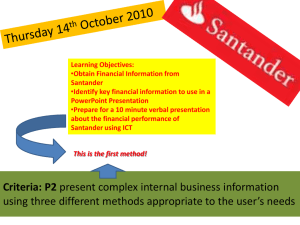

listing prospectus dated november 26, 2014 santander commercial

advertisement