Exporters product mix across markets: the fickle fringe and

Exporters product mix across markets: the fickle fringe and the stable core

∗ e

†

, Angelo Secchi

◦

, and Chiara Tomasi

‡

†

PSE - University of Paris 1 and CEPII

◦

PSE - University of Paris 1 and LEM

‡

University of Trento, LEM and Banque de France

First Draft - 29 May 2015

Present Version - December 4, 2015

Please do not circulate

∗

The present work has been possible thanks to a research agreement between the Italian Statistical Office (ISTAT) gratefully acknowledges the Paris School of Economics for granting him a ’Residence de Recherche’ for the period

2012-2013. We also acknowledge financial support from the Institute for New Economic Thinking, INET inaugural grant #220.

1

1 Introduction

It has long been recognized that business firms in advanced economies tend to show a remarkable degree of product diversification and many arguments have been made about why firms diversify.

Synthetically these arguments can be organized around two main dimensions: technology and demand. With respect to technology, economies of scope generated by excess capacity in purchased and generated productive factors, including organizational knowledge, have been traditionally considered the main motivation for a firm to diversify its production.

1

Regarding demand, it has been found that complementarities and strategic products bundling/tying to exploit price discrimination or to leverage market power across different markets are important diversification motives. More recently the development of the so called “product platform strategies” has shown that technology and demand may operate jointly in shaping a firm’s diversification dynamics to improve production efficiency and to be more reactive in meeting customers needs especially in segmented markets.

2

However, it has been also suggested that there exist limits to this tendency to diversification. Indeed, demand or resource cannibalization effects and the tendency to move away from the core of its technological competences, hence loosing competitive advantage, bound the number of products a firm is able to efficiently produce and sell on the market. This literature on multi-product firms provides two messages that are important for our work. First, the composition of output in terms of products, that is the product-mix, emerges as a crucial factor in determining a firm’s performance in terms of productivity and profitability. Second, the structure of the product-mix should be viewed as the outcome of a strategic choice embedding both technology and demand related factors.

The present paper suggests that export markets provide an ideal laboratory to study multiproduct firms’ behavior. Indeed, a large empirical evidence has recently shown that, as for domestic markets, international markets are dominated by largely diversified firms typically exporting more than one product in more than one destination. Further, traditional data used in international trade are based on custom transactions and record rich information at the product level and for any destination market a firm is active in, features very rarely present in dataset covering the domestic market. Accordingly, the aim of this work is to investigate exporters’ product-mix, their composition, and the main factors driving their variation across destination countries with a special emphasis on the role of demand and of market structure.

To better motivate our study we start with an example and we consider a typical firm producing electrical motors, shipping 16 different products to 20 different destinations.

3

The combinations of

1 This interpretation requires that the external transfer of this excess capacity is subject to some form of market failure.

2

For example, Volkswagen is reducing the unit cost of its Golf model by producing also Tiguan and Touran using the same platform, known as “PQ35”. At the same time these latter two models allow Volkswagen to cover two other segments of the same market. In the same vein Egelman et al. (2013) shows that productivity improves when firms produce concurrently multiple generations of the same product in the same production unit, due to the transfer of knowledge between generations of products.

3 This is a real example. We indeed do not unveil the identity of the firm and omit, on purpose, some information for confidentiality reasons. A detailed description of the data-set used for the empirical investigation is provided in

2

products exported by this firm appears to a great extent fickle across markets: indeed it exports

14 different product-mixes in the 20 active destinations. However, together with this variability we also observe that there exist some combinations of products which a firm exports more frequently than the others which includes at the same time items with very high sales together with items with low sales value and whose composition depends by and large on technology and on markets characteristics. Indeed, when we look more in details at this firm we observe that, in 4 out of its top 10 destinations

4

(DEU,FRA,GRC,NLD), it exports the same product mix composed by “AC

Motors” of two different powers combined with an additional generic good labeled “Parts of these motors”. In other 3 of the top 10 destinations (AUS, USA, CZE) sales are concentrated on a different product mix based on “Universal AC/DC motors”. Further, the relative importance of the 3 products exported in the EU top destinations, while stable in a first approximation, change across markets: this firm is exporting to Germany mainly high power AC motors (those with power ranging between 750W and 75KW) while in Netherlands the most important products in term of export share are the low-power AC motors (those with power below 750W).

5

To what extent are these patterns, and in particular the coexistence of a a fickle part with a stable component in the mix of products a firm is selling, common among exporters? And what are the main factors driving the variation of a firm’s product mix choice across destination markets?

Using a cross section of firm-product-destination level Italian and French data, this paper provides an exhaustive investigation of export patterns of multi-product firms across destination markets.

In performing our investigations we innovate with respect to the existing literature by moving the focus from single product to product-mixes, both as a simple ordered list of product names and also considering the corresponding market shares. Moreover we explicitly control for a firm’s choice of not exporting some of its available products, that is by taking into account product selection.

Our results show that there is a great deal of variability among product-mixes a firm’s exports in different destinations both in terms of the combination of products and in terms of their relative importance in terms of export value. Among the drivers behind this variability a firm-destination specific measure of market size plays a major role but also market structure and the ability to match demand, again measured with firm-destination specific proxies, appear able to capture part of the observed variability. At the same time, together with this fickle part, we highlight the existence of a stable component among the diverse product-mixes exported. We show that this core combination of products is relevant, both in terms of frequency with which is exported and in terms of export value. We also show that some items in this core combination of products would not have been identified using a criterion based on sales values. In line with the economic intuition, we provide evidence that the probability of exporting this core set of products increases with the size of the destination market and with the ability of matching demand but it is inversely related with the market concentration.

We interpret our results as suggestive of the existence of widespread forms of production and

Section 3.

4

The top 10 destinations cover 90% of the total exports of this firm.

5 Figure A1 in Appendix A shows the export sales distribution across products and destinations for this firm.

3

demand complementarities making some combinations of products within a firm more likely to be exported than others.

6

At the same time demand conditions, strategic environments, consumers tastes and other market specific characteristics generate significant variability across product-mixes exported to different destinations. These results emphasize the central role of both technology and demand in shaping firms product-mix selection and link with the recent evidence showing that changes in a firm’s product structure contributes to a significant extent to reallocate resources within firms toward their most efficient use thus fostering aggregate revenue-based productivity growth (Bernard et al., 2010; Goldberg et al., 2010).

The remainder of the paper is organized as follows. Section 2 provides an overview of the existing literature on multi-product firms.

Section 3 describes the data used in the empirical analysis and provides a preliminary empirical exercise showing the degree of export sales variability across destinations. Section 3 defines the concept of a firm’s product vectors. Section 4 investigates the extent of geographical heterogeneity characterizing a firm’s product vectors and discusses three major factors likely to generate such diversity. Section 5 focuses instead on the stable part. The last section concludes.

2 Related literature

This paper relates to research on multiple-product firms in the industrial organization and international trade literature.

In the industrial organization tradition there exists a vast literature exploring fostering factors and limiting forces operating behind diversification dynamics. Traditional motives originate in the economies of scope induced by excessive capacity in productive factors (Bayley and Friedlaender,

1982; Montgomery, 1994, provide two classic reviews). Demand complementarities and strategic bundling/tying of different products have also shown to be important diversification drivers. Stigler

(1963) and Whinston (1990) investigate products bundling/tying for price discrimination and market power leverage purposes, respectively.

7

More recently, the development of “product platform strategies” has suggested that supply and demand factors might operate simultaneously (see the overview in Baldwin and Woodard, 2009). Among factors limiting the scope for diversification it has been found that both the demand or resources cannibalization and the idea that moving away from its core competencies reduces a firm’s efficiency in production play an important role (see

Roberts and McEvily (2005) and Silverman (1999)) .

