applied for discounting pension obligations in the HGB balance sheet. The only option granted is that, for simplification purposes, a uniform interest rate may be used for the entire pension plan based on a maturity of 15 years. Among the economic evaluation parameters, the IFRS financial reporting of pension obligations also subsumes trend assumptions and the return on plan assets. In contrast with the closing date principle under German tax law, the valuation of pension obligations under IAS 19 explicitly calls for taking into account the expected future changes and trends in the valuation bases for pension benefits. In particular, dynamic effects of current pension benefits (so-called pension trends) are to be included in the calculations, and dynamic salary trends must be taken into account for salary-linked pension plans. With the revised version of IAS 19 rev. 2011 published on 16 June 2011, the return on plan assets (“expected return on plan assets” in the terminology prior to IAS 19 rev. 2011) was substantially revised. For accounting periods starting from 1 January 2013, the applicable discount rate for the calculation of the pension obligation is implicitly used as return rate for the plan assets as well. Accordingly, the return on plan assets will no longer be determined individually for the company, and the allocation of the plan assets is irrelevant to its determination. 4.2.2 Defined Benefit Obligation Definition The value of the pension obligation on closing date is designated in IFRS accounting of defined benefit plans as the defined benefit obligation (DBO). In actuarial terms, the defined benefit obligation represents the total present value of the accrued pension obligation that results from the services rendered by the employee during the accounting period and in previous periods. Figure 3: Accounting principles pursuant to IAS 19 rev. 2011 Accounting principles pursuant to IAS 19 rev. 2011 Demographic Valuation Assumptions (company-specific assumptions) Biometric assumptions (in particular death, disability) Economic Valuation Assumptions (company-specific assumptions and macroeconomic assumptions) Discount rate Fluctuation probabilities = Return on plan assets Retirement age/retirement behaviour Trend assumptions (e. g. pension and wage trend) Objective: Realistic valuation through … … unbiased and mutually compatible assumptions, … assumptions that are neither imprudent nor excessively conservative, … assumptions that reflect the economic relations. Best estimate principle in accordance with IAS 19.73 Source: Own research, Allianz Global Investors Pensions 11 Pension Valuation / Determination The objective of actuarial valuation methods is to determine the value of the pension obligation or of the premium required for financing the pension obligation during the appropriate period. the pension obligation increases over time, as the discount period continues to shorten. A particular characteristic of the Projected Unit Credit Method is that the value of the pension claims on each reporting date is not based on reporting date assumptions, but instead is anticipated or determined (hence „projected“) by taking into account future changes of the key valuation parameters, such as salary and pension trends. Under IAS 19, since 31 December 1999, the Projected Unit Credit Method (PUC method) has been explicitly required as the actuarial valuation method for the IFRS balance sheet. The Projected Unit Credit Method is a valuation procedure from the aggregation methods class. Under aggregation methods, the amount of the pension obligation is calculated as the sum of the expected future benefit payments discounted on the respective closing dates and weighted with their probabilities, provided they have been accrued by the reporting date. Based on the individual obligation resulting from a classic defined benefit plan, the premium required to fund National accounting While the German Accounting Law Modernization Act does not require an explicit evaluation method for the HGB balance sheet, in German tax accounting pursuant to Section 6 a EStG, only the so-called partial valuation method (Teilwertverfahren) may be applied. Pension obligations (cumulative) Figure 4: DBO process using the PUC method and increase in funding premium over time Premium y Premium x x Source: Own research, Allianz Global Investors Pensions 12 x+1 y y+1 65 Age 4.2.3 Plan Assets While pension obligations in Germany are traditionally often financed internally through investments that are not matched with the obligation, but instead used for the core business of the company (so-called internal financing), in the Anglo-American world the primary method used is external financing of the obligation (so-called outside funding). With outside funding of pension obligations, designated assets protected against the insolvency of the sponsor are accumulated outside the company; these assets are exclusively “reserved” for fulfilling pension obligations (so-called plan assets). Definition IAS 19 refers to assets as plan assets, i. e. assets that must be offset or netted against the underlying pension obligation, if the following three criteria are cumulatively met: 1. Separation (“… held by an entity (a fund) that is legally separate from the reporting enterprise …”). The assets must be outsourced to an independent entity (e. g. a trust / CTA solution), which has the sole purpose of financing, paying out and ensuring benefits. Repayments to the company may only be made if: there is excess funding, i. e. if the pension liabilities can be fully serviced by the remaining plan assets, or if the external entity reimburses the company for benefits that the company has already paid to the pension beneficiaries (known as Reimbursement). 