CHAPTER 2 LITERATURE REVIEW

advertisement

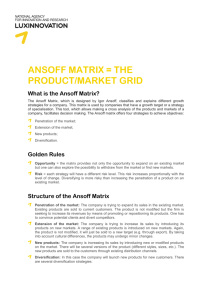

CHAPTER 2 LITERATURE REVIEW 2.1. Diversification Strategy Market Alternatives Product/Service Alternatives Reduce Market Existing Market Expanded Market Market diversification Reduced Product/Services Existing Product/Services Modified Product/Services New Market Product diversification Market and Product diversification New Product/Services Figure 1: Competitive Position Growth Alternatives ( Woodcock & Beamish, 13: 2003 ) Diversification is a part of corporate-strategy (Hill & Jones: 2001; Pearce II & Robinson: 2003; Hit et al: 2007). Diversification inside corporate strategy level means this option may bring the future direction of the company. 2.2. Reasons for diversification Every strategy always has reasons because strategy would be used by the company to fulfill its goals. Reasoning is a basic-concept for effective-strategy. Hit et al (173: 2007) explained some reasons why a company uses diversification-strategy 2.2.1. Value Creating Diversification • Economies of scope (related diversification) o Sharing activities o Transferring core competencies • Market Power (related diversification) o Blocking competitors through multipoint competition o Vertical integration • Financial economies (unrelated diversification) o Efficient internal capital allocation o Business restructuring 2.2.2. Value Neutral Diversification • Antitrust regulation • Tax laws • Low performance • Uncertain future cash flows • Risk reduction for firm • Tangible resources • Intangible resources 2.2.3. Value Reducing Diversification • Diversifying managerial employment risk • Increasing managerial compensation Operational relatedness: Sharing Activities Between Business High Low Related Constrained diversification Both operational Corporate relatedness Unrelated diversification Related linked diversification Low High Corporate relatedness: transforming core competencies into business Figure 2: Value Creating Diversification Strategies: Operational and Corporate Relatedness 2.3. Operational and Corporate Relatedness When a company decided to do diversification, it was important to pay attention in relation between core-competencies and operational of the company. Operational relatedness and corporate relatedness are the ways to diversify for creating value for the company. Study about relation of these two things showed how important resources and key-competencies are when company needed to diversify. 2.4. Levels of Diversification (Hill et al, 170: 2007) • Single Business: 95% or more of revenue comes from a single business. • Dominant Business: between 70% and 95% of revenue comes from a single business • Moderate to High Level of Diversification o Related Constrained: less than 70% of revenue comes from the dominant business, and all business share product, technological, and distribution linkages. o Related linked (mixed related and unrelated): less than 70% of revenue comes from the dominant business and there are only limited links between businesses. • Very High Levels of Diversification o Unrelated: less than 70% of revenue comes from the dominant business and there are no common links between businesses. 2.5. Types of Diversification • Related Diversification Diversification into a new business activity is linked to a company’s existing business activity or activities, by commonality between one or more components of each activity’s value chain. Normally, these linkages are based on manufacturing, marketing or technological commonalities. Example: Philip Morris did diversification by acquiring Miller Brewing because there is closed relation between beer and smokers. • Unrelated Diversification Diversification into a new business area has no obvious connecting with any of the company’s existing areas. 2.6. Diversification for Grand Strategy As explained before, diversification may become a variant of corporate-strategy. Diversification together with other variant of strategies might be used by a company to reach its goals. There are two matrixes which connected with diversification. First, was Grand Strategy Selection Matrix and second was Model of Grand Strategy Clusters. In Grand Strategy Matrix we can see that diversification would be chosen by the company with strong external pressure/inducements. In Strategy Cluster Matrix, diversification would be used in slow market-growth. The target of this strategy was to create new-value for the company outside the existing market at this moment. Overcome Weakness Turnaround or retrenchment Divesture Liquidation Internal (redirected resources within the firm) Vertical Integration Conglomerate diversification I II IV III Concentrated growth Market development Product development Innovation Horizontal Integration Concentric diversification Joint venture External (acquisition or merger for resource capability) Maximize Strengths Figure 3: Grand