Answers to Sample Long Free

advertisement

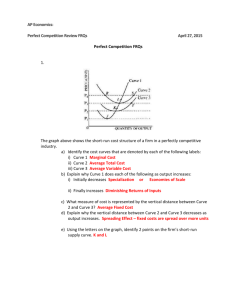

UNIT 3 Microeconomics LONG FREE-RESPONSE SAMPLE QUESTIONS Answer Key Answers to Sample Long Free-Response Questions *1. In a particular product market, there is only one seller and there are significant barriers to entry. (A) Explain how this firm determines its equilibrium output and price. (B) Explain whether this firm is producing the economically efficient level of output. In your answer include a brief definition of economic efficiency. Grading Rubric: Part (A) = 6 points, Part (B) = 3 points Part (A) Components of a good answer: (i) Because the firm is a monopoly, it faces a downward-sloping demand curve. (ii) Because its demand curve is negatively sloping, its marginal revenue curve will be more steeply sloping downward. (iii) Bring in marginal cost to determine output at MR = MC . (iv) Recognize that the profit-maximizing point is MR = MC. (v) Read price from the demand curve at the output where MR = MC. In allocating points for Part (A), give 1 point for each of (i) through (iv) and 2 points for (v). Part (B) Components of a good answer: (i) A definition of economic efficiency (either allocative efficiency requires P = MC or productive efficiency is producing at minimum ATC) (ii) Correctly relating the definition to the monopoly situation. A monopolist is not efficient by either definition. In allocating points for Part (B), give 1 point for the efficiency definition and 2 points for correctly relating the monopolist situation to the definition of efficiency. Special situations: (1) There is a possibility that an answer will have efficiency, meaning that a producer operates at the least ATC for a given level of output, and hence the monopolist could be productively efficient. That’s okay! Give 3 points. (2) Answer states that the monopolist is not efficient because it produces too little output and charges too high a price, or the monopolist restricts output. Give 1 point for this line of “reasoning.” (3) If a rudimentary concept of inefficiency is recognized, give 1 point. * Actual free-response question from a past AP test. Reprinted by permission of the College Entrance Examination Board, the copyright owner. For limited use by NCEE. Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y. 221 UNIT 3 Microeconomics LONG FREE-RESPONSE SAMPLE QUESTIONS Answer Key *2. Assume that initially, a perfectly competitive industry is in long-run equilibrium. (A) For the typical profit-maximizing firm in this industry, explain the following: (i)i How the firm determines its level of output (ii) What the level of profit is and why it is at this level (B) A change occurs that reduces the variable costs of production for all firms in this industry. Explain how and why this decrease in variable costs affects each of the following in the short run: (i)i The typical firm’s level of output (ii) The industry price and level of output Grading Rubric: Part (A) = 4 points, Part (B) = 5 points Part (A) Components of a good answer: (i)ii Identification of the output at which price or marginal revenue equals marginal cost at the profit-maximizing output, and (ii)i Identification of long-run equilibrium as zero economic profits (or only normal profits — the exact wording is not important) and an explanation of why there are zero economic profits in long-run equilibrium. The allocation of 4 points for Part (A) would be 2 for (i), 1 for identification of the zero-profit condition and 1 for the explanation of why zero profits exist in long-run equilibrium. Part (B) Basic points the answer should make: (i)ii The reduction in variable costs would reduce marginal cost, which would cause marginal revenue to equal marginal cost at a higher level of output (in other words, the student should use a marginal revenue and marginal cost argument to motivate the increase in the firm’s output caused by the reduction in variable costs). (ii)i The increase in output of the individual firms will result in an increase in industry supply, and (iii) The increase in industry supply will cause industry output to increase and thus industry output to fall. The allocation of the 5 points for Part (B) would be 2 for (i), 1 for (ii) and 2 for (iii). If the student simply says that a decrease in costs will cause a producer to increase her output, that would be only 1 point for (i). A student who says that all of this will increase the output of the product and reduce the price of the product without using an increase in supply to motivate these events would receive only 1 point for (iii). If the student starts the answer with a nice clear graph for a monopolist and proceeds to answer the question as if it applied to a monopoly instead of to a perfectly competitive industry, 2 would be the maximum possible number of points that could be given for an answer, and these 2 points would be for an identification of the MR = MC position as a maximum profit position. The rest of the question would not effectively apply to a monopolist. * Actual free-response question from a past AP test. Reprinted by permission of the College Entrance Examination Board, the copyright owner. For limited use by NCEE. 222 Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y. UNIT 3 Microeconomics LONG FREE-RESPONSE SAMPLE QUESTIONS Answer Key *3. A retail industry is perfectly competitive and in long-run equilibrium. (A) The wholesale price increases. Explain what happens initially to the retail industry’s output and price. (B) In reaction to the changes above, the government imposes a retail price ceiling on the product at its original price level. What will be the effect of the price ceiling on the quantity demanded and supplied in the retail