2. Exclusivity of purpose (“… available to be used only to pay or fund employee benefits …”) The plan assets are used exclusively for payment or financing of benefits. 3. Availability in case of insolvency (“… are not available to the reporting enterprise’s own creditors (even in bankruptcy) …”) The assets must be unavailable to the creditors of the company – particularly in the case of bankruptcy. The plan assets consist of the funding provided by the company and the returns earned less benefit payments. The assets may comprise financial assets (e. g. shares, bonds, mutual funds, qualifying insurance policies), property, plant and equipment (e. g. machinery) or real estate. Financial instruments issued by the company itself (i. e. treasury shares) may be suitable as plan assets if they are transferable. In particular, the criterion of transferability is satisfied when the assets are freely tradable. National accounting In contrast to the three criteria under IAS 19, for balance sheets in accordance with German HGB, plan assets must only meet two requirements: exclusivity of purpose and insolvency-protection. A transfer of assets to an independent entity is not necessary – in contrast to IAS 19. As a result, there may be a balance sheet effect in the HGB balance sheet through the pledging of a securities account, e. g. for the purpose of covering a managing partner pension commitment. For exclusivity of purpose, the Accounting Law Modernization Act requires that plan assets be liquid at all times to cover pension obligations, which excludes operating assets (such as owner-occupied real estate) from use as plan assets for the HGB balance sheet. The approval of plan assets under IFRS and HGB always depends on close coordination with the responsible auditor. The classification of plan assets under IFRS and HGB and the consequences of these different definitions can be summarised as follows: 13 Pension Figure 5: Different definitions of plan assets under IFRS and HGB Requirements 1. Separation 2. Exclusivity of Purpose 3. Insolvency-Protection Plan assets under IFRS Plan assets under HGB Transfer to a legally separate entity No requirement Availability (liquidity) for fulfilling pension obligations Assets must be available exclusively and at all times for pension liabilities (no assets that are necessary for operations) Identical requirement under IFRS and HGB Source: Own research, Allianz Global Investors Pensions Figure 6: Consequences of the different definitions of plan assets under IFRS and HGB Plan assets under IFRS No plan assets under IFRS Plan assets under HGB Securities (e.g. special or mutual fund units) in CTA solutions Pledged securities account No plan assets under HGB Owner-occupied real estate or loan to the sponsoring company in CTA solutions Unpledged securities account Source: Own research, Allianz Global Investors Pensions Valuation / Determination Under IAS 19, plan assets are to be measured at fair value as of the reporting date. Fair value generally corresponds to the observed market value or value on a securities exchange, which is usually easily determined, particularly for an investment in the form of financial instruments. Difficulties in determining fair value may occur for some assets, such as property, plant and equipment or real estate. In such cases, fair value is to be determined in the best possible way, e. g. through appropriate valuation procedures and expert opinions. For qualifying insurance policies that secure the benefit commitments by fully matching the amount and timing of those benefits, 14 the fair value of the insurance contract is equivalent to the present value of the commitments made for future benefits (Defined Benefit Obligation) (so-called corresponding measurement). Therefore, an economic effect in the IFRS balance sheet comparable to a defined contribution plan is achieved through this full offsetting. Nevertheless, in this case as well, disclosure requirements for the notes to the balance sheet continue to be relevant for the defined benefit plan. If the promised benefits and the benefits secured through qualifying insurance policy do not match, the asset value of the insurance contract is usually presented as fair value and offset with the pension obligation. National accounting With the Accounting Law Modernization Act, the valuation of plan assets at fair value (rather than at cost) is also applicable for the first time in the HGB balance sheet. Trusts A trust solution (Contractual Trust Arrangement, CTA) can be used to hold assets as plan assets for funding pension obligations: As a vehicle set up by a single company or – often more efficient – by making use of a multi-employer trust, such as Allianz Treuhand GmbH. Using a multi-employer trust, companies can participate regardless of their affiliation, size, and the scope of their existing obligations, and achieve a balance sheet effect by offsetting benefit obligations and plan assets in both IFRS and the HGB balance sheets. How does a trust work, in particular in the multi-employer form? For