Beyond the investigation of why firms diversify, the present paper more closely links with the research suggesting that there are combinations of products more likely to be co-produced within

6

This result is well in tune with what Bernard et al. (2010) find on domestic production using US Manufacturing

Censuses data.

7

Typical examples of strategic products bundling/tying are block-booking of movies and the pooling of an OS with a browser and a media player. Product bundling may also be induced by simple efficiency considerations (e.g.

tobacco and filter for typical cigarettes brand or right and left shoes together with their laces). A typical example of demand complementarity is associated with compatibility issues and aimed at reducing the risk of mismatching: a tablet with its cover or the cylinder head and the cylinder block for the same auto engine (Yu and Wong, 2015).

4

firms than others due to demand, technology or other forms of interdependence across products

(Bayley and Friedlaender, 1982). Using data on US manufacturing firms, Bernard et al. (2010) observe that the probability that a firm produces a product conditional on production of another product is relatively high within goods that belong to the same sectors or related sectors. As suggested by the authors, a successful model explaining multi-products firms should incorporate some forms of interdependence across products, either driven by demand or costs factors.

Within the industrial dynamics literature, several new streams of research on multi-product firms emphasize the importance of intra-firm adjustments which are significantly different from adjustments that occurs between firms due to entry and exit (Bernard et al., 2010; Goldberg et al., 2010; Navarro, 2012). These recent studies document the frequency of product switching within firms and its importance for industrial evolution and output growth: the intra-firm resource reallocation can indeed be a significant source of productivity increase. Bernard et al. (2010) and

Goldberg et al. (2010) show for US and Indian firms respectively, that changes in firms’ product mix have made a considerable contribution to both individual and aggregate output growth. None of these papers, however, consider whether and how the intra-firm reallocation mechanisms can be altered by supply and demand interdependence across products.

Our work is most closely related to the nascent empirical literature that documents the relevance and the behaviour of multi-product firms in international trade. While the literature on multi-product firms in the theory of industrial organization and industrial dynamics literature is well established, developments within the trade literature are more recent since they have been stimulated by the increasing availability of transaction level data. This new stream of research has shown that an overwhelming share of international trade is conducted by large firms that export a broad variety of products to different destinations. In the US firms shipping more than five (HS10) products represent 30% of total exporters but account for 97% of all exports (Bernard et al., 2009), in Brasil 25% of exporters ship ten or more (HS6) products and account for 75% of total exports

(Arkolakis and Muendler, 2010).

8

A set of empirical regularities concerning multi-product exporters have been reported by Arkolakis and Muendler (2013, 2010) for Brasil, Denmark, Chile and Norway. The authors report three robust stylized facts concerning an exporter’s number of products shipped within each destination

( export scope ) and the corresponding average sales per product within each country ( export scale ).

First, few large wide-scope exporters and many narrow-scope firms coexist within each destination.

Second, the sales of wide-scope exporters are concentrated in few products and the same firms are able to tolerate lower sales for their lowest-selling products. Third, a systematically positive relationship is observed between average exporter scale (i.e the average sales per product within each country) and exporter scope.

9

The omnipresence and the importance of multi-product firms in international trade has opened

8

Similar figures are observed for Italy and France where 42% and 40% of exporters ship more than five (HS6) products and account for 96% and 95% of total export flows, respectively.

9 Further strengthening these evidences, the same stylized facts appear to characterize both Italian and French exporters. Appendix B reports further details on these regularities.

5

new avenues for theory and several approaches have been consider to model the production of multiple goods in international markets. While differing in the assumption regarding supply and demand characteristics, these recent models all predict that within firm adjustments in response to trade policy changes are relevant in explaining aggregate trade improvements. Some recent empirical works provide support for these theoretical predictions (Bernard et al., 2011; Soderbom and Weng, 2012; Qiu and Zhou, 2013; Iacovone and Javorcik, 2010; Mayer et al., 2014). In response to tariff reductions or increase competition, the evidence suggests that firms reduce the number of products they export and skew export sales towards their better performing products. Such liberalization episodes induce an increase in firm and aggregate productivity as a consequence of the reallocation of resources across products within firms.

While the existing models consider different features of multi-product exporters, their focus is mainly on the role of selection across products and countries within firms and on the effect of differences in competition across markets on the skewness of firm sales across products. Less attention has been paid on the modeling of firm’s product mix composition and their variability across countries. We contribute to this literature by exploring the variability of firm’s product mix choices across destinations. We uncover new stylized facts regarding this variability and offer a novel explanation based on firms varying product mix composition across countries in response to market demand characteristics.

3 Data and definitions

Our analysis on multi-product and multi-country firms exploits trade data on the universe of Italian and French exporters. The foreign trade statistics are collected by the national statistical office and consist of all cross-border transactions performed by Italian and French firms, respectively.

10

For all export flows defined at the firm-product-destination level the data include both annual values and quantities expressed respectively in euros and in kilograms. Product categories are classified according to the Harmonized System and they are reported at the 6-digit level (HS6).

11

Since we are interested in the cross-section of firm-product exports across destinations, we restrict our attention to the most recent year available for both countries, namely 2006. Finally, since our study focuses on the variability of a firm’s exports across products and countries we exclude from the analysis those firms exporting only one product or serving only one destination.

Table 1 compares the total value of exports, the number of firms and the average number of products and destinations of the whole and of the restricted sample for both Italy and France in

2006.

12

It is important to note that while the reduction in the number of firms is sizable in both

10

The datasets were accessed at the ISTAT and Banque de France facilities and they have been made available for work after careful screening to avoid disclosure of individual information.

11

This is the finest level of disaggregation available for Italy while French custom data are available at 8-digit

(CN8). However, we consider the classification at 6-digit to make the analysis comparable across the two countries.

12

Table C1 in the Appendix C reports the total value of exports and the number of exporters distinguishing between three broad categories of firms: manufacturers, wholesalers and retailers, others. In Italy there is a larger fraction of manufacturing exporters than in France (55% vs 32%). These firms account for a large share of a country’s total

6

Total exports

(billion euros)

# Firms

Avg. # Products

Avg. # Countries

Table 1: DESCRIPTIVE STATISTICS

Italy France

Whole sample Restricted sample Whole sample Restricted sample

(1) (2) (3) (4)

271.1

266.2

268.7

265.1

74,365

8.4

9.5

45,530

12.6

14.7

32,432

8.5

8.8

19,689

12.9

13.5

Notes : Table reports descriptive statistics on the Italian and French dataset for 2006. In the restricted sample we keep those firms exporting more than one product and serving more than one destination.

countries, the amount of exports covered remains substantially unchanged.

13

Before proceeding in the empirical analysis, we conduct a preliminary exercise showing that there exist sources of variability of export sales both at firm-destination and firm-product-destination level. We regress the export value of each firm-product-destination transaction on different sets of fixed effects. Specifically we estimate the following regression model y f pd

= α f p

+ α pd

+ α f d

+ f pd

, (1) where y f pd are firm-product-destination export sales, α f p is a firm-product fixed effect that captures all the variety-specific factors, such as cost or quality, α pd is a product-country fixed effect aiming to capture factors affecting all firms exporting the same HS6 product to the same destination, such as competition and demand level. Finally, α f d is a firm-country fixed effect and f pd is an idiosyncratic firm-product-destination component together capturing asymmetric preferences between varieties and taste heterogeneity across countries. To assess the export sales variability we need to restrict our analysis to those products exported by each firm to more than one country, those countryproduct combinations served by more than one firm and those pairs firm-destination for which we have more than one product.