industry? (C) Given the effect of the price ceiling on the typical firm’s profits, will firms in the retail industry have an incentive to enter or exit this industry in the long run? Explain. Grading Rubric: Each part is worth 3 points. Part (A) The components of a good answer include (i)ii an increase in factor input prices increases the cost of production and shifts the industry supply curve to the left (upward) (ii)i equilibrium quantity decreases and (iii) equilibrium price increases. Allocate 1 point for each correct part. There does not have to be an explicit recognition that the wholesale price is a cost. Part (B) Components of a good answer: (i)ii Recognizes that the quantity demanded is greater (movement along the demand curve) (ii)i Recognizes that there is movement along the supply curve (decrease in the quantity supplied) (iii) Recognizes that what happens in (i) and (ii) creates a disequalibrium situation, which could be identified as a shortage or excess demand. The precise language is not crucial. What is important is that the answer recognizes that the price ceiling has changed an equilibrium situation into one of disequalibrium. Allocate 1 point for each correct part. Special cases: (1) If merely shortage is mentioned, give it 1 point. (2) If the standard price ceiling diagram indicating a shortage or disequalibrium or demand/supply imbalance is given, give the answer 3 points. * Actual free-response question from a past AP test. Reprinted by permission of the College Entrance Examination Board, the copyright owner. For limited use by NCEE. Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y. 223 UNIT 3 Microeconomics LONG FREE-RESPONSE SAMPLE QUESTIONS Answer Key Part (C) Components of a good answer: (i)i There is recognition that, since originally the industry was in long-run equilibrium, the increase in costs coupled with the price ceiling results in losses (not merely a decrease in profits). (ii) The losses will drive firms out of the industry (firms will exit). Allocating the points: (1) If the answer indicates that profits are lower and that firms will exit the industry, give 1 point. (2) If the answer indicates that the firms are earning less than normal profits (or economic losses) as the result of the price ceiling and hence will exit the industry in the long run, give 3 points. (3) If the answer indicates that firms will exit and states that more than profits have declined, such as “the firm is losing money” or “the firm can now do better than someone else,” then 2 points is an appropriate score. (4) If there is a general statement about exit or entry into an industry correctly related to the profit/loss situation, give 1 point. *4. A perfectly competitive manufacturing industry is in long-run equilibrium. Energy is an important variable input in the production process, and therefore the price of energy is a variable cost. The price of energy decreases for all firms in the industry. (A) Explain how and why the decrease in this input price will affect this manufacturing industry’s output and price in the short run. (B) What will be the short-run effect on price, output and profit of a typical firm in this manufacturing industry? Explain. (C) Will firms enter or exit this manufacturing industry in the long run? Why? Grading Rubric: Basically the point distribution is 3 points for Part (A), 4 for Part (B) and 2 for Part (C). Part (A) The industry’s supply curve shifts to the right, resulting in an increase in equilibrium output and a decrease in equilibrium price. The supply curve shifts to the right because of the decrease in input cost (energy prices). 1 point: An explanation that the industry supply curve shifts to the right because of a decrease in costs 1 point: Price declines as a result. 1 point: Quantity increases as a result. * Actual free-response question from a past AP test. Reprinted by permission of the College Entrance Examination Board, the copyright owner. For limited use by NCEE. 224 Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y. UNIT 3 Microeconomics LONG FREE-RESPONSE SAMPLE QUESTIONS Answer Key Part (B) For the firm: The price decline from the industry carries over to the firm, the MC curve must shift to the right, average costs must decline, profit-maximizing output must increase. The profit situation depends on how the student draws the curves. (Yes, I know it depends on the elasticity of the industry demand curve, but they do not!) 1 point: The firm, as a price taker, has a lowered price equivalent to the decrease in industry price. 1 point: Firm produces an increased quantity at MR = MC, as indicated by the new marginal cost curve. 1 point: Explains why the marginal cost curve has shifted downward (to the right). 1 point: Coherent (consistent) statement about the firm’s profits, i.e. ■ The firm may show an economic profit if price decreases less than average cost decreases OR ■ Profits may be uncertain since both price and average cost decrease OR ■ Profits decrease since the price decrease is greater than the average cost decrease, but this condition still requires that output increase. The maximum points for Part (B) are 2 if the MC curve doesn’t move!!! Part (C) Profit situation must be consistent with Part (B) and explanation include entrance if economic profits, uncertainty if profit situation is uncertain and exit if losses. 1 point: Impact on isndustry, whether firms enter, exit or is uncertain is consistent with previous discussion. 