external funding and insolvency protection of pension obligations, the company enters into a trust agreement with the trustee, and on this basis, transfers the assets necessary to cover these obligations. The actual administration of the trust assets is usually outsourced to a separately appointed asset manager. According to the trust agreement, the trustee becomes the legal owner of the transferred assets. He may only use the assets in order to provide or finance the benefits promised in the pension plan, i. e. the trust assets are strictly reserved to the defined purpose. This applies even if the employer / trustor should become insolvent. In this case, the employee can apply directly to the trust to receive the promised benefits. However, the trust does not provide any guarantee, but pays out the benefits only if and insofar as the necessary funds were transferred from the employer. The trust structure is called “double-sided,” because the trustee acts both as administrative trustee for the employer as well as security trustee for the employee. However, a contractual relationship exists only between the company and the trustee; the security trust is a contract for the benefit of third parties, i. e. the beneficiaries of the pension plan. Using a trust solution for creating plan assets offers a number of advantages: Foremost is flexibility, because there are no set guidelines in a trust solution as to amount or timing of contributions by the employer. The funding of the trust may be based on the individual circumstances of the company, depending, for example, on the intended level of external funding or the available liquidity. The netting of trust assets and pension obligations of the trustor company is possible because while the trust assets do legally belong to the trust, economically they remain allocated to the trustor company. The criteria for plan assets, which are set according to international accounting rules and the German Commercial Code, are fulfilled by an appropriately designed trust agreement. The final approval for offsetting the trust assets with the pension obligations lies with the auditor of the company. In German tax accounting, the pension obligation is not offset with the pension assets; the trust remains invisible for tax purposes, in a manner of speaking. This leaves the tax holiday effect of the provision in place. Important for the employees: The external funding of the trust will not affect the tax treatment of employee contributions or benefits. Since the pension plan remains untouched under labour law by external funding through the trust, no consent of the individual employees or of the works council is required for the implementation of a trust solution. 15 Pension In addition, a trust solution also improves the insolvency protection for the benefit commitments. While a statutory insolvency protection for occupational pensions in Germany already exists in the form of the German Pension Protection Association (Pensions-SicherungsVerein – PSV), this applies only to statutory vested rights within the scope of pension law and benefits in the payout-phase. This means, in turn, that occupational benefit claims are not protected against insolvency if, for example, they are only contractually vested or if they exceed the protection limits of the PSV. Even accrued benefits from deferred compensation in the last two years before insolvency – if exceeding the contribution threshold of 4 % of statutory pensionable salary – are not legally protected against insolvency. The benefit claims of individuals who are not subject to the pension law, such as the controlling owner-manager of an enterprise, remain completely unprotected. In all these cases, private law insolvency protection can be set up by the trust. In addition, the trust can be used for providing insolvency protection for other obligations vis-à-vis the employees, e. g. from time accounts or part-time retirement. In multi-employer models, a broad range of capital investment structures (including hybrid structures) can be put in place with investment funds and insurance products. Biometric risks can also be hedged through the integration of the appropriate insurance components into the overall concept. Figure 7: Contractual Trust Arrangement Company Benefit obligation Benefit entitlement Transfer of assets Trust agreement Treuhand GmbH or e. V. Benefit claim Employee Claim procedure Source: Own research, Allianz Global Investors Pensions 16 Investment Asset manager 4.2.4 Pension Expense Service Cost Service cost will be recognised in profit and loss and calculated prospectively by the actuary. It includes: Current service cost Past service cost and Settlements. Past service cost may result from the subsequent improvement or deterioration of a pension plan. Unlike original current service cost, which reflects the benefit components newly accrued in the current accounting period, past service cost always relates to previous accounting periods. As a rule, past service cost was previously recognised over a certain period of time as a separate item in pension expense. Under IAS 19 rev. 2011, it is now subsumed as part of service cost and is to be fully and immediately recognised in the year of the plan change. The definition of past service cost was also expanded under IAS 19 rev. 2011 and now also includes effects associated with curtailments. Curtailments can arise at