Results are reported in Table 2. Two comments are in order. First, in line with previous studies firm-product and product-destination heterogeneity appear to play a major role in explaining the variation in the data.

14

This justifies theoretical approaches combining efficiency varying by firmproduct (rather than by firm only) together with product-destination specific entry costs. Second, a combination of firm-product and country-product FE leaves almost 40% of the export sales variability unexplained pointing out at the existence of two other relevant sources of heterogeneity, exports (85% in Italy, 71% in France). On the contrary, France is characterized by a larger number of wholesaler and retailer exporters than Italy (43% in France against 36% in Italy.). Wholesalers and retailers account for 21% of

France’s total exports but only 12% in Italy.

13

Because of some missing value in the employment variable, in the analyses that follow we will be working with a slightly smaller number of French firms (19,043 rather than 19,689).

14 Di Comite et al. (2014), Munch and X. (2008) and Bernard et al. (2011) reach similar conclusions.

7

Table 2: R

2

FOR REGRESSIONS ON VARIETY-COUNTRY (LOG) EX-

PORT SALES.

HS 6-digit CN 8-digit firm-product FE product-destination FE

Yes

Yes

Yes

Yes

Yes

Yes

Yes

Yes

ITALY

FRANCE

52.3%

55.8%

25.1%

24.2%

60.0%

63.7% 56.0% 25.4% 63.8%

Notes : Results are based on restricted sample imposing a minimum of two destinations for each firm-product, of two firms for each country-product and of two products for each firm-destination. Italian and French custom data for

2006.

namely firm-destination and firm-product-destination (also referred as variety-destination).

15

.

In order to check that our results are not merely driven by a classification effect, we replicated the analysis for French firms by narrowing the definition of a variety and using the firm-CN8 combination. As shown in Table 2, independent of the product-market definition, we see that a large amount of the variability is left unexplained when we include both firm-product and countryproduct fixed effects.

In what follows, we provide a characterization of multi-country and multi-product firms export patterns. It is important to stress that we do not consider separately the firm-destination and firm-product-destination sources of variability. Rather, we develop an empirical strategy, based on firms product mix heterogeneity across destinations, that captures to a large extent both sources of fickleness. We assess the existence of such variability and the factors likely to explain this heterogeneity.

Product vectors

Differently from previous empirical analyses that look at each single good exported by a firm, the focus of this paper is on the mix of products that a firm sells in the different destinations where it is active. With this purpose we define the Local Product Vector (LPV f d

) and the Global Product

Vector (GPV f

). The former is the set of products sold by firm f to destination d while the latter contains the whole set of products exported by firm f irrespectively from their destination. In the rest of this paper we study LPVs and GPVs from two different but complementary perspectives.

First, introducing a novelty with respect to the existing literature, we look at product vectors as an ordered list of product names, in our case HS6 product codes. Formally, we represent the

GPV f as an ordered 16 vector of 1s whose size is equal to the total number of products firm f

15 In unreported regressions we include, together with firm-product and product-destination FE, firm-destination

FE. The latter explains an additional 12% of the observed variability summing up to 72% for Italy and 75% for

France, leaving about 25% of the variability due to firm-product-destination heterogeneity

16

We follow the order induced by the HS classification system.

8

0.10

0.02

0.01

0.01

0.00

0.02

0.50

0.02

0.12

0.02

0.28

0.79

0.18

0.78

0.18

0.94

0.06

0.93

0.07

0.31

0.17

0.45

0.53

0.37

0.02

0.76

0.21

0.09

0.21

0.13

0.23

0.33

1.00

0.16

1.00

1.00 1.00

DEU

0.03

ESP FRA

0.83

0.08

AUS GRC GBR USA CZE NLD

0.11

0.11

0.41

0.82

0.72

ISR

0.75

0.13

1.00

0.41

0.59

0.93

0.07

D11 D12 D13 D14 D15 D16 D17 D18 D19 D20

Destination

0.11

0.02

0.02

0.02

0.20

0.01

0.01

0.00

0.01

0.01

0.00

GPV

0.01

0.01

0.04

0.01

0.52

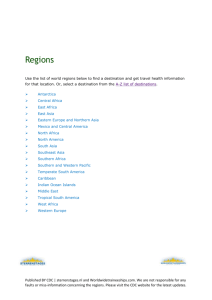

Figure 1: Global product vector (GPV) and Local product Vectors (LPV) with product market shares for a firm in the Italian sample. 0 .

00 represents products whose market share is lower than

1%.

exports (NP f

). Similarly, we characterize the LPV f d as an ordered binary vector reporting 1 when a product is actually exported by firm f to destination d and 0 otherwise. The LPV f d represents one of the 2NP f possible arrangements of NP f different products. Clearly, as a consequence all the local product vectors LPV f d belonging to a given firm have exactly the same dimension of the corresponding GPV f

. This way to proceed introduces a further novelty with respect to the existing studies in that it allows us to control for a firm’s choice of not exporting an available product to a given destination, that is by taking into account product selection. Indeed, the fact that a firm decides not to export one of its products to a given destination is an economic choice likely to contain relevant information.

Second, we enrich the information contained in LPVs and GPVs adding information on product market shares. Formally we replace in the GPV f corresponding product and 1s in the LPV f d

1s with firm f ’s worldwide market shares of the with firm f ’s market shares of the corresponding product exported to destination d . By construction the GPV and LPV with market shares still have the same dimension and in this case their components sum up to 1. Figure 1 reports the

GPV f and LPV f d for the firm we used as an illustrative example in the Introduction. This figure provides illustrative evidence on the richness of a firm’s product mix structure. This firm tends to export different combinations of product in different destinations but, at the same time, some

9

Table 3: EXPORT DIVERSIFICATION: PRODUCTS, DESTINATIONS and LPV

Mean Std. Dev.

Min.

1Q 2Q 3Q Max.

Obs.

ITALY

# Products

# Destinations

# LPV

12.55

14.66

8.46

# Products in LPV 2.43

19.18

15.53

9.80

2.37

2.00

3.00

7.00

14.00

555.00

45,456

2.00

4.00

9.00

21.00

129.00

45,456

1.00

1.00

3.00

1.33

5.00

1.80

10.00

2.62

117.00

65.31

45,456

45,456

FRANCE

# Products

# Destinations

12.92

13.50

# LPV 7.98

# Products in LPV 2.59

22.08

15.52

9.90

3.00

2.00

2.00

1.00

1.00

3.00

3.00

2.00

1.33

6.00

8.00

4.00

1.80

14.00

18.00

9.00

2.72

649.00

165.00

141.00

75.73

19,608

19,608

19,608

19,608

Notes : Table reports the descriptive statistics for firms’ export diversification for 2006. The statistics are computed on the restricted sample, i.e. we remove from the dataset exporters with either a single product or a single destination.

combinations appear more common than others.

Within each destination, the distribution of product sales appears very skewed. However, the relative importance of each product within each destination changes across markets. Last, the most typical choice this firm makes is that of not exporting an available product in an active destination, suggesting once again the importance of controlling for product selection when studying a firm’s diversification patterns in international markets.

Broadening the perspective, Table 3 reports descriptive statistics on product vectors for Italian

(top panel) and French (bottom panel) exporters. The first two rows of each panel provide information on the distribution of the number of products exported and of the number of destinations served by each firm. On average, an Italian exporter exports 12 products and it reaches more than 14 destinations while a French exporters exports 12 products and it serves 13 destinations.