1 point: Correct and consistent explanation for assertion about profits *5. Peaches and nectarines are substitute goods, and both are produced under conditions of competitive long-run equilibrium. (A) Joyce, a producer in the peach industry, discovers a technological breakthrough that reduced only the cost of producing peaches. Explain how the change in technology will affect each of the following for Joyce. (i)ii Quantity of peaches produced (ii)i The price of peaches (iii) Short-run profits (B) Now assume that all other peach-producing firms adopt the new technology. Explain how the adoption of the new technology will affect each of the following in the peach-producing industry. (i)i The price of peaches (ii) Quantity of peaches produced * Actual free-response question from a past AP test. Reprinted by permission of the College Entrance Examination Board, the copyright owner. For limited use by NCEE. Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y. 225 UNIT 3 Microeconomics LONG FREE-RESPONSE SAMPLE QUESTIONS Answer Key (C) This new technology is not applicable to the production of nectarines. Explain how the changes that occurred in the peach industry will affect each of the following in the nectarine industry. (i)i The price of nectarines (ii) Quantity of nectarines Grading Rubric: Part (A) = 3 points The technological breakthrough, which reduces the costs of producing peaches, lowers the average total cost curve and marginal cost curve, resulting in a greater output at the same price. The reduction in average costs, the increase in Joyce’s production and the price remaining constant combine to increase short-run profits. 1 point: An explanation that costs have decreased, shifting the marginal cost curve and resulting in a new profit-maximizing higher level of output 1 point: Price remains constant because of perfect competition. Thus, Joyce cannot affect the market price. 1 point: The student must show, convincingly, that short-run profits increase. One of the following explanations is acceptable. ■ Price is constant and costs decrease. ■ Costs have decreased while total revenue has increased because of constant price and increased input. ■ If the student has indicated above that price has decreased, then the student must argue that average costs decrease more than price decreases (or equivalent) to get an increase in Joyce’s profits. Grading Rubric: Part (B) = 2 points The new technology spreads to the entire peach industry, resulting in a rightward shift of the industry supply curve. Price decreases and quantity increases. 1 point: For indicating graphically or verbally that the industry supply curve shifts to the right. 1 point: For equilibrium price and quantity effects. 1/2 point for price decrease and 1/2 point for quantity increase Grading Rubric: Part (C) = 2 points Given that peaches and nectarines are substitutes, a decrease in the price of peaches results in a decrease in the demand for nectarines. A leftward shift in the demand curve for nectarines results in a decrease in the equilibrium price and quantity. 1 point: For a decrease in demand resulting from the price decrease in peaches and the fact that peaches and nectarines are substitutes. The reason must be given. 226 1/2 point: Decrease in nectarine equilibrium price 1/2 point: Decrease in nectarine equilibrium quantity Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y. UNIT LONG FREE-RESPONSE 3 Microeconomics SAMPLE QUESTIONS Answer Key *6. In the country of Lola, sugar had always been produced in a perfectly competitive industry until a dictator seized power and monopolized the production of sugar. (A) Draw a graph that shows the output and price the monopolist would choose to maximize profits. COSTS/REVENUE MC P D MR Q QUANTITY The people of Lola revolt, imprison the dictator and repeal the law restricting the number of sellers of sugar. (B) Explain two conditions that might lead to an increase in the number of sugar sellers after the repeal of the law. Conditions that might lead to an increase in the number of sellers: (i)ii Reduction in the barriers to entry (ii)i Profits that were earned by the monopolist (iii) Returning property rights to original owners Grading Rubric: 2 points 1 point: For each correct condition, up to a maximum of 2 points (Appealing but irrelevant responses such as technological progress, subsidies and population growth are not acceptable.) (C) Describe how an individual seller would determine the profit-maximizing output level of sugar if the sugar industry were perfectly competitive. An individual will determine the profit-maximizing output by equating marginal revenue to marginal cost (MC = MR). For a competitive firm, price equals marginal revenue (P = MR). Price is determined in the market or industry and is not determined by the individual seller. Merely asserting that the firm is a price taker is insufficient for credit. * Actual free-response question from a past AP test. Reprinted by permission of the College Entrance Examination Board, the copyright owner. For limited use by NCEE. Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y. 227 UNIT 3 Microeconomics LONG FREE-RESPONSE SAMPLE QUESTIONS Answer Key Grading Rubric: 2 points 1 point: Recognizing that output is produced where MC = MR 1 point: Recognizing in some form that P = MR (D) Given your answers in Parts (A) and (C), is the repeal of the law likely to make the sugar industry more efficient? In your explanation, be sure to include an explanation of economic efficiency. Under perfect competition, the industry is operating more efficiently. Economic efficiency includes having P = MC (allocative efficiency) and P = min ATC (production efficiency). Grading Rubric: 2 points 1 point: Some correct definition of economic efficiency (P = MC or P = min ATC) 1 point: Correct explanation that the firm will operate where P = MC and at min ATC 228 Advanced Placement Economics Teacher Resource Manual © National Council on Economic Education, New York, N.Y.