Strategy Selection Matrix (Pierce II & Robinson Jr, 208: 2003) Rapid Market Growth • • • I Strong Competitive Forces IV • • • • Concentrated Growth Vertical Integration Concentric diversification Concentric diversification Conglomerate diversification Joint ventures • • • Reformulation of concentrated growth Horizontal integration Divestiture Liquidation II Weak Competitive Forces III • • • • • Turnaround retrenchment Concentric diversification Conglomerate diversification Divestiture Liquidation or Slow Market Growth Figure 4: Model of Grand Strategy Clusters (Pearce II & Robinson Jr, 210: 2003) 2.7. Growth Strategy: Diversification Definition A strategy based on investing in companies and sectors which are growing faster than their peers. WIKA has already decided to grow as named the roadmap to 2010. In the end of the roadmap, the company hopes to be the excellent company in Southeast Asia with Sales Growth of 36%. Core business is still in construction but it focuses in EPC, Investment and International Construction. From 2002 to 2010 WIKA has gradually changed its business-lines but never leave the construction as a core business. 2.7.1. Ansoff Matrix Igor Ansoff presented a matrix that focused on the firm's present and potential products and markets (customers). By considering ways to grow via existing products and new products, and in existing markets and new markets, there are four possible productmarket combinations. Ansoff's matrix is shown below: Existing Markets New Markets Existing Products New Products Market Penetration Product Development Market Development Diversification Figure 5: Anzoff Matrix 2.7.2. What is the product – Market-Grid - Description The Product/ Market Grid of Ansoff is a model that has proven to be very useful in business unit strategy processes to determine business growth opportunities.The Product/ Market Grid has two dimensions: products and markets.Over these 2 dimensions, four growth strategies can be formed. Four growth strategies in the product/market grid: 1. Market Penetration. Sell more of the same products or service in current markets. These strategies normally try to change incidental clients to regular clients, and regular client into heavy clients. Typical systems are volume discounts, bonus cards and Customer Relationship Management. Strategy is often to achieve economies of scale through more efficient manufacturing, more efficient distribution, more purchasing power, overhead sharing. 2. Market Development. Sell more of the same products or services in new markets. These strategies often try to lure clients away from competitors or introduce existing products in foreign markets or introduce new brand names in a market. New markets can be geographic of functional, such as when we sell the same product for another purpose. Small modifications may be necessary. Beware of cultural differences. 3. Product Development. Sell new products or services in current markets. These strategies often try to sell other products to (regular) clients. These can be accessories, add-ons, or completely new products. Cross-selling. Often, existing communication channels are used. 4. Diversification. Sell new products or service in new markets. These strategies are the most risky type of strategies. Often there is a credibility focus in the communication to explain why the company enters new markets with new products. On the other hand diversification strategies also can decrease risk, because a large corporation can spread certain risks if it operates on more than one market. Diversification can be done in four ways: - Horizontal diversification. This occurs when the company acquires or develops new products that could appeal to its current customer groups even though those new products may be technologically unrelated to the existing product lines.(new products, current market) - Vertical diversification. The company moves into the business of its suppliers or into the business of its customers. (move into firms supplier's or customer's business) - Concentric diversification. This results in new product lines or services that have technological and/or marketing synergies with existing product lines, even though the products may appeal to a new customer group. (new product closely related to current product in new market) - Conglomerate diversification. This occurs when there is neither technological nor marketing synergy and this requires reaching new customer groups. Sometimes used by large companies seeking ways to balance a cyclical portfolio with a non-cyclical one.(new product in new market) There are two types of diversification: - related - unrelated diversification. Related diversification means that the firm remains in a particular industry, but diversify into another type of product to be sold to new markets. Unrelated diversification refers to a situation where the firm completely ventures into a new business area to serve new markets with its new product development. New capital investments are also needed. In this scenario, it would mean that the firm is entering into an industry that it has little experience with limited or no knowledge of the industry. 