the closure of an operation, during restructuring or closures of pension plans. In the case of a curtailment, the company must be committed to substantially reducing the circle of persons entitled to benefits or to altering the pension plan so that significant portions of future years of service or salary increases lead only to reduced pension claims or to no pension claims. The current service cost is determined using the Projected Unit Credit Method. It corresponds to the actuarial cash value of the benefit components that are newly accrued by the (active) employees during the accounting period. Analogous to the defined benefit obligation, the following applies: All other things being equal, a higher discount rate reduces current service cost, and a lower discount rate increases current service cost. With a settlement, the company transfers, without any extended liability, the pension obligation for which it is responsible to another entity (e. g. another company or pension provider), or the pension obligation is extinguished by the payment of a termination indemnity. In accordance with IAS 19.113, the conclusion of an insurance contract does not lead to a settlement, if the employer remains subject to the extended liability to pay benefits. In the past, the structure and recognition of pension expense under IAS 19 was characterized by numerous accounting options that sometimes were contrary to the IFRS accounting principle of “true and fair view.” The revised version of IAS 19 rev. 2011 brought many changes in this area, with the objective of making classification as unambiguous as possible and improving comparability of income and expense components. Pension expense can now be categorised as: Service cost Net interest Remeasurement. 17 Pension The new IAS 19 rev. 2011 provides no guidelines regarding the explicit presentation of the individual pension expense items in the income statement. Service cost is, in practice, usually presented as personnel expense and recognised as part of operating profit in profit and loss. Net Interest Net interest, which is also recognised in profit and loss, represents the interest income or expense resulting from the net liability or from the net assets (so-called net defined benefit liability / asset as the difference between pension obligations and plan assets). In the terminology of the previous version of IAS 19, net interest comprised the sum of the interest cost and the expected return on plan assets, while under IAS 19 rev. 2011 the discount rate used to calculate the benefit obligation is now to be applied to both figures (see 4.2.1 Accounting principles). Expected changes during the accounting period due to pension payments or funding of plan assets are taken into account. A simple mathematical expression of net interest is: Net interest = (plan assets – pension obligation) x discount rate In practice, net interest is generally optionally included in operating results or in the financial results of the income statement. Therefore, with regard to the income and expense components of pension obligations, comparisons of annual financial statements of different companies continue to be of limited value. Although it was questionable in business terms, the presentation of interest cost in financial results and expected returns on plan assets in operating result was previously 18 possible –, it will no longer be possible in the future because of the net perspective. By combining the interest expense with the return on plan assets, all the risks and rewards of the actual investment of plan assets are now no longer recognised as an income component of net interest, but are now presented on the balance sheet within the framework of remeasurement described below. Remeasurement At the end of the accounting period, deviations naturally occur between the prospectively measured values (i. e. the expected values) and the actual values for the pension obligation, plan assets, etc. The reasons for this can, for example, be found in changed discount rates, the occurrence of biometric risks or unexpected developments of plan assets. These discrepancies between the expected and actual values are referred to as remeasurement. The valuation changes basically include all the changes in the pension obligation and the fair value of plan assets, as far as these are not included in service cost or net interest, i. e. they include in particular: actuarial gains and losses on the liability side (e. g. conditioned by changes in the discount rate) and deviations in the actual development of plan assets from the corresponding part of the net interest allocated to plan assets (based on the discount rate). In contrast to the recognition of service cost and net interest in the profit and loss statement, the remeasurement is immediately and completely recorded in equity, specifically in the statement of comprehensive income in accordance with IAS 1.81 (other compre- hensive income (OCI)). There is no longer any provision for deferred recognition in income of these amounts, such as in the framework of the corridor method, which was done away with in IAS 19 rev. 2011. The recognition of the remeasurement in other comprehensive income protects the income statement from excessive volatility. This approach is, in practice, often referred to as OCI or SoRIE method (SoRIE: Statement of Recognised Income and Expense), an approach that has been in the standard since 2004, and which had already been applied in Germany before the introduction of IAS 19 rev. 2011. It has been used by about twothirds of DAX companies and has found broad acceptance. The following figure presents the classification and allocation of pension expense for defined benefit plans pursuant to IAS 19 rev. 2011: National accounting In accordance with the provisions of German commercial and tax law, the pension provision is determined at the end of each accounting period. The difference between the pension provisions of the previous year, including benefits paid in the accounting period determines the pension expense to be recognised in income. 