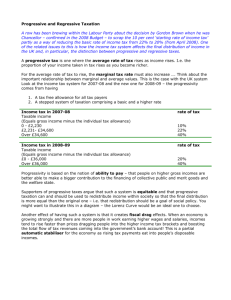

AP Microeconomics – Chapter 16 Outline I. Learning objectives—In

advertisement

AP Microeconomics – Chapter 16 Outline I. Learning objectives—In this chapter students should learn: A. The main categories of government spending and the main sources of government revenue. B. The different philosophies regarding the distribution of a nation’s tax burden. C. The principles relating to tax shifting, tax incidence, and the efficiency losses caused by taxes. D. How the distribution of income between rich and poor is affected by government taxes, transfers, and spending. II. Government and the Circular Flow A. Figure 16.1 shows the circular flow model with the addition of the government sector. B. Modifications to the Figure 2.2 Model 1. Flows (5) through (8) illustrate that government makes purchases in both the product and resource markets. 2. Flows (9) and (10) illustrate that the government provides public goods and services to households and businesses. 3. Flows (11) and (12) illustrate that government receives taxes from and distributes subsidies to households and businesses. C. These flows suggest ways that the government might alter the distribution of income, reallocate resources, and change the level of economic activity. AP Microeconomics – Chapter 16 Outline III. Government Finance A. Government Purchases and Transfers 1. Government purchases require the use of resources to produce products and are part of the domestic output. 2. Transfer payments do not use resources or create output; they include Social Security benefits, welfare payments, veterans’ benefits, and unemployment compensation. 3. Transfer payments have increased as a percentage of national output since 1960, while government purchases as a percentage of output have declined (Figure 16.2). B. Government revenues come from three sources: taxes, proprietary income, and funds borrowed by selling bonds to the public. C. Deficit spending occurs when government spending exceeds revenues in a given time period. D. One result of deficit spending can be crowding out, when government crowds out private sector borrowing for investment, which can reduce potential long‐run economic growth. IV. Federal Finance A. Expenditures emphasize four important areas (Figure 16.3): AP Microeconomics – Chapter 16 Outline 1. Pensions and income security 2. National defense 3. Health 4. Interest on the public debt B. Receipts come from several sources (Figure 16.3). AP Microeconomics – Chapter 16 Outline 1. Personal income tax is the primary source of federal revenue. a. The federal personal income tax is progressive. People with higher incomes pay a higher percentage of their income in tax than do people with lower incomes. b. A marginal tax rate is the rate at which the tax is paid on each additional unit of taxable income (Table 16.1). c. The average tax rate is the total tax paid divided by total taxable income. d. A tax whose average tax rises as income increases is progressive. 2. Payroll taxes to fund Social Security and Medicare are a close second source of revenue. 3. Corporate income taxes on profits are the third largest source of revenue. 4. Sales taxes are placed on a wide range of products and are generally added to the final bill at the time of sale. Excise taxes are placed on specific products, such as alcoholic beverages, tobacco, and gasoline, and generally are hidden from the consumer in the price of the product. AP Microeconomics – Chapter 16 Outline C. Global Perspective 16.1 shows that the United States, Mexico, Turkey, South Korea, and Canada enjoy relatively low tax burdens. European nations (particularly Scandinavian countries) have relatively high burdens. V. State and Local Finance A. State governments have different mixes of revenues and expenditures than the federal government has (Figure 16.4). 1. State revenues primarily come from sales and excise taxes and secondly from personal income taxes. Corporate income taxes and license fees account for most of the rest of state revenues. 2. States vary widely in terms of revenue sources; seven states have no personal income tax, and most states rely on lotteries and intergovernmental revenues. AP Microeconomics – Chapter 16 Outline 3. State spending goes primarily for education, welfare, highways, health and hospitals, and public safety. B. Local revenues and spending differ from the state and federal levels (Figure 16.5). 1. Local revenue is derived primarily from property taxes, while sales and excise taxes add to revenue. 2. Local spending is primarily for education, while welfare, health and hospitals, public safety, housing/parks/sewage, and streets and highways are other major spending areas. 3. The gap between local tax revenues and spending is largely filled by grants from state and federal government (referred to as “intergovernmental grants”). C. CONSIDER THIS … State Lotteries: A Good Bet? 1. States raise billions of dollars through state lotteries, though they remain controversial. 2. Critics argue that it is morally wrong for states to sponsor gambling, that lotteries promote compulsive gambling and attract criminals, and that lotteries take advantage of lower‐income families by promoting a message that luck—rather than education and hard work—are the route to wealth. 