17

Note the remarkable similarity between the Italian and French “average” exporters both in terms of their product and geographical diversification. Next, the third and the fourth row of each panel of Table 3 report, respectively, descriptive statistics on the distribution of the number of LPVs and of the number of products exported to a given destination (i.e. the number of 1s in a LPV).

For both Italy and France, the average number of LPVs is 8 with, again on average, 2.5 products actually exported.

18

These two simple figures, beyond confirming again an impressive similarity between the two countries, suggest that the average exporter does not sell the same product mix to each destination. At the same time, it exports to each destination only a small subset of its set of products.

In the next section we investigate the extent of geographical heterogeneity characterizing a

17 If we consider the whole population of exporters on average the number of products exported by both Italian and French firms is 8, while the number of destinations reached is 9.5 for Italy and 8.8 for France, respectively.

18

Note that a firm’s maximum number of product vectors is the minimum between 2

N P f − 1 and ND f

, where NP f is the number of products exported and ND f the number of destinations served by firm f .

10

firm’s LPVs and we discuss few major factors likely to generate such diversity.

4 Product vectors: the fickle fringe

In order to provide a quantitative assessment of the degree of diversity of a firm’s LPVs we measure, with a proper metric, the distance between each LPV, first considered as a list of 0s and 1s, and the corresponding GPV. The specific aim of this exercise is to capture how common is for a firm to decide not to export an available product to the whole set of destination it serves. Then, we change perspective and we add to firms’ GPV and LPVs the corresponding product market shares computing, again with a proper metric, the distance of each LPV from its GPV. This second exercise is directly linked to the testing of the hypothesis of a perfectly rigid hierarchy of products in different destinations implied by the most popular theoretical models describing multi-product and multi-destination firms. Finally, we set up a regression framework to investigate the relative importance of three potential drivers behind the observed geographical diversification patterns of

Italian and French exporters.

Measuring diversity among product vectors

To capture the variability of a firm’s local product vectors, as lists of 0s and 1s, across destinations we measure the distance of LPV f d from the corresponding GPV f using a normalized version of the

Levenshtein distance (LevD), also known as Edit distance. It is a string metric developed to measure the difference between two sequences. Formally, it represents the minimum number of single edits

(insertion, deletion, substitution) required to change one sequence into the other divided by the number of elements of the longest sequence minus 1.

19

Consider the following simple example

1

GPV f

=

1

1

1

1

LPV f d

1

=

0

1

1

1

LPV f d

2

=

1

0

0

.

Both LPV f d

1 and LPV f d

2 are different from the GPV f but how much different are they? In this example the LevD(GPV f

,LPV f d

1

) is equal to 1/3: 1 change is needed to transform LPV f d

1 into the GPV f and the length of the longest sequence is 4. Instead, the LevD(GPV equal to 2/3: 2 changes are required to transform LPV f d

2 into the GPV f f

,LPV f d

2

) is and the length of the longest sequence is still 4. More generally, in our example any additional difference between the two sequence affects the Levenshtein distance by 1/3.

Figure 2 reports frequency distribution of the LevD between each LPV f d and the corresponding

GPV f for Italian and French exporters. The observed values for the LevD span the whole theoretical range of the Levenshtein distance, that is [0 , 1). Still, it is apparent that the vast majority of the

19 See Appendix D for more details on this measure. Note that in our case we need to consider only substitutions since all the product vectors have the same dimension. In this case this metric is also known as Hamming distance.

11

1

0.1

LEVENSHTEIN DISTANCE from GPV - 2006

Italy

France

Mean Median Obs.

0.894 0.986 666522

0.888 0.988 264615

ITALY

FRANCE

0.01

0.001

[0-0.1) [0.1-0.2) [0.2-0.3) [0.3-0.4) [0.4-0.5) [0.5-0.6) [0.6-0.7) [0.7-0.8) [0.8-0.9)

Levenshtein distance

[0.9-1]

Figure 2: Frequency histograms of the Leveshtein distance from GPV in 2006 for Italy (red) and

France (blue).

observations are concentrated in the right tail of the two distributions with an average not far from

0.9 and an even higher value of the median. Given that the average number of products by both

Italian and French exporters is about 13, an average LevD means that one needs to make about 11 changes to transform a local into the corresponding global product vector. This result corroborates the idea that exporters in both countries tend to possess a rather diversified portfolio of products but they decide to export in each destination only a small and diverse subset of them.

To eliminate the possibility that the picture we observe is driven by some peculiar properties of our sample we run a few robustness checks. First, we investigate if firm size matters. We build quartiles of the firm size distribution in terms of number of employees and we study the LevD for the first and fourth quartile. Second, we condition our analysis on highly diversified firms versus low diversified firms defined as those exporting more than 15 products versus those exporting less than 6. Third, as a further important stress test for our result we calculate the LevD using only a firm’s most important destination in term of export value. Last, we replicate the exercise using data from 2003. Appendix E, which reports frequency distribution of the observed LevD for these robustness checks, largely confirms our result.

Working with product vectors as simple lists of HS6 codes has the main advantage of allowing us to identify the effects of different forms of product complementarity (demand or supply driven) able to generate combinations of products containing, as equally important, high values items with

12

low value ones.

20

However, it is clear that not all the products a firm exports in a destination play the same strategic role for its competitiveness. Apple Inc. will be more affected by a negative demand shock, for example in China, on its Iphone rather than by a similar shock on its Apple pencil for

Ipad. This is an important concern since we already know that a firm’s distribution of export sales across products within a destination tend to be highly skewed concentrating sales in very few items.

Indeed, existing studies on multi-product exporters have so far almost exclusively focused product mixes defined using product market shares. In particular, they found that the rank correlation, computed either across destinations or between the local and the global rankings, ranges between

0.50 and 0.85 (Mayer et al., 2014; Arkolakis and Muendler, 2010; Di Comite et al., 2014).

While it is certainly important to weight products by their market shares, we believe that the exiting approach based on rank correlation suffers of two main limitations. First, rank correlation does not allow to control for a firm’s decision of not exporting a product to a given destination and this may upward bias the observed correlation. Second, rank correlation fails in properly quantifying the compositional dissimilarity between two different vectors being based on rankings.

In the following we consider both issues.

First, we compute the Spearman rank correlation, directly controlling for a firm’s decision of not exporting a product to a given destination. Results appear substantially lower than those in the existing literature: the mean and the median rank correlation decrease to 0.410 and 0.420 for both Italy and France.

21 Indeed, once controlling for the extensive margin response, we observe a substantial departures from a perfectly stable hierarchy of products across destinations.

22

Second we replace Spearman rank correlation with a proper distance measure to capture the effective dissimilarity among product vectors measured in terms of market shares. Indeed, rank correlation cannot capture any heterogeneity across PVs in a situation like the following

0 .

97

GPV f

=

0 .

02

0 .

01

0 .

51

LPV f d

1

=

0 .

49

0

0 .

85

LPV f d

2

=

0 .

15

0 where, notwithstanding LPV f d

1 and LPV f d

2 present two substantially different structures, the rank correlation between each LPV and the GPV is in both cases equal to one. To overcome this limitation we use the Bray-Curtis dissimilarity measure, a statistic that allows us to quantify the

20 From the example proposed in the Introduction is evident that, within a firm, there are products that are exported more frequently than others, not necessarily characterized by high export sales.

21 Without considering the 0s, i.e. the choice of not exporting an available product to an active destination, the mean and the median Spearman pairwise rank correlation for Italy, using data for 2006, are 0.581 and 0.90, respectively.

Similar figures are observed for France.

22

The strong reduction in the rank correlation holds even when we restrict our analysis on the set of most relevant markets served by a firm that are those representing more than 1% of a firm’s total exports. Figures for this robustness check are available upon request.