4.2.5 Balance Sheet Approach The revised version of IAS 19 rev. 2011 improves the comprehensibility, transparency and comparability of the balance sheet approach of defined benefit plans. In particular, this main goal of the new standard was achieved with the abolition of controversial accounting options (e. g. corridor method). Figure 8: Classification and allocation of pension expense pursuant to IAS 19 rev. 2011 Pensions expense pursuant to IAS 19 rev. 2011 Service cost Net interest Remeasurement • Current service cost • Interest cost • Past service cost • (Expected) Return on plan assets All changes to DBO or fair value of plan assets, provided they are not taken into consideration in service cost or net interest • Settlements On the basis of the discount rate for calculation of the DBO Recognition in profit and loss Recognition in OCI (Other comprehensive income) Source: Own research, Allianz Global Investors Pensions 19 Pension The IFRS balance sheet recognition of defined benefit plans is now the result of the net difference between the benefit obligation and plan assets (so-called net defined benefit liability / asset). Thus, both changes in the benefit obligation and developments of plan assets will, in the future, be immediately recognised in each accounting period, as part of full balance sheet recognition. The resulting fluctuations on the balance sheet, which may be substantial, are not, however, directly expressed in the income statement of the company, but are recorded in equity using the OCI or SoRIE method (cf. explanations on pension expense). The volatility of net obligations or net assets to be recognised and the equity implications may very well be subject to significant increase. If there are plan assets, the offsetting or netting of pension obligations and plan assets is mandatory, not optional. In simple terms, under IAS 19 rev. 2011, most accounting options were abolished in the accounting approach to defined benefit plans. IAS 19 follows the HGB accounting approach already familiar from the German Accounting Law Modernization Act, i. e. the net difference of the pension obligation is presented net of plan assets. Example The pension obligation is EUR 300,000. a. Plan assets total EUR 200,000 → The company has a Net Defined Benefit Liability amounting to EUR 100,000. b. Plan assets total EUR 350,000 → The company has a net defined benefit asset amounting to EUR 50,000 (at this point, information on the special provisions concerning the so-called asset ceiling under IAS 19.58 will be omitted). 20 4.2.6 Notes The information disclosed in the notes of an IFRS balance sheet (known as disclosures) should enable the reader of the balance sheet to understand and assess the economic fundamentals of the pension plan (IAS 19.120). Among other things, the following information is to be included in the disclosures: A general description of the type of pension plan (e. g. length-of-service plan), including the legal framework The main actuarial assumptions (e. g. discount rate, trend assumptions) A reconciliation from the beginning to the end of the accounting period for, among other items, the pension obligation, plan assets and balance sheet recognition A breakdown of pension expense into its individual components, including those items in which they are recognised in the income statement. Within the scope of IAS 19 rev. 2011, the disclosures on defined benefit plans have also been subjected to various changes which are intended to present, in more detail, the characteristics and risks associated with the pension plan. The following changes are examples: Sensitivity analyses of the pension obligation for any significant actuarial assumption, including explanations (sensitivity analyses for example concerning the discount rate, trends, retirement age and mortality rates; only one assumption should be varied in each case, i. e. there are no interactions required among the various assumptions) Information on the maturity profile of the pension obligations Information about any financial instruments and strategies in the pension plans (e. g. asset-liability matching). The new disclosure requirements are not to be considered a final “check list,” but rather to complement the comprehensive nature of the disclosures. With regard to the level of detail of the disclosures, the company can still decide on whether the objective of disclosure of information has been sufficiently fulfilled. 