2.7.3. Selecting a Product-Market Growth Strategy The market penetration strategy is the least risky since it leverages many of the firm's existing resources and capabilities. In a growing market, simply maintaining market share will result in growth, and there may exist opportunities to increase market share if competitors reach capacity limits. However, market penetration has limits, and once the market approaches saturation another strategy must be pursued if the firm is to continue to grow. Market development options include the pursuit of additional market segments or geographical regions. The development of new markets for the product may be a good strategy if the firm's core competencies are related more to the specific product than to its experience with a specific market segment. Because the firm is expanding into a new market, a market development strategy typically has more risk than a market penetration strategy. A product development strategy may be appropriate if the firm's strengths are related to its specific customers rather than to the specific product itself. In this situation, it can leverage its strengths by developing a new product targeted to its existing customers. Similar to the case of new market development, new product development carries more risk than simply attempting to increase market share. Diversification is the most risky of the four growth strategies since it requires both product and market development and may be outside the core competencies of the firm. In fact, this quadrant of the matrix has been referred to by some as the "suicide cell". However, diversification may be a reasonable choice if the high risk is compensated by the chance of a high rate of return. Other advantages of diversification include the potential to gain a foothold in an attractive industry and the reduction of overall business portfolio risk. The product/market grid of Ansoff is a model that has proven to be very useful in business unit strategy processes to determine business growth opportunities. The product/market grid has two dimensions: products and markets. 2.8. What kind of decision will be the best in diversification? What is the basis? 2.8.1. Diversity to unrelated industry Example: Conglomerate PT Astra International Tbk. In 1957, Astra was established as a trading company. Over the course of its development, Astra has formed a number of strategic alliances with leading global players in various industries. Since 1990, the Company had been a go public company, listed on both the Jakarta and Surabaya Stock Exchanges, now known as the Indonesia Stock Exchange with the Company’s market capitalization as of 31 December 2007 stood at Rp 110.5 trillion. Astra now has six core businesses: Automotive, Financial Services, Heavy Equipment, Agribusiness, Information Technology and Infrastructure. At year-end 2007, Astra Group had a workforce of 116,867 people, spread across 130 subsidiaries and affiliates. Table 1: Financial Performance (Rpbn) Automotive Financial services Agribusiness Information technology Heavy equipment and mining Others Total Less elimination Total consolidated Contribution (%) Automotive Financial services Agribusiness Information technology Heavy equipment and mining Others Total 2006 30,259.0 7,567.8 3,758.0 619.0 13,719.6 28.9 55,952.2 (243.0) 55,709.2 54.1 13.5 6.7 1.1 24.5 0.1 100.0 Net revenue 2007 38,318.4 7,310.5 5,961.0 725.6 18,165.6 28.3 70,509.3 (326.4) 70,183.0 54.3 10.4 8.5 1.0 25.8 0.0 100.0 Source: Bahana Securities 2.8.2. Diversity to related-industry Growth (%) 26.6 (3.4) 58.6 17.2 32.4 (2.0) 26.0 34.3 26.0 2006 859.1 727.0 1,198.6 76.7 1,340.1 (10.4) 4,191.2 52.0 4,243.2 20.5 17.3 28.6 1.8 32.0 (0.2) 100.0 Operating profit 2007 Growth (%) 1,717.9 99.9 1,355.6 86.5 2,907.1 142.5 95.1 23.9 2,393.3 78.6 (8.9) (14.4) 8,460.0 101.9 41.5 (20.3) 8,501.5 100.4 20.3 16.0 34.4 1.1 28.3 (0.1) 100.0 Figure 6: Strategies of Related Diversification Timing: The first question to assess is the competitive strength of the firm that is looking to expand. Is the motive to expand an offensive one-- triggered by healthy margins in the core business, and strengths that can be leveraged elsewhere? Or, is it primarily defensive, where a firm is looking to “escape” its declining core? Unfortunately, scope expansions are in most cases not effective in solving the latter predicament; in addition, they are unlikely to leverage any existing strengths of the firm in such a setting. Thus, Bausch and Lomb, the market leader in soft contact lenses, decided to expand away from its core business when growth slowed and competitors attacked with new technologies such as cast molding. The