13

0.3

0.2

0.15

0.1

0.08

0.06

BRAY-CURTIS dissimilarity from GPV 2006

Italy

France

Mean Median Obs.

0.461 0.409 666522

0.460 0.415 264615

ITALY

FRANCE

[0-0.1) [0.1-0.2) [0.2-0.3) [0.3-0.4) [0.4-0.5) [0.5-0.6) [0.6-0.7) [0.7-0.8) [0.8-0.9) [0.9-1]

Bray-Curtis dissimilarity

Figure 3: Frequency histograms of the Bray-Curtis distance from products market shares of the

GPV in 2006 for Italy (red) and France (blue).

compositional diversity between two vectors. This dissimilarity index is defined as

BC f d

=

P p

| s f p

− s f dp

|

P p

| s f p

+ s f dp

|

, (2) where s f p and s f dp represent export shares of product vector d of firm f , respectively.

23 P p

| s f p

+ s f dp

| p in the global vector and in the destination is a normalizing factor, always equal to 2 in our case. The Bray-Curtis dissimilarity is bound between 0 and 1, where 0 means the two vectors have the same composition ( s f p

= s f dp for all p ) and 1 means the two vectors are completely disjoint. In the example above the BC dissimilarity computed for LPV f d

1 is 0.47 and that for LPV f d

2 is 0.13.

In Figure 3 we report the Bray-Curtis dissimilarity computed between each firm LPV and the corresponding GPV. First, it is interesting to note that as expected focusing on product level export shares reduces the overall degree of heterogeneity among a firm’s LPVs with respect to its GPV.

However, only one fifth of the observations display a value of the BC distance lower than 0.1 and this appears robust across Italy and France. With an average BC distance of around 0.46 these results provide further support against the idea that there exists a highly stable hierarchy among the products a firm exports in different destinations.

As before, we test the robustness of this investigation disaggregating our sample by firms’ size, by the overall number of product exported, focusing only on the top destination, and using data

23 See Appendix D for more details on this measure.

14

from 2003. Results, reported in Appendix E, overall confirm the ability of the BC distance to capture heterogeneity across PV and the robustness of our result.

Regression analysis

The analysis so far reveals a substantial degree of geographical diversity among product vectors exported by Italian and French firms and an associated departure from a perfect ordering of the products sold in different destinations. At the same time, the pattern observed is at odds with a scenario where products are randomly assigned across countries. In this section, we set up a regression framework to identify the role of different factors in driving a firm’s choice of the specific product mix to be exported in a destination market.

Our point of departure is that theoretical models of multi-product and multi-country firms based on cost efficiency as the only determinant of firm behavior in export markets cannot account for all the geographical variation in product mixes we detect in the data. Indeed, although firm-product heterogeneity in costs has been empirically confirmed to be very important in determining firms’ behavior into export markets, it seems to be not a sufficient condition to explain the firm-product level sales variation in different countries. Our results, instead, corroborates models predicting imperfect correlation between a firm’s product export sales across countries, as in Bernard et al.

(2011). Motivated by this literature, in the following we focus specifically on 3 potential explanatory factors.

First, we consider Market size . Demand heterogeneity, driven by asymmetric preferences between varieties across countries, is likely to play a role in explaining why a firm’s product market share and its ranking vary among destinations. In this respect, the model in Di Comite et al. (2014) show that single-product firms’ sales vary across markets when each destination is allowed to have different preferences for the same variety supplied.

Second, we focus on Market structure with the underlying idea that the level of competition faced by a firm in a destination market is likely to influence the choice of the products exported to that market. In Mayer et al. (2014), for example, a firm responds to tougher competition by dropping its worst performing products and by concentrating its export sales towards the best performing ones. In their model, however, the variation in competition cannot alter the rigid ordering of a firm’s product ranking but only the product mix skewness across destinations.

A third explanation for the variation in a firm-product export sales, not explicitly considered in any theoretical model, is provided by the difference across countries in the market positioning of a firm with respect to its competitors. A firm’s choice regarding its exports across countries can be related to how different is the price of the product exported to a specific country with respect to the average price of its competitors in that product-destination. This price difference can be driven by several factors such as quality differences, markups heterogeneity, market competition, firm composition, supply factors such as shipping costs, and further destination country characteristics.

Regardless the sources of within-firm price adjustments, price differences of a firm with respect to its competitors can explain the variation in a firm-product export sales across countries. We refer

15

to this idea as Market positioning .

To build empirical counterparts for Market size, Market structure and Market positioning, we make use of trade data from BACI, a product level dataset recording imports and exports flows for a very large set of countries (cfr. for details Gaulier and Zignago, 2010).

We start by calculating a proxy of market size. Using data from BACI we compute IM P

∗ pd

=

P IM P

∗ pod

, the total imports for product p to destination d .

O pd o ∈ O pd product p to destination d , excluding in turn Italy or France.

24 is the set of countries exporting

Then, for each firm-destination pair, we compute the simple average

25 of (log) IM P

∗ pd according to

Market size f d

=

1

X

| Π f

| p ∈ Π f log IM P

∗ pd where | Π f

| is the cardinality of the set products exported by firm f . A high value for Market size f d means that in the destination d there is a large potential demand for the combination of products exported by firm f .

Next, we build a proxy for Market structure.

Again using BACI we compute HHI

∗ pd

P o ∈ O pd

( Imp

∗ pdo

/ P o ∈ O pd

Imp

∗ pdo

)

2

=

, the Herfindal index for product p in destination d . We take the average over products for each firm-destination pair

Market structure f d

=

1

X

| Π f

| p ∈ Π f log HHI

∗ pd

.

The higher the value of Market structure f d

, the greater the level of concentration faced by firm f in the foreign market d .

Finally, we compute an empirical measure of Market positioning following a two step procedure.

!

Using the BACI dataset, we first compute U V

∗ pd

= exp P o ∈ O pd

IM P

IM P

∗ pod

∗ pd log U V

∗ pod

, that is the weighted

26 geometric average of the unit values of product p in destination d . Second we build

− log | U V f pd

− U V

∗ pd

| the opposite of the absolute value of the difference between the unit value for product p charged by firm f in destination d with respect to the average in that market. Last, we take as above a simple average across products exported by firm f in destination d using

Market positioning f d

=

1

X

| Π f d

| p ∈ Π f d

− log | U V f pd

− U V

∗ pd

| .

The higher the value of this index the closer is the market positioning, in terms of unit values, of

24

All the proxies built using BACI are identified with an ∗ as superscript.

25 By taking a weighted average, using as weight the relative importance of product p in a firm’s total export sales, would introduce an endogeneity problem as product market shares are also used when building one of our dependent variable, i.e. the Bray-Curtis measure.

26 Weights captures the relative importance of that transaction on the total imports for the product-destination pair pd .

16

Table 4: REGRESSIONS ON THE LEVENSHTEIN AND BRAY-CURTIS DISTANCE

FROM GPV, 2006

(1a)

ITALY

(1b) a (2a)

FRANCE

(2b) a

Dependent variable: Lev f d

Market size f d

Market structure

Adj.

R 2 f d

Market positioning f d

-0.025

-0.266

-0.036

-0.411

(0.002) [0.000] (0.025) [0.000] (0.004) [0.000] (0.042) [0.000]

0.031

0.057

0.036

0.066

(0.007) [0.000] (0.014) [0.000] (0.008) [0.000] (0.016) [0.000]

-0.002

-0.023

-0.001

-0.012

(0.0004) [0.000] (0.004) [0.000] (0.0005) [0.050] (0.006) [0.050]

0.54

0.55

Dependent variable: BC f d

Market size f d

Market structure

Adj.