4.3. Practice: Case Study on Accounting of Defined Benefit Plans At the beginning of the accounting period, the pension obligation amounting to 1,000 monetary units is opposed to plan assets of 800 monetary units. The company, accordingly, presents a pension obligation amounting to 200 monetary units in the balance sheet. The changes and developments during the accounting period and the resulting implications for the balance sheet approach, liquidity and pension costs are shown in the table below: Figure 9: Case study on IFRS accounting of defined benefit plans Begin of period actual Defined Benefit Obligation (DBO) begin of period expected End of period (actual/recognized) Balance sheet Pension cost P&L OCI Liquidity –1.000 Service cost –100 –100 –100 Interest cost (5 %) – 50 – 50 –50 Benefit payments 50 50 Remeasurements 50 – 40 Defined Benefit Obligation (DBO) end of period – 40 –1.100 –1.140 Contributions 100 100 100 Benefit payments – 50 – 50 – 50 Return on plan assets (5 %) 40 40 Plan assets begin of period –1.140 800 Remeasurements Plan assets end of period 40 20 890 910 20 910 –230 –110 –20 100 Source: Own research, Allianz Global Investors Pensions 21 Pension The balance sheet value of the pension plan at the end of the accounting period is the net difference between pension obligation and plan assets. The company now presents a pension obligation in the amount of 230 monetary units. In the income statement portion of the pension expense, the service cost and net interest are both taken into consideration (consisting of the interest expense for the pension obligation and the interest income from plan assets, in each case based on the discount rate for calculating pension obligations). In the income statement, a pension expense amounting to 110 monetary units is recognised as income. 22 The company records valuation changes at the end of the accounting period resulting from the pension obligations and the plan assets in the amount of –20 monetary units in equity in other comprehensive income (OCI). In the terminology of IAS 19 rev. 2011, a negative (positive) sign implies an actuarial loss (gain). Pension payments to beneficiaries, which the company withdraws in full from the plan assets, impact liquidity, as well as the funding of the plan assets in the amount of 100 monetary units. Investments involve risk. The value of an investment and the income from it may fall as well as rise and investors may not get back the principal invested. Equities can be volatile and, unlike bonds, do not offer a fixed rate of return. Bond prices will normally decline as interest rates rise. High-yield or “junk” bonds have lower credit ratings and involve a greater risk to principal. Dividend-paying stocks are not guaranteed to continue to pay dividends. Investments in emerging markets may be more volatile than investments in more developed markets. Derivative prices depend on the performance of an underlying asset; derivatives carry market, credit and liquidity risk. Past performance is not indicative of future performance. No offer or solicitation to buy or sell securities, nor investment advice / strategy or recommendation is made herein. In making investment decisions, investors should not rely solely on this material but should seek independent professional advice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. Forecasts are inherently limited and should not be relied upon as an indicator of future results. The views and opinions expressed herein, which are subject to change without notice, are those of the issuer and / or its affiliated companies at the time of publication. The data used is derived from various sources, and assumed to be correct and reliable, but it has not been independently verified; its accuracy or completeness is not guaranteed and no liability is assumed for any direct or consequential losses arising from its use, unless caused by gross negligence or willful misconduct. The conditions of any underlying offer or contract that may have been, or will be, made or concluded, shall prevail. The duplication, publication, extraction or transmission of the contents, irrespective of the form, is not permitted. This is a marketing communication. This material has not been reviewed by any regulatory authorities, and is published for information only, and where used in mainland China, only as supporting materials to the offshore investment products offered by commercial banks under the Qualified Domestic Institutional Investors scheme pursuant to applicable rules and regulations. This document is being distributed by the following Allianz Global Investors companies: RCM Capital Management LLC, an investment adviser registered with the US Securities and Exchange Commission; Allianz Global Investors Europe GmbH, a licensed provider of financial services (Finanzdienstleistungsinstitut) in Germany, subject to the supervision of the German Bundesanstalt für Finanzdienstleistungsaufsicht (BaFin) and an investment adviser registered with the US Securities and Exchange Commission; RCM (UK) Ltd., which is authorized and regulated by the Financial Services Authority in the UK; Allianz Global Investors Hong Kong Ltd. and RCM Asia Pacific Ltd., licensed by the Hong Kong Securities and Futures Commission; Allianz Global Investors Singapore Ltd., regulated by the Monetary Authority of Singapore [Company Registration No. 199907169Z]; RCM Capital Management Pty Limited, licensed by the Australian Securities and Investments Commission; and RCM Japan Co., Ltd., registered in Japan as a Financial Instruments Dealer. 23 Allianz Global Investors Europe GmbH Mainzer Landstraße 11–13 60329 Frankfurt am Main September 2012 www.allianzglobalinvestors.eu