company invested in electric toothbrushes, dental aids, skin ointments, and hearing aids. After several years, and having seen its market share in its core business decline from 40% to 16% (while Johnson and Johnson introduced the idea of disposable lenses), Bausch and Lomb exited many of these noncore businesses and looked to focus on the core again. Companies in similar situations often do well not by looking outward but inward: invariably, a more effective solution is to identify ways to solve the problems in, and “profit from the core”1, as companies like Harley-Davidson have done. Industry attractiveness: Structurally, how attractive is the new business arena being considered for expansion? Do incumbents enjoy healthy margins or are competition likely to be fierce and profits meager? The familiar “five forces” analysis is useful not only in predicting industry profitability but, more importantly, in identifying the various sources of competition that the company is likely to face. Specifically, it is useful to examine whether and how the firm’s intended entry strategy can effectively combat the likely competitive forces. For example, consider the furniture industry. An entrant that seeks to exploit scale economies by automating manufacturing processes is likely to be more vulnerable to the industry’s cyclical dynamics since automation would increase the fraction of its costs that are fixed. On the other hand, the “infinite variety” in designs that characterizes the industry also makes it difficult for manufacturers to develop brands with consistent identities and carve out a high-end position. Scope economies with existing business: The viability of an entry strategy leaves unanswered the question of which firm is in the best position to pull off such a strategy. Specifically, what are the scope economies or synergies with the firm’s existing businesses: might expansion into the new businesses either leverage particular strengths from the existing ones, or benefit them in turn? Exhibit 1 illustrates the different sources of such synergies. These might arise from cost-sharing: for example, the centralization of procurement, combination of staff functions, economies in distribution and logistics, or common production platforms. Or, they might enhance revenues of the combined businesses by mechanisms such as cross-selling, bundling, and one-stop shopping. While cost synergies are often the driving force in scope expansions and mergers, the search for revenue synergies has become more common as well. For example, several mergers between high-end and low-end machine tool manufacturers in the last decade were driven by the desire to combine breadth of product offerings in “one-stop shopping” for industrial customers. Health care delivery has seen the emergence of multi-business firms like Covenant Health Systems, whose outpatient ambulatory care centers have led to more referrals for more profitable inpatient care. And, cross-selling motivations have resulted in financial services companies like Charles Schwab expanding to offer products ranging from money market funds to investment advisory services. Each of the synergies described above stems from the sharing of activities by different businesses. Activity analysis is a useful, and concrete, approach to evaluating scope economies. At the same time, it is useful to keep in mind that tangible activity coordination is not the only source of synergies. Often, synergies can arise from the sharing of resources or intangible skills. These might include a common brand, reputation, specific knowledge and expertise, managerial talent, systems and processes, values, or even a common culture. As these examples illustrate, resource sharing, while intangible, can be no less important. More importantly, it suggests a different way to evaluate the question of “relatedness” between any two businesses: rather than simply ask whether the products being sold by the businesses are related, one ought to also examine whether there are common competencies required to succeed in these businesses. This can often lead to counterintuitive, but no less powerful, expansion decisions. For example, Honda expanded into cars, motorcycles, lawn mowers, and generators, leveraging its competence in engines and power trains. Canon expanded into copiers, laser printers, and cameras, exploiting its competencies in optics, imaging, and processor controls. And, Minebea expanded from ball bearings to semiconductors, leveraging its competence in miniaturized manufacturing. Each of these examples suggests a useful principle to keep in mind when evaluating resource sharing benefits: these benefits are most compelling when the competencies in question are not only (i) important drivers of performance in that business, but they are also (ii) distinctive or unique to the firm. Organizational mechanisms for coordination: Having examined the potential