R 2 f d

Market positioning f d

-0.031

-0.173

-0.034

-0.221

(0.002) [0.000] (0.013) [0.000] (0.002) [0.000] (0.015) [0.000]

0.047

0.046

0.040

0.042

(0.005) [0.000] (0.005) [0.000] (0.006) [0.000] (0.007) [0.000]

-0.023

-0.145

-0.014

-0.094

(0.002) [0.000] (0.010) [0.000] (0.001) [0.000] (0.006) [0.000]

0.49

0.48

N.Obs

Firm FE and Country FE

664,419

Yes

229,450

Yes

Notes : Table reports regression on the Levenshtein and Bray-Curtis dissimilarity measures. Data are for

2006.

a

Columns (1b) and (2b) report standardized coefficients. Standard error clustered at firm and country level. Coefficients reported together with standard errors (brackets) and p-values (squared brackets).

a firm f to those of its competitors.

To investigate the role of these 3 factors as drivers of the observed heterogeneity across LPVs, we estimate the following regression model

Y f d

= β

1

Market size f d

+ β

2

Market structure f d

+ β

3

Market positioning f d

+ α f

+ α d

+ f d

, (3) where Y f d is either the Levenshtein distance (LevD f d

) or the Bray-Curtis dissimilarity index

(BC f d

). Since we seek to uncover the variation in the dissimilarity index for a given firm, we include in the model firm fixed effects throughout α f to account for systematic differences across exporters in ability that might affect trade outcome across destinations. We also include destination fixed effects, α d

, which implicitly account for cross-country differences in total income, market toughness, trade costs and other institutional frictions that might affect the variation in a firm’s local product vector. We are thus interested in β ’s which reflects the sign of the conditional correlation between the distance or the dissimilarity index and our firm-destination level variables.

17

Since on the right-hand side of our regression we have the logarithm of a geometric mean, the estimated coefficients can be interpreted as semi-elasticities. The error term, f d

, includes possible other firm-destination idiosyncratic factors explaining the heterogeneity detected. Standard errors are clustered at firm and country level.

Table 4 contains the results for both the dependent variables. In columns (1a) and (2a) we present the benchmark specification for Italy and France, respectively, while in columns (1b) and

(2b) we report beta coefficients, estimated using standardized variables. Since our dependent variables are measured over a scale that does not possess a clear quantitative economic interpretation and since we are interested in comparing the role of the different regressors, we focus on these latter results in our discussion. Once again, we interpret the sign of β ’s as the sign of a conditional correlation that does not reflect causality.

We start with the top panel reporting results for the model where the dependent variable is the

Levenshtein distance LevD f d

. First, all the three firm-country level variables have significant impact on the distance measure. Second, in line with the economic intuition, the dissimilarity between

LPVs and the corresponding GPV is lower in larger markets, in countries where the concentration is smaller and where a firm’s matching in terms of market positioning is better. Indeed, it is more likely for a firm to export all the products of its portfolio in those destinations where there is a large demand for its products, where competition is not impeded by just few large players and where the unit values charged are in line with average unit values prevailing in those markets. Third, Market size seems to have the strongest effect. If we increase the market size by one standard deviation, the Levenshtein distance will decrease by 0.266 and 0.411 standard deviations in Italy and France, respectively. This means that an increase by one standard deviation of Market size reduces by one the average number of changes required to transform a firm’s LPV into its GPV for the typical exporter in Italy and France. Changes in market structure and market positioning seem to have a more limited impact. Finally, once again we observe an impressive similarity between Italian and

French exporters hinting at the existence of common mechanisms behind this set of evidences (cfr.

below the section Discussion).

The bottom panel of Table 4 contains the results for the Brays-Curtis index. The analysis here considers not only the variability in the composition of the product vectors but also the relative importance in terms of export share of each product within the vector. The results are very much in line with that observed for the LevD distance measure. An increase in the market size decreases the dissimilarity between the export shares of the products belonging to a firm’s local vector and those of the global one. That is a firm, when serving a destination characterized by a higher demand for its products, is likely to serve this country with a product vector whose structure reflects that of its global one. The variable Market structure is instead positively correlated with the dissimilarity index. Where concentration is higher, a firm tends to export a local product vector with products market shares that tend to be more diverse of those in the GPV. Finally, to a destination where its product prices are in line with those of the competitors, a firm exports a product vector whose shares are similar to that of the global one. In terms of the relative importance of the 3 regressors

18

we observe again that market size is playing a major role even if in this case market positioning appears to be able to explain a larger part of the variability in the Bray-Curtis distance. This is especially true for Italy, whose firms seem to be more sensitive to their relative fit in terms of unit values in a destination market.

4.1

Robustness checks

In this section, we consider a set of exercises aimed at testing the robustness of our results with respect to a few possible confounding factors.

First, as suggested by a recent empirical literature on multi-product exporters a firm’s product mix exported in different markets may be influenced by differences in tariffs regulating trade across destinations. Bernard et al. (2011) show, for example, that a declining trade costs causes firms to drop their least attractive products while Dhingra (2013) proves, for Thailand, that exportoriented firms reduced their product lines in response to a unilateral tariff cut.

27 To try to isolate this effect of tariffs on firms’ product vectors choices across countries we add to our specification

(3) an additional regressor, Tariff f d

,

28 defined as

Tariff f d

=

1

X

| Π f

| p ∈ Π f

Tariff rate pd where Tariff rate pd is the level of tariff payed to export product p in destination d while | Π f

| is the cardinality of the set products exported by firm f . We expect that the higher the tariff level faced by firm f in destination d , the more difficult will be to export the whole set of product in its GPV and then the higher will be the dissimilarity among LPVs and the GPV.

Estimates for the beta coefficients on Tariff f d are reported in columns 1 and 2 of Table 5 for

Italy and Table 6 for French, respectively. The main message is that when we include the tariff variable our results do not change. A firm’s is likely to export a product vector close to its global vector in relatively larger markets and where its position in terms of its export prices is more in line with that of its competitors. On the contrary, higher concentration is associated with higher distance. The variable Tariff f d turns out to be not statistically significant in the regressions for

Italy and barely significant for France when using the Levenshtein regression as dependent variable.

This lack of statistical power for Tariff f d might cast some doubts on the validity of this robustness check so we also estimate our regression considering only those products exported to countries belonging to the EU where no tariffs are in place. As expected all the coefficients are smaller than in the case of the whole sample but the overall story is not affected.

Second, to provide evidence that our empirical results are not capturing product mix heterogeneity related to the level of income in destination countries we re-compute the distance measures

27

From a theoretical point of view, Qiu and Zhou (2013) build a model where efficient firms expand their export product scope in response to foreign tariff cuts, whereas inefficient firms reduce theirs.

28

The variable Tariff is taken from XXX

19

Table 5: REGRESSIONS ON THE LEVENSHTEIN AND BRAY-CURTIS DISTANCE FROM GPV: ROBUST-

NESS CHECKS FOR ITALY

Tariff

(1)

EU countries

(2)

ITALY

Developed

(3)

No carry along

(4)

No MNC

(5)

Dependent variable: Lev f d

Market size f d

Market structure

Adj.

R

2 f d

Market positioning

Tariff f d f d

-0.267

-0.126

-0.237

-0.245

-0.260

(0.026) [0.000] (0.020) [0.000] (0.025) [0.000] (0.022) [0.000] (0.025) [0.000]

0.055

0.027

0.053

0.055

0.055

(0.014) [0.000] (0.009) [0.000] (0.014) [0.000] (0.013) [0.000] (0.014) [0.000]

-0.023

-0.022

-0.021

-0.019

-0.024

(0.005) [0.000] (0.005) [0.000] (0.005) [0.000] (0.004) [0.000] (0.004) [0.000]

0.005

(0.005) [0.397]

0.25

0.66

0.58

0.56

0.54

Dependent variable: BC f d

Market size f d

Market structure

Tariff f d f d

Market positioning

Adj.