3. Defenders argue that lotteries are preferable to taxes because they are voluntary and relatively painless, and that lotteries compete with illegal gambling, helping to reduce organized crime. VI. Local, State, and Federal Employment A. The largest numbers of federal jobs are in national defense (26%) and the Post Office (26%). Other major categories include hospitals and health, natural resources, police, and financial administration (Figure 16.6). C. The largest numbers of state and local jobs are in elementary/secondary education (41%) and higher education (12%). Other major categories include hospitals and health, police, administration, and corrections (Figure 16.6 – see next page). AP Microeconomics – Chapter 16 Outline VII. Apportioning the Tax Burden A. Benefits Received versus Ability to Pay 1. The benefits‐received principle asserts that households and businesses should be taxed in relationship to the services they receive. For example, gasoline taxes are earmarked for highway construction and maintenance. a. How can the government determine the benefits households and firms receive from national defense, education, and other public goods and services? b. The principle cannot be applied to income redistribution programs; welfare recipients and the unemployed would have to pay for their benefits, defeating the purpose of the programs. 2. The ability‐to‐pay principle asserts that the tax burden should rest more heavily on those with greater income and wealth. The rationale is that those people with more income or wealth will value their marginal dollars less than those with low incomes, where each dollar is very meaningful. A problem with this principle is that there is no scientific way to make utility comparisons among individuals to determine different abilities to pay among households. B. Progressive, Proportional, and Regressive Taxes 1. A tax is progressive if its average rate increases as income increases; the tax grows absolutely and proportionately with income. 2. A tax is proportional if its average rate remains the same as income increases; the tax payment grows absolutely with income, but remains in the same proportion to income. 3. A tax is regressive if its average rate declines as income increases; the tax may or may not increase in the absolute amount, but it declines in proportion to income. C. Applications 1. The federal personal income tax is mildly progressive, with marginal tax rates ranging from 10 to 35 percent in 2010. Certain deductions that favor high‐income groups erode the progressivity of this tax. AP Microeconomics – Chapter 16 Outline 2. Sales taxes are not as proportional as they seem, if they are on all goods. A general sales tax is regressive because, although everyone pays the same percentage on expenditures, the rich tend to spend a much smaller fraction of their incomes, while the poor may spend all of their incomes. Therefore, the rich will pay a smaller overall proportion of their income in sales taxes. 3. The federal corporate income tax is essentially a flat‐rate tax with a set rate. But if it is passed on to consumers in the form of higher prices, it may actually be regressive in its impact. 4. Payroll taxes are regressive. The Social Security portion of the tax (6.2 percent) is not applied to income above a certain level ($106,800 in 2010). On the other hand, the Medicare tax (1.45 percent) is applied to all wage income. A person making $106,800 pays 7.65 percent ($8170.20) of his or her wage income; a person making $213,600 pays only 4.6 percent ($9718.80) of his or her wage income. Payroll taxes are even more regressive than they appear, because they are only levied on wage and salary income; interest and dividends, rents, capital gains, and other sources of income are not subject to payroll taxes at all. 5. Property taxes tend to be regressive because landlords pass along this cost to tenants who have lower incomes; housing costs are a larger proportion of income for the poor than for the rich, so economists estimate that the property tax on that housing would end up being a greater proportion of low incomes than of high incomes. D. CONSIDER THIS … The VAT: A Very Alluring Tax? 1. A value‐added tax places a tax on the difference between the value of raw materials and the value of the product a firm sells—the value the firm adds to the product. 2. Firms would pass the tax on to consumers in the form of higher product prices. 3. Proponents argue a VAT tax would increase saving and investment, because consumption, rather than saving, would be taxed. 4. Opponents argue that VAT taxes are a regressive hidden tax that can lead to excessive tax rates because it is so easy to raise the tax. Opponents also argue that VAT taxes do not encourage saving and investment, because the future consumption households are saving for would also be taxed under the VAT tax. VIII. Tax Incidence and Efficiency Loss A. Tax incidence—the degree to which a tax falls on a particular person or group. 1. The division of the burden is not obvious. Figure 16.7 (see next page) shows the impact of a $2 per‐bottle tax on wine that was priced at $8 per bottle before the tax. AP Microeconomics – Chapter 16 Outline 2. S is the no‐tax supply situation and St is the after‐tax supply curve. The new equilibrium price rises to $9, not $10 as one might expect with the $2 tax. a. Consumers pay $1 more per bottle. b. Producers receive $1 less per bottle. 