sources of synergies, one ought to scrutinize how exactly they will be realized. Specifically, what organizational mechanisms need to be put in place to ensure this? Firms often deem this question to fall under the domain of “implementation”. However, failing to think through the organizational choices and changes that accompany any scope expansion is a common reason why mergers fail. Consider, for example, Saatchi and Saatchi’s foray into the consulting businesses in the 1980s. Regardless of whether one viewed the potential synergies between advertising and consulting services to be large or small, the firm’s approach to organizational integration proved to be the decisive factor in its failed expansion. Specifically, its approach of “front-end separation, back-end integration”— while successful in integrating its earlier advertising acquisitions—was flawed here, in light of the differences between the “push based” budgeting systems common in consulting and the “pull based” approach intrinsic to advertising. The nature of organizational coordination will of course be informed by the types of synergies identified above. For example, the incentives to cross-sell two products will be greater when there is a common sales-force for both products than with different ones for each. Or, the ability to leverage company-wide competencies is often easier with a functional organizational structure than with a divisional one. And, in addition to the role of the formal organizational structure in facilitating (or impeding) coordination, informal mechanisms can often be quite powerful in “boundary-spanning” as well: company-wide norms, values, and cultures. Recognizing, and acting on, these organizational changes can be critical to realizing the benefits of scope in practice. Ownership: Extracting the rents from expansion into a new arena does not require that companies fully own the new business as well. The choice of ownership (i.e., where the boundaries of the firm should be drawn) is relevant for most horizontal expansion decisions, but is particularly central to firms’ decisions on whether to expand into adjacent parts of the value chain—the vertical integration question. Therefore, although the key insights behind the logic of ownership are quite general, they are discussed, in what follows, largely in the context of the choice to vertically integrate. Source: Adopted from Bharat N. Anand, Strategies of Related Diversification (2005) Example: Engineering and Construction: PT Wijaya Karya (Persero) Tbk. Table 2: Growth of order Source: company Table 3: Financial Performance Year to 31 Dec Revenue (IDRb) EBITDA (IDRb) Net Profit (IDRb) EPS (IDR) Growth (%) P/E (x) BVPS (IDR) P/BV (x)221 EV/EBITDA (x) ROA (%) ROE (%) Dividend (IDR) Dividend Yield (%) 2006 3.049 135 94 16 37.3 36.7 69 8.6 25.6 3.5 23.3 13 2.2 Source: company, Bahana Estimates Table 4: Construction Company Margin 2007 4.285 242 129 22 37.5 14.5 221 1.4 3.4 3.1 10.0 4.8 1.5 2008F 6.450 281 152 26 17.8 12.3 240 1.3 4.7 2.7 10.8 6.6 2.1 WIKA : fully diversified; ADHI : partly diversified; TOTL : focus TOTL net margin was higher than the others when the construction growth was high in 2007. On the other hand when oil prices increased significantly since the beginning of 2008, the cost of construction company raised and could possibly ruin its profit as shown at above figure. As escalation clause on cost of construction only applicable for multi year projects and mostly for companies with exposures to government projects, the benefited companies would be WIKA and ADHI. WIKA would be the most benefited because of it diversified business model to reduce the volatility in margin as a result of the uncertain raw material cost and global financeturmoil. 2.8.3. Do not diversify From the figure below, there are many other industries which have interesting growth in its own business. It means even focusing in one line of business; it will still have opportunity to grow in its industries. Table 5: The growth of industry in Indonesia Indonesia Banking Mining & Energy Telecom Consumer & Retail Automotive Cement** Plantations Heavy Equipments Property Oil & Gas services Construction Toll Road Poultry Mkt Cap US$mn 115,367 30,836 29,616 19,487 9,892 7,931 5,296 3,944 3,545 2,358 651 270 280 79 Source: Bahana Securities 05A 2.7 -19.5 16.2 15.9 -10.4 0.9 44.7 -6.1 -4.4 -0.1 N/A 7.1 22.8 N/A EPS Growth (%) 06A 07A 43.1 50.9 68.4 52.0 26.5 96.4 -32.0 -16.4 36.8 -10.9 -8.1 N/A 35.6 50.3 480.5 23.0 107.6 26.1 10.3 58.7 45.3 112.2 59.5 3.6 3.1 19.8 -29.5 -14.7 08F 27.1 05A 20.6 21.9 18.7 33.8 23.8 19.0 27.4 8.3 4.4 27.7 26.7 47.0 13.0 55.3 25.6 31.8 25.6 11.0 10.3 57.6 N/A 55.4 20.7 59.0 13.2 -18.2 11.0 ROE (%) 06A 07A 22.5 27.2 18.3 30.7 32.0 6.2 16.6 15.3 23.7 20.4 8.5 15.5 22.6 16.8 39.9 18.7 45.3 31.9 6.0 22.2 18.5 35.9 26.0 6.4 14.4 12.8 5.8 26.7 08F 26.3 19.5 40.1 30.6 6.4 23.7 20.7 39.7 27.7 6.7 20.2 16.9 8.1 18.0