R

2 f d

-0.174

-0.107

-0.153

-0.129

-0.169

(0.013) [0.001] (0.034) [0.001] (0.023) [0.000] (0.012) [0.000] (0.013) [0.000]

0.045

0.016

0.045

0.042

0.045

(0.005) [0.000] (0.006) [0.006] (0.007) [0.000] (0.006) [0.000] (0.005) [0.000]

-0.144

-0.055

-0.120

-0.138

-0.141

(0.010) [0.000] (0.008) [0.000] (0.013) [0.000] (0.010) [0.000] (0.010) [0.000]

-0.002

(0.004) [0.512]

0.49

0.56

0.51

0.45

0.49

N.Obs

Firm FE

Country FE

654,580

Yes

Yes

282,862

Yes

Yes

456,259

Yes

Yes

652,872

Yes

Yes

618,464

Yes

Yes

Notes : Table reports regression on the Levenshtein and Bray-Curtis dissimilarity measures. Data are for 2006. Standard error clustered at firm and country level. Standardized coefficients reported together with standard errors (brackets) and p-values (squared brackets).

Table 6: REGRESSIONS ON THE LEVENSHTEIN AND BRAY-CURTIS DISTANCE FROM

GPV: ROBUSTNESS CHECKS FOR FRANCE

Tariff

(1)

FRANCE

EU countries Developed

(2) (3)

No carry along

(4)

Dependent variable: Lev f d

Market size f d

Market structure

Adj.

R

2 f d

Market positioning

Tariff f d f d

-0.421

-0.173

-0.341

-0.364

(0.042) [0.000] (0.018) [0.000] (0.031) [0.000] (0.034) [0.000]

0.069

0.032

0.057

0.065

(0.016) [0.000] (0.006) [0.000] (0.017) [0.000] (0.015) [0.000]

-0.013

-0.037

-0.006

-0.009

(0.006) [0.048] (0.005) [0.000] (0.007) [0.380] (0.005) [0.110]

0.010

(0.004) [0.034]

0.31

0.60

0.44

0.34

Dependent variable: BC f d

Market size f d

Market structure f d

Market positioning

Tariff f d

Adj.

R

2 f d

-0.226

-0.139

-0.194

-0.132

(0.015) [0.000] (0.017) [0.000] (0.017) [0.000] (0.016) [0.000]

0.043

0.021

0.046

0.040

(0.007) [0.000] (0.004) [0.000] (0.007) [0.000] (0.007) [0.000]

-0.092

-0.056

-0.085

-0.092

(0.006) [0.000] (0.007) [0.000] (0.008) [0.000] (0.006) [0.000]

-0.003

(0.002) [0.272]

0.48

0.56

0.49

0.42

N.Obs

Firm FE

Country FE

222,907

Yes

Yes

101,432

Yes

Yes

156,813

Yes

Yes

217,502

Yes

Yes

Notes : Table reports regression on the Levenshtein and Bray-Curtis dissimilarity measures. Data are for 2006.

Standard error clustered at firm and country level. Standardized coefficients reported together with standard errors

(brackets) and p-values (squared brackets).

20

and re-run the regressions focusing only on a set of developed countries.

29

Indeed, several empirical analyses shows that firms are more likely to export high quality products and technologically advance goods to high-income countries (Verhoogen, 2008; Crino’ and Epifani, 2012; Flach and

Janeba, 2013). More generally, firms segment markets and adapt product quality and prices according to the income level of the destination country. Results, reported in columns 3 of both tables, provide evidence that our findings are not neutralized when focusing on developed countries only. The three firm-country level variables are still effective in capturing the variability of products vectors across destinations.

Third, in columns 4 we report the results concerning a fourth sensitivity check aimed at ensuring that our findings are not driven by the “carry-along trade” effect according to which manufacturing firms export products that they do not produce (Bernard et al., 2012). In principle, to detect the carry-along firms one should have information on both production and export data at the product level. Given that these data are not available, we approximate the phenomena by excluding from the sample those products which are contemporaneously exported and imported by the same firm.

We see that the findings are robust to this change in the composition of products vectors, excluding the possibility that our results are due to the imports of products which are re-exported by the firm and (possibly) not produced.

Finally, in order to account for the peculiar behavior of multinational companies (MNCs), which are complex organizations that sprawl across industries and countries, we remove them from the sample. Because data on multinationals are available only for Italy we provide this robustness check only in column 5 of Table 5.

30

This specification confirms the robustness of our baseline results regarding the relevance of all the three firm-country specific variables in explaining a firm’s distance between the local and the global product vector.

Additional robustness checks are reported in Table E1 for Italy and in Table E2 for France in the Appendix E. We consider whether our results change if we modify the way we define the three firm-destination level regressors. In the previous specifications, we build the three variables by averaging over the total number of products exported by a firm in a destination. This has the advantage of avoiding serious endogeneity problems that would arise by taking a weighted average but, at the same time, it does not take into account the relative importance of each product in a destination. To account for that we first compute the three measures using, for each firm, only the top product in each destination. Second, we use weighted variables using as weights the total exports of all Italian firms in product p to destination d over the total exports of all Italian firms in destination d , excluding the export sales of the firm under investigation. We also check that our findings are not a statistical artifact generated by the structure of product classification by considering those firms exporting in more than one HS2-digit product.

31

. Finally, we replicate the

29

We define developed countries those with capita income levels above the 50th percentile according to the World

Bank.

30

Among the papers analyzing the behavior of multiproduct multinationals see the recent work of Yeaple (2013).

31 The latter firms represent, both in Italy and France, around 80% of the population suggesting a remarkable degree of diversification among firms.

21

DEU ESP FRA AUS GRC GBR USA CZE NLD ISR D11 D12

Destination

D13 D14 D15 D16 D17 D18 D19 D20 GPV DEU ESP FRA AUS GRC GBR USA CZE NLD ISR D11 D12

Destination

D13 D14 D15 D16 D17 D18 D19 D20 GPV

Figure 4: Core Product Vector (CPV) and Weak Core Product Vectors (WCPV) for a firm in the

Italian sample.

analysis using the year 2003 and using wholesalers instead of manufacturing firms. Our results are robust to these other specifications.

5 Product vectors: the stable core

The analysis on product vectors revels a substantial degree of heterogeneity in a firms’ product mix across destinations, both from a qualitative and a quantitative perspective. At the same time, however, we do not observe a complete differentiation of LPVs suggesting that there might be a structural component in the mix of products a firm is exporting that is stable across destinations. So far the literature on multi-product firms has focused on the concept of core products defined as the top-selling varieties for which a firm seems to have some systematic advantage. Beyond considering single goods rather than vectors of products, the existing studies have concentrated exclusively on the importance of a product in terms of export share. However, in discussing the illustrative example in the introduction, we have shown that there are some combinations of products that are more likely than others to be exported. Further, we have shown that there might be goods that, although less relevant from a purely quantitative point of view, are crucial for the definition of a firm’s typical product mix. Because of product complementarity or technological relatedness, one might observe that the production and thus the export of one product may result in the production and the export of its components or of other related goods that are not necessarily characterized by high sales.

To provide a statistical characterization of this stable part of the product vectors, we introduce two new concepts: the Core Product Vector (CPV f

) and the Weak Core Product Vector (WCPV f

).