3. In this example, consumers and producers share the burden of the tax equally. The incidence is not completely on either one. B. Elasticities of demand and supply explain the incidence of an excise or sales tax. 1. Given supply, the more inelastic the demand for the product, the larger the portion of the tax shifted to consumers (Figure 16.8b). AP Microeconomics – Chapter 16 Outline 2. Figure 16.8a shows the situation if demand is more elastic, where a larger portion of the tax is borne by the producer. The decline in equilibrium quantity is smaller with an inelastic demand, so governments place excise taxes on such products (cigarettes, gasoline, and alcohol) to maximize revenue. 3. Given demand, the more inelastic the supply (Figure 16.9b), the larger the portion of the tax borne by producers or sellers. Figure 16.9a shows the situation if supply is more elastic. The decline in equilibrium quantity is smaller with an inelastic supply. C. Efficiency Loss of a Tax 1. Figure 16.10 illustrates the concept of efficiency loss, which occurs as a result of an excise tax or sales tax. The efficiency loss (deadweight loss) is the sacrifice of net benefit to society because consumption and production of the taxed product are reduced below their allocatively efficient levels. 2. Elasticities play a role in determining the extent of the efficiency loss. Other things equal, the greater the elasticities of supply and demand, the greater the efficiency loss of a particular tax. 3. Qualifications to the analysis reflect the position that other goals of tax policy may be more important than the goal of minimizing efficiency losses from taxes. a. Redistributive goals—Excise taxes placed on luxury items in 1990 resulted in efficiency losses, but the benefits from redistributing income from the wealthier consumers who buy luxury items may have been worth the loss in efficiency. However, these luxury taxes caused an increase in unemployment due to lower product sales and have been repealed or expired. b. Reducing negative externalities—If alcohol and tobacco consumption are reduced as a result of excise taxes, the taxes may have socially desirable consequences. D. Probable Incidence of U.S. Taxes 1. The personal income tax generally falls on the individual, except for those who can control the price of their labor services and pass on the cost of the tax through higher fees. AP Microeconomics – Chapter 16 Outline 2. The workers’ portion of payroll taxes are borne entirely by the workers, because they cannot shift those taxes to others. Employers also shift part of their portion of the payroll tax to workers in the form of lower pre‐tax wages. 3. The incidence of the corporate income tax is uncertain. Some corporations may be able to shift the burden by charging higher prices; others may find that increasing the price would reduce profitability, so the burden is then borne by stockholders in lower dividends or workers in reduced wage growth. 4. Excise taxes can be shifted to the consumer where demand is inelastic. This is true generally with the small range of products on which excise taxes are levied (gasoline, cigarettes, and alcohol). However, because sales taxes cover such a wide range of products, sales taxes tend to be borne entirely by the consumer. 5. The incidence of property taxes may fall on the property owner, but in the case of rental and business property, the tax would be largely shifted onto the tenant or the customer. 6. Global Perspective 16.2 indicates that the United States is less dependent upon sales and excise taxes than are many other industrialized nations. D. Table 16.2 summarizes the discussion of the shifting and incidence of taxes. AP Microeconomics – Chapter 16 Outline IX. The U.S. Tax Structure A. It is difficult to determine the overall progressivity or regressivity of the American tax structure because some taxes can be shifted to others. B. The federal tax system is progressive. 1. In 2007, the average federal tax rate for the 20 percent of taxpayers with the lowest incomes was 4.0 percent. The average tax rate for the 20 percent of the taxpayers with the highest incomes was 25.1 percent. The tax rate was 26.7 percent for the top 10 percent of taxpayers and 29.5 percent for the top 1 percent of taxpayers. 2. This progressivity is offset by the Social Security tax, which is regressive. Because of the cap of $106,800, taxpayers who earn more pay a lower percentage of their income in tax than do lower and middle income earners. C. State and local taxes are largely regressive. Both sales and property taxes fall as a proportion of income when income rises. D. Overall, the American tax structure is slightly progressive. The American system of taxes and transfer payments does reduce income inequality and is estimated to quadruple the incomes of the poorest one‐fifth, which makes the tax‐transfer system more progressive than the tax system alone. X. LAST WORD: Taxation and Spending: Redistribution versus Recycling A. Effective redistribution of income requires that the taxes taken from the rich flow to the poor through spending on goods, services, and programs that are used primarily by the poor. B. Economic research confirms that the rich do pay a larger percentage of their income in taxes than the poor, and spending is concentrated on programs that benefit the poor, such as welfare, subsidized health care, public education, and jobs programs.