The former is the most frequent arrangement observed for a firm f across markets. Precisely, the

CPV f represents the typical (the modal) product vector exported by firm f .

32

The latter is any arrangements which leaves unchanged all the cells with 1 in the CPV f

. In other words, the WCPV f

32 Regarding the identification of the CPV f

, in case of ties LPV f are ranked according to the total value exported to destination d .

are ranked by their value. In other words they

22

Table 7: DESCRIPTIVE STATISTICS ON WCPV

Mean Std. Dev.

Min.

1Q 2Q 3Q Max.

Obs.

ITALY - Whole sample

Number of Products in WCPV

Share of destinations with WCPV

8.36

0.62

Share of export covered by products in WCPV 0.80

14.98

0.26

0.31

1.00

0.01

0.00

2.00

0.44

0.70

4.00

0.60

0.97

9.00

0.85

1.00

385.00

1.00

1.00

45,456

45,456

45,456

FRANCE - Whole sample

Number of Products in WCPV

Share of destinations with WCPV

8.78

0.62

Share of export covered by products in WCPV 0.79

18.64

0.26

0.31

1.00

0.02

0.00

2.00

0.46

0.67

3.00

0.62

0.97

8.00

0.85

1.00

586.00

1.00

1.00

19,608

19,608

19,608

Notes : The table reports the descriptive statistics for firms’ WCPV for 2006. The statistics are computed on the restricted sample, i.e.

we remove from the dataset exporters with either a single product or a single destination.

is a product vector containing the CPV f

. Figure 5 reports the CPV f and the WCPV f for the firm we are using as an illustrative example in this paper. For this firm the most frequent combination of products exported is composed by three goods. Two of them are specific types of electric motors and account for 52% and 11% of the total exports of this firm. The third one is labeled “parts of motors” and its market share is only 1%. This combination of products is served in 5 out of 20 destinations. We also observe that in other 2 countries the firm sells the very same product mix together with an additional idiosyncratic product. Therefore 7 out of 20 destinations are served with the WCPV. It is interesting to note that 6 among these 7 are in the Top 10 destinations in terms of market shares while the remaining one account for only 1%.

Table 7 reports descriptive statistics on firms’ WCPV for Italian (top panel) and French (bottom panel) firms. The table indicates the number of products in WCPV, the share of destinations covered by WCPVs and the share of exports covered by products in WCPVs. First, we observe that the average number of unique products in the whole set of WCPVs is about 8 both in Italy and in France. This is substantially lower than 13, the average number of products exported in the two countries. Second, a WCPV is exported, on average, in about 60% of the destinations served by a firm, again both in Italy and France. Third, products in WCPVs account for a large share of a firm’s total exports, on average about 80%. Finally, the average export share of products in a

WCPV is around 10%.

All together these statistics point at the existence of a combination of products that is a strict subset of the entire set of goods exported by a firm and that is sold in a great deal of its active destinations. The sales distribution within this subset is very skewed but overall this combination of products appears to be extremely relevant in terms of the total exports it can account for. For these reasons we identify these products as a firm’s stable core of its products portfolio.

In the rest of this section we investigate which are the drivers behind the choice of exporting a WCPV in a given destination focusing, in line with the previous analyses, on the role of market size, market structure and market positioning. With this aim we estimate the following regression

23

Table 8: PROBABILITY OF EXPORTING THE WCPV, 2006.

(1a)

ITALY

(1b) a (2a)

FRANCE

(2b) a

Dependent variable: DWCPV f d

Market size f d

Market structure

Adj.

R

2 f d

Market positioning f d

0.023

0.091

0.027

0.127

(0.003) [0.000] (0.012) [0.000] (0.003) [0.000] (0.015) [0.000]

-0.039

-0.027

-0.035

-0.027

(0.005) [0.000] (0.004) [0.000] (0.008) [0.000] (0.006) [0.000]

0.013

0.056

0.012

0.061

(0.001) [0.000] (0.006) [0.000] (0.001) [0.000] (0.007) [0.000]

0.32

0.38

N.Obs

Firm FE

Country FE

664,419

Yes

Yes

229,450

Yes

Yes

Notes : Table reports regression on the WCPV. Data are for 2006.

a

Columns (1b) and (2b) report standardized coefficients. Standard error clustered at firm and country level. Coefficients reported together with standard errors

(brackets) and p-values (squared brackets).

model

DW CP V f d

= β

1

Market size f d

+ β

2

Market structure f d

+ β

3

Market positioning f d

+ α f

+ α d

+ f d

(4)

, where DWCPV f d is a dummy equal to 1 if a firm f is exporting a WCPV in destination d , X f d,k are our three firm-destination specific regressors and α f and α d are firm and destination fixed effects, respectively. Regressors are logarithms of geometric means so that we could interpret the estimated coefficients as semi-elasticities but, as above, we focus our discussion of the results on estimates obtained with standardized variables.

Columns (1b) and (2b) in Table 8 report the results. The picture that emerges appears in line with the previous results and it confirms the strong similarity between France and Italy. Market size seems also in this case to be the major factor in action. The coefficients on the market size are positive and statistically significant suggesting that the higher the level of demand in a destination, the higher the likelihood that a firm will reach that market with a product combination that includes its core product vector. Concerning market structure, the estimated coefficients indicate that when facing higher concentration a firm is less likely to export its weak core product vector. That is, a firm tends to serve a destination characterized by tougher competition with its core products.

Interestingly, this result is in line with one of the findings of Mayer et al. (2014) according to which firms respond to increase in competition by exporting those products which are most directly

24

related to their core competencies. Finally, the coefficients on the market positioning are positive and statistically significant. This suggests that the closer a firm’s positioning with respect to its competitors in a market, the more likely that this firm concentrates its exporting activity on its core products.

6 Discussion

Four facts concerning firms’ product mix choices across destinations emerge from the empirical analysis documented above. First, we observe a strong variability in a firm-product export sales across destinations which is not entirely explained by firm-product and product-country heterogeneity. Second, by using the novel concept of firms’ product vector, we show that firms’ product mixes are very heterogeneous across destinations: a great deal of variability is observed both in terms of the combination of products and in terms of export value shares. Third, among firm-destination idiosyncratic factors, taste heterogeneity and market structure play a crucial role in explaining such variability. Fourth, in a firm’s product mixes together with a fickle part there exists a component which is stable across destinations: within a firm we observe that some combinations of products are typically exported to several destinations suggesting the existence of a core part in the product vector.

What do these results imply for distinguishing among theories on firms’ product mix choices in international markets? The several approaches that have been considered in the literature, while successful in replicating some of the stylized facts on multi-product exporters, have in common two main limitations with respect to the investigations presented in this paper. First, they are not directly aimed at explaining the variability of the firms’ product mixes across different destinations.

Second, all the existing models treat each product within a firm in isolation without taking into account possible interdependences associated to technology or demand factors.

A first set of international trade models consider, in a monopolistic competitive setting, multiproduct firms facing a product ladder where productivity declines for each additional variety produced.

Mayer et al. (2014) assume firm-product specific marginal costs increasing with scope together with non-CES preferences which generate the prediction that firms’ sales are more skewed towards core competences in more competitive markets. In Arkolakis and Muendler (2010) firms face product specific marginal costs which are a decreasing function of a firm’s scope and productdestination specific incremental local entry costs which augment with the number of products exported. If the combination of two costs is strictly increasing in a firm’s scope then sales within a destination are concentrated in a few core products, wide-scope exporters sell more of their top selling products than narrow-scope exporters and sales